“Historically, the claim of consensus has been the first refuge of scoundrels; it is a way to avoid debate by claiming that the matter is already settled.”

-Michael Crichton

While consensus still regards the labor market as strong and improving, the simple fact is that the labor data is getting less good from a rate of change standpoint. This matters, as second derivates are the natural precursor/harbinger to first derivate changes. Initially, things get less good, then they get bad. Initial jobless claims have hit their frictional lower bound and we're coming up on the anniversary of that lower bound meaning that the best they can do going forward is not get any worse. Imagine if that were a company at full earnings power/potential and the best it could is not see earnings decline going forward. Not to digress, but what would that be worth? Obviously, not much of a growth premium and yet the market is still trading at its 9th highest decile on CAPE since 1926. The analog here for Financials is peak earnings from a credit standpoint for balance sheet-intensive Financial companies. We've finally begun to see credit costs stop falling, and in some cases they have begun to rise. Even with some late-cycle loan growth, this spells peak earnings. Stairs up, elevator down.

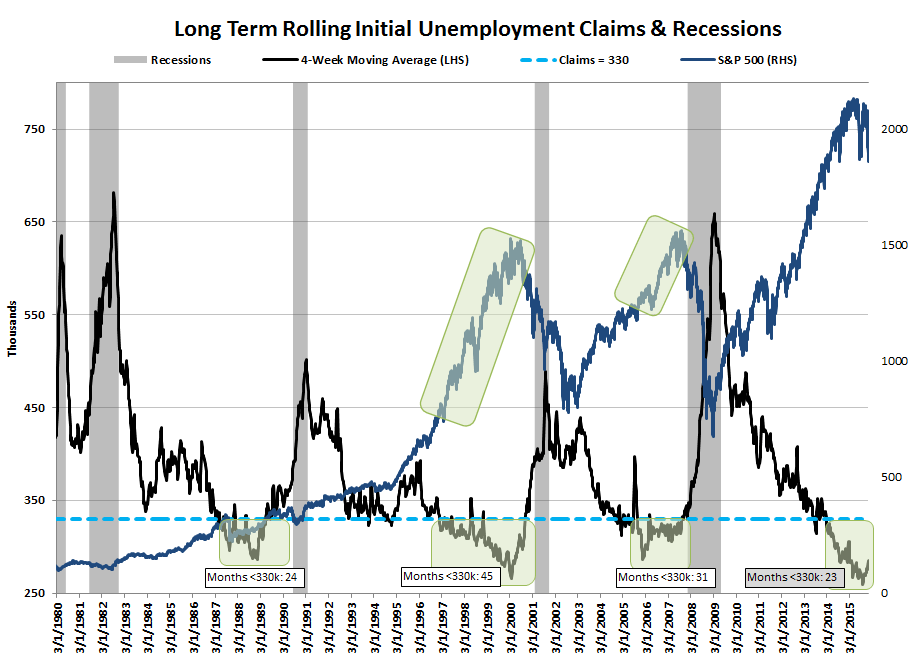

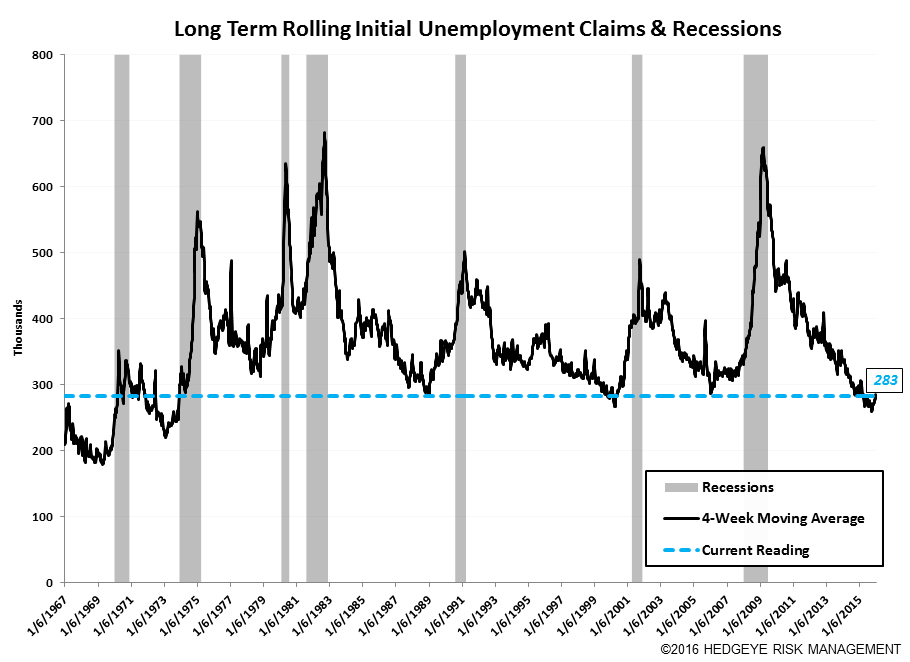

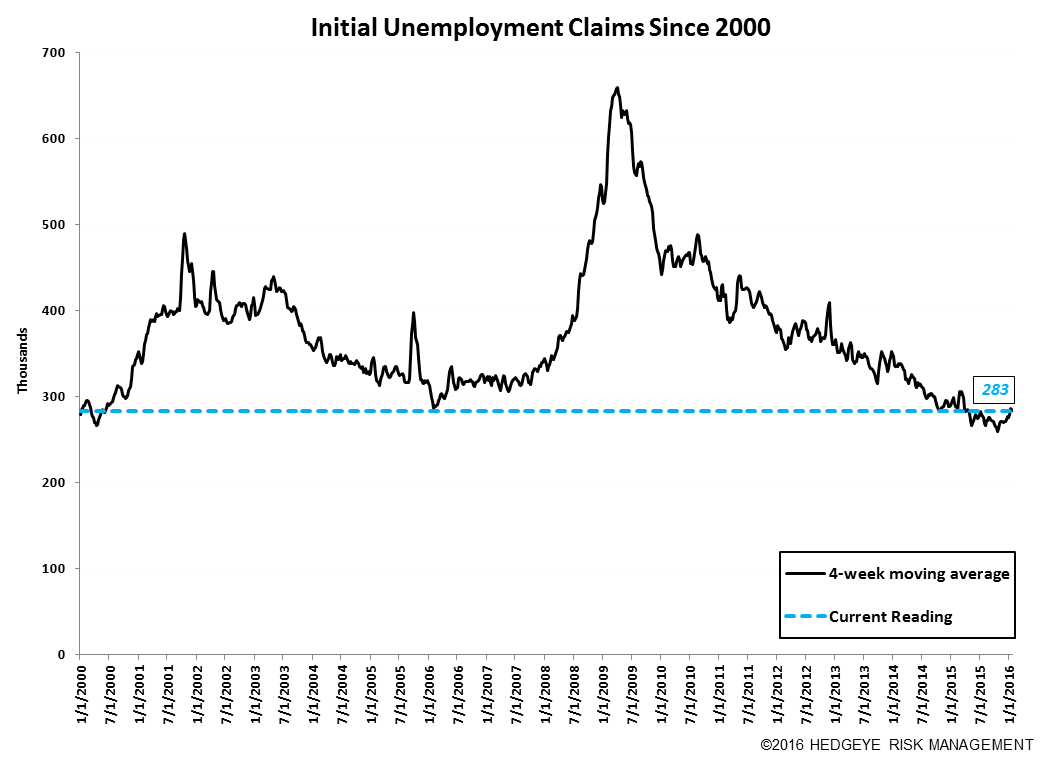

