“Reputation is a bubble which man bursts when he tries to blow it for himself.”

-Someone Observing The Old Wall

So a short, aging, Wall St. guy from the CT burbs (with 4 kids) walks into a room with 2 strapping younger dudes…

That is my professional life. And no, I’m not the young buck who walks in looking like Cam Newton (Darius). I’m the fatter version of a former me who is on Day 7 of a roady, covering 4 cities (New York, Boston, San Francisco, and Los Angeles) trying to keep up with these guys.

The meetings go great. We have this crazy contrarian thing called the time-series of economic data that augments this other thing called our macro opinion. We are The Bears. Raging. We get that. We also get that our reputation will hinge on whether or not we overstay our welcome.

Back to the Global Macro Grind…

Do you think, for more than 3 seconds, that I don’t want to call the bottom? Seriously. I have spent almost 17 years trying to understand, respect, and measure tops and bottoms.

Lesson #1: Both tops and bottoms are processes, not points.

As the legendary Paul Tudor Jones taught us, it’s the last part of the macro move that makes the most fools out of us. In fractal math, we’d call that the last 1/3 of the move. It’s where the “value” guy buys too early, and the bear covers too soon. (both BUY orders)

Lesson #2: Be there for the last 1/3 of the move (SELL bounces).

So, no matter where your “market” opinion has been over the last 18 months, here we are. There are no excuses. There is no finger pointing. Our reputations will be won or lost by the decisions we make next. This is not a charitable exercise. This is Wall Street.

Lesson #3: Stop opining. Give me the wood.

And since I’ve done that for 7 straight marketing days, I will do that (again) on the 8th day. I’ll put my reputation on the line and keep pressing our best call – the probability of a US #Recession is rising (not falling). Consensus isn’t yet Bearish Enough.

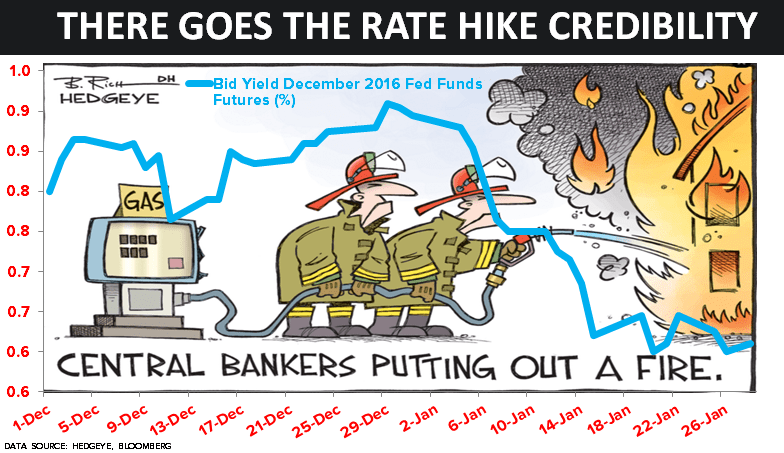

As a result, the Reputational Bubble that is popping is that of an un-elected and un-accountable bureaucracy called The Federal Reserve. Until Bernanke’s legacy of linear forecasters embrace the non-linearity of it all, one of the most obvious risks remains their forecast.

That is why the #Deflation & #GrowthSlowing bears won (again) yesterday. To summarize:

- The Fed continues to be a pro-cyclical version of a Labor Economist (Overweight #LateCycle employment data)

- The Fed continues to call something that’s been pervasive (#Deflation) “transitory”

- And, as a result, the Fed continues to be behind the curve, lagging both real-time economic data and market moves

No, the Fed wasn’t “dovish enough” in their statement. Newsflash: they are still hawkish and in “rate hike” mode. And it’s going to take at least another 3-6 months for them to catch up to our economic view. That’s the bull case!

Our Top 3 Macro Theme Ideas on the long side remain:

- Long US Dollars (UUP)

- Long The Long Bond (TLT)

- Long Utilities (XLU)

Our Top 3 Macro Theme Ideas on the short side remain:

- Russell 2000 and SP500

- Junk Bonds (JNK)

- Financials (XLF)

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.96-2.06%

SPX 1

RUT

USD 98.64-99.63

Oil (WTI) 28.01-32.98

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer