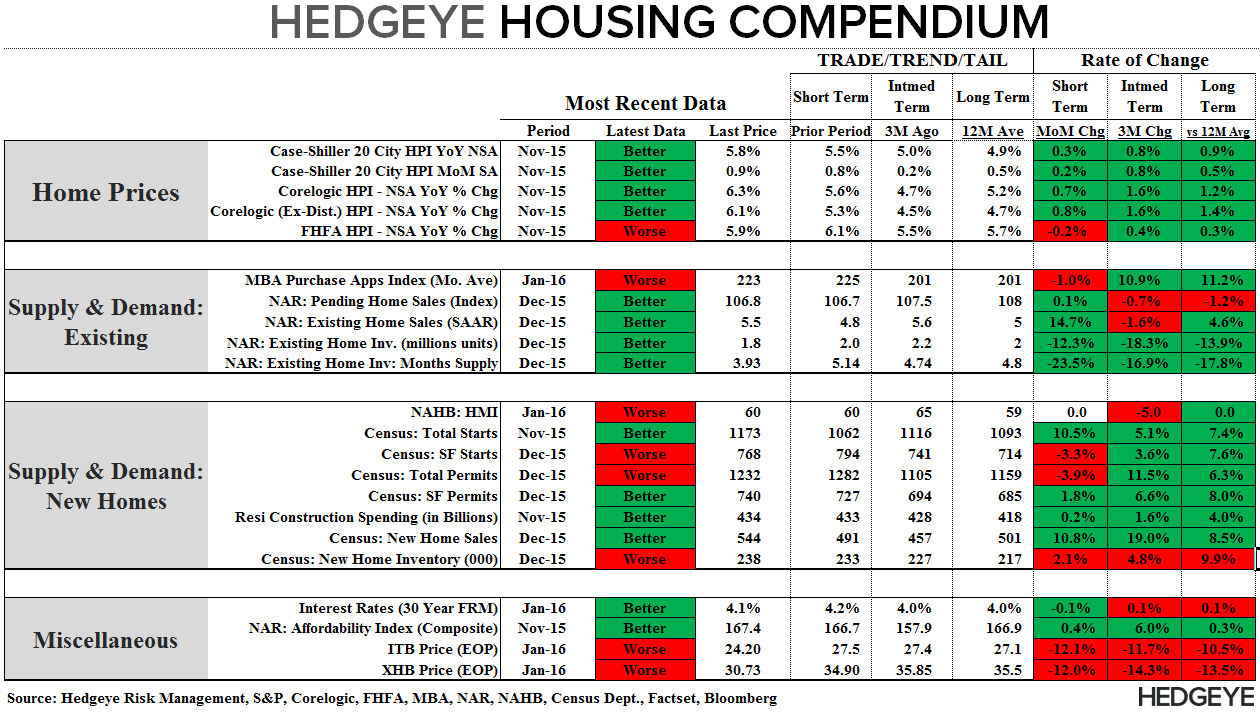

Our Hedgeye Housing Compendium table (below) aspires to present the state of the housing market in a visually-friendly format that takes about 30 seconds to consume.

Today’s Focus: December Pending Home Sales

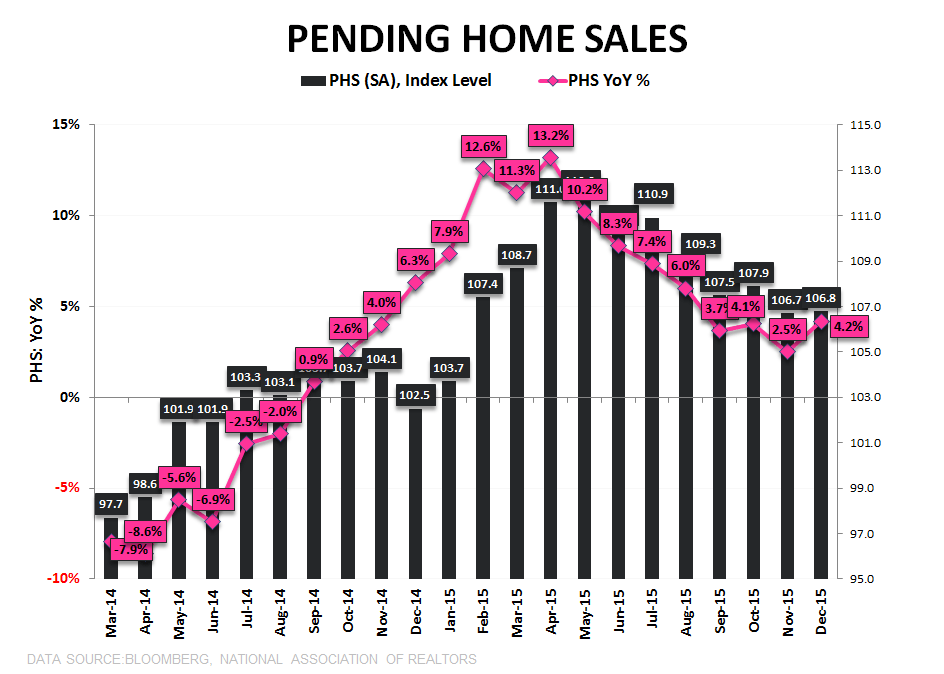

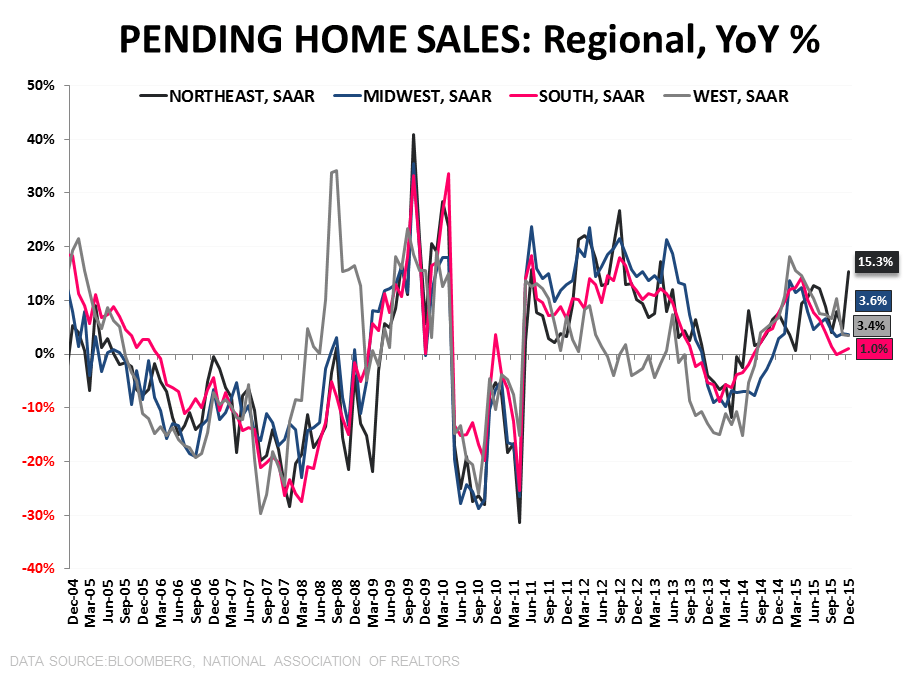

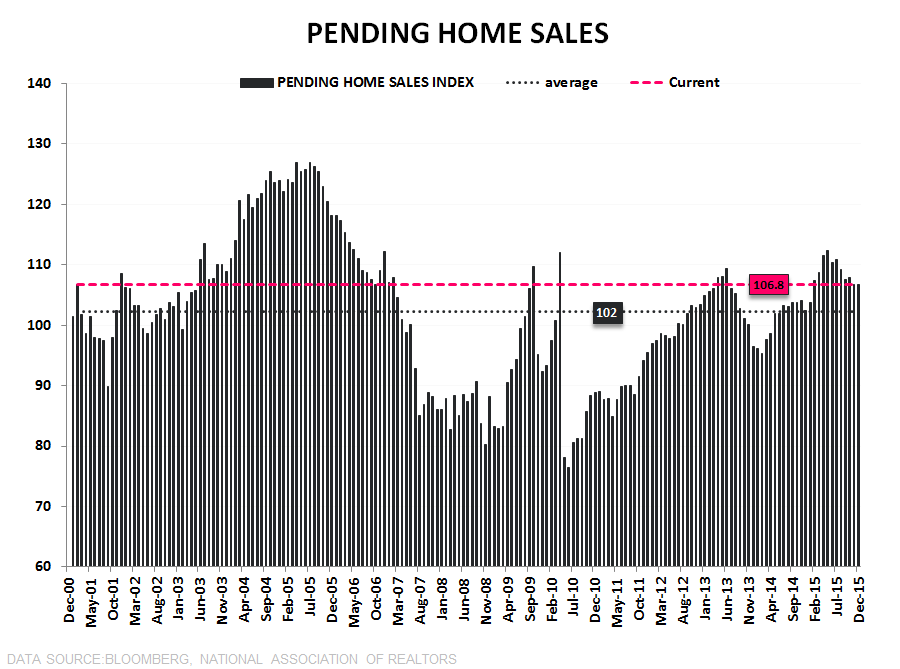

Sales in the existing home market continue to underwhelm. Signed Contract activity rose +0.1% MoM and accelerated +170bps to +4.2% YoY as a softer comp supported the rate-of-change improvement. There are probably four notable takeaways:

- First, the step function rise in Purchase Application demand beginning in Mid-November has not similarly manifested in signed contract or closure activity reported by the NAR. In other words, you can take the recent strength in MBA numbers with a grain of salt.

- Second, with sales activity basically flat sequentially, mild weather doesn’t appear to have been an outsized driver of activity – and if it was, its masking further softening in the underlying trend. For a broader discussion of the dynamics at play in the Nov-Jan housing data please see yesterday’s note Watch The Trees, Not The Bark

- Third, flat growth isn’t going to cut it against progressively steepening comps into mid-2016. Demand growth will have to show some resurgent mojo to avoid negative YoY growth against Apr/May compares. For reference, the average on the index over the last 4-months = 107.2 – almost -5% lower than the 112 level recorded in Apr/May of last year.

- Fourth, The TRID backfill and PHS re-coupling dynamics that supported the strong rebound in EHS last month should reverse and augur a soft or similarly underwhelming Existing Home Sales release for January (release on 2/23).

In short, better sequentially but not “Better”. The positive 2nd derivative trends observed over much of 2015 will continue to reverse as we head through 2016.

About Pending Home Sales:

The Pending Home Sales Index is a monthly data release from the National Association of Realtors (NAR) and is considered a leading indicator for housing activity in the US. It is a leading indicator for Existing Home Sales, not New Home Sales. A pending home sale reflects the signing of a contract, but not the closing of the transaction, which occurs 1-2 months later. The NAR uses data from the MLS and large brokers to calculate the Pending Home Sales index. An index value of 100 corresponds to the average level of activity during 2001.

Frequency:

The NAR Pending Home Sales index is released between the 25th and the 31st of each month and covers data from the prior month.

Joshua Steiner, CFA

Christian B. Drake