Meanwhile, rolling SA claims are in their 23rd month below 330k. The last three cycles saw claims remain below 330k for 24, 45 and 31 months (33 months on average) before the economy entered recession. That puts us 10 months from the average, 1 month from the min and 22 months from the max. Any way you slice it, the hour is late and there's a faint glow of asteroid on the horizon.

The following three charts show the continued labor market deterioration in energy states. The Y/Y rate of change in energy state jobless claims continued at a +13% pace in the week ending January 16 versus the -7% rate of improvement in the Total U.S. excluding those 8 energy states.

The data

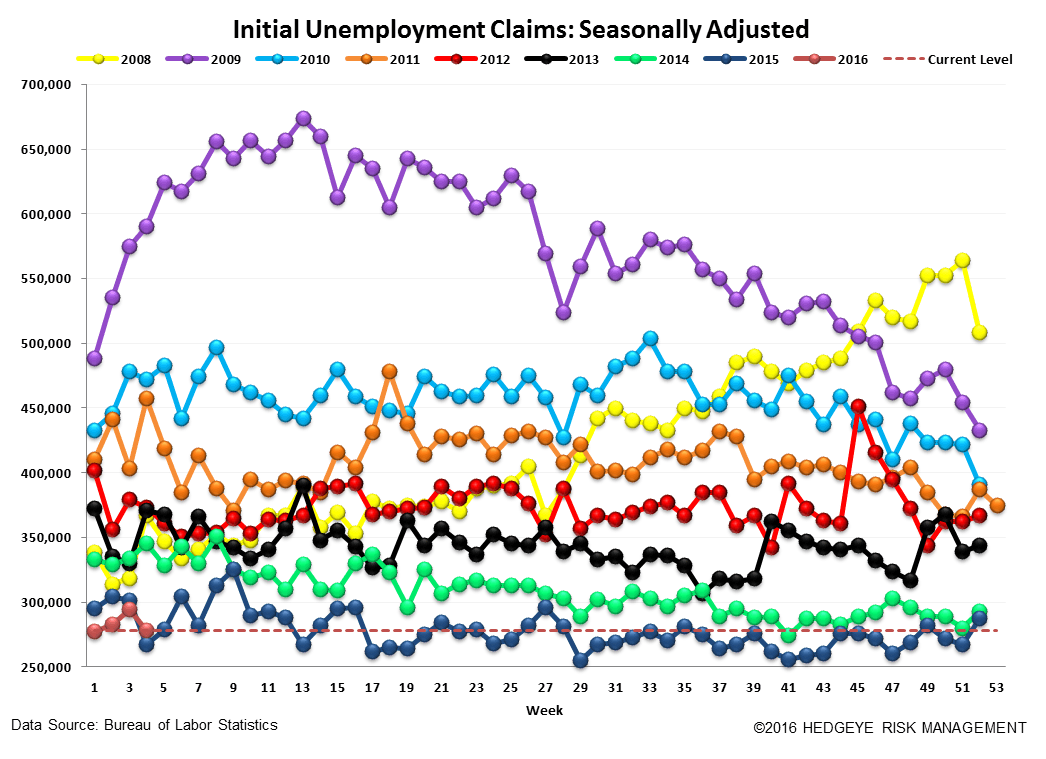

Prior to revision, initial jobless claims fell 15k to 278k from 293k WoW, as the prior week's number was revised up by 1k to 294k.

The headline (unrevised) number shows claims were lower by 16k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims fell -2.25k WoW to 283k.

The 4-week rolling average of NSA claims, another way of evaluating the data, was -3.1% lower YoY, which is a sequential deterioration versus the previous week's YoY change of -6.2%

Yield Spreads

The 2-10 spread rose 1 basis point WoW to 116 bps. 1Q16TD, the 2-10 spread is averaging 119 bps, which is lower by -17 bps relative to 4Q15.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT