Let’s face facts…these Coach numbers stunk something awful. Sales were +4%, but down 3% excluding the addition of Stuart Wietzman. Even including the deal, gross profit was down 2%, EBIT was down 5%, and EPS down 7% -- and this was on top of a 31% EPS decline last year, and 14% decline the year before. Terrible numbers for any company that actually cares about driving a basic financial model.

But we’re not talking about one of those companies. We’re talking about Coach – a company that has not grown sales organically since the debut of the iPhone 5. When we added Coach to our Long bench (after being short for over 2-years) in December all we were looking for was incremental lack of weakness on the margin. We definitely got that.

So what would make us get full-on bullish? It would be confidence that this company can actually grow it’s top-line sustainably. From a modeling perspective, we can move the 69% gross margin or the 50% SG&A ratio around by a few points here or there. But the only thing that makes this clock tick is revenue growth. Our confidence on that one still needs some work.

But until then, there are a few metrics that keep us in the game with a positive bias.

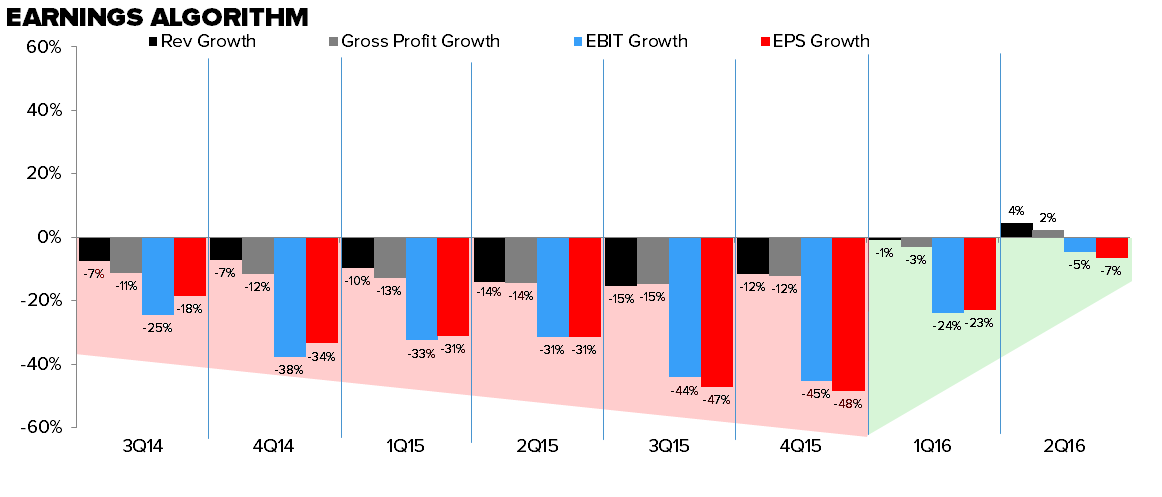

1. The first is the raw earnings algorithm. For two years it’s been terrible, and for two quarters it’s been…well, better. The chart below suggests that earnings are hitting a trough – and we’d point out that that this is the same time other companies will see increased downward revisions as the economy weakens.

2. The SIGMA chart for COH looks outstanding. Coach has not been this clean with its inventory position since 4Q10 (iPhone 4…to stick with that metaphor). This is an extremely positive gross margin setup for COH. Stocks usually don’t (almost never) go down when the picture looks like what you see below.

3. The last thing that keeps us positive is not a metric, but a group attribute. Since August 2014 ‘The Space’ has been a disaster. Not necessarily the business trends, but definitely the stocks. This hit KATE the hardest, as it continued to deliver but had its multiple cut in half while Kors and Coach put up horrific numbers. But now Coach is stabilizing. We’re pretty sure that KATE is performing well. That just leaves Kors as the lone brand hemorrhaging share. It’s tough to make the case that ‘The Space’ is broken when only one brand is on the decline. In this scenario, COH and KATE (which have a dramatically different customer, by the way – see graphic at the bottom of the note) help each other, allowing Kors to shoot itself in the foot – in the US, at least – all by its lonesome.