Commodity-leveraged credit, which moved on a lag to top-down commodity deflation, is now FAST on the move.

With large impairment charges and write-downs foreshadowed by many large producers, credit markets are front-running balance sheet contraction to reflect lower short and long-term commodity price assumptions:

- BHP made a pre-earnings announcement of a $7.2 Bn pre-tax impairment charge on U.S. shale assets.

- Australia’s Woodside Petroleum said it expects to take an ~$1 Bn pre-tax impairment hit due to lower long-term oil price assumptions when it announces its full-year 2015 results in mid-February.

As we flagged in a recent note PRODUCER LEVERAGE , much of the spread risk lies with what are current IG credits.

Two important points we would make with respect to the more recent moves in credit markets:

1) Both high-yield AND investment grade have historically moved together when spreads widen (all corporate credit is at risk), and there is a large amount of IG credit that could move high-yield in 2016 in the current price environment.

2) A good chunk of low-notch IG commodity credit trades like it’s going high yield, but there is also a large chunk that is 1-2 notches off lowest IG-Notch that has just started moving in the last couple of months – These issues are worth a look if you are behind our pending recession call.

To consolidate concerning commentary from S&P & Moody’s on the shift in credit quality at the end of last week:

- S&P: More companies were at risk of having their credit ratings cut at the end of December than at the close of any other year since 2009

- S&P: The number of potential downgrades was at 655, compared with 824 reported by the finish of 2009

- S&P: The year-end total for 2015 was "exceptionally" higher than a yearly average of 613

- S&P: Oil-exporting countries face fresh downgrades as crude prices fall further. The agency currently has Azerbaijan, Bahrain, Kazakhstan, Oman, Russia, Saudi Arabia, Brazil, and Venezuela on negative watch.

- Moody’s: Friday morning, Moody's disclosed it was putting the ratings of 120 Oil & Gas companies and 55 mining companies on watch.

- S&P: Revised 2016 and 2017 metals price assumptions late Friday night, following on its recent reduction in 2017 oil price forecasts from $US65 a barrel to $US45. (expected but meaningful):

- Iron Ore: Cut to $65/MT for 2015-16 vs. $85/MT back in October

- Copper: $2.70/lb. for 2015 through 2017, down from its previous forecast of $3.10/lb. for 2015-2016

- Gold: Forecasts remain flat at $1,200 per ounce for the period from 2015-2017.

- Nickel: Lowered from $8.00/lb. in 2015-2016 to $6.50/lb. this year and $7.25/lb. in 2016

- Zinc: Lowered from $1/lb. this year to $0.95, but maintained its $1/lb. forecast for 2016

In the table below, we have pegged a significant amount of investment grade credit from commodity producers that could get downgraded to high-yield ($227Bn) -- some credits much more at risk near-term than others.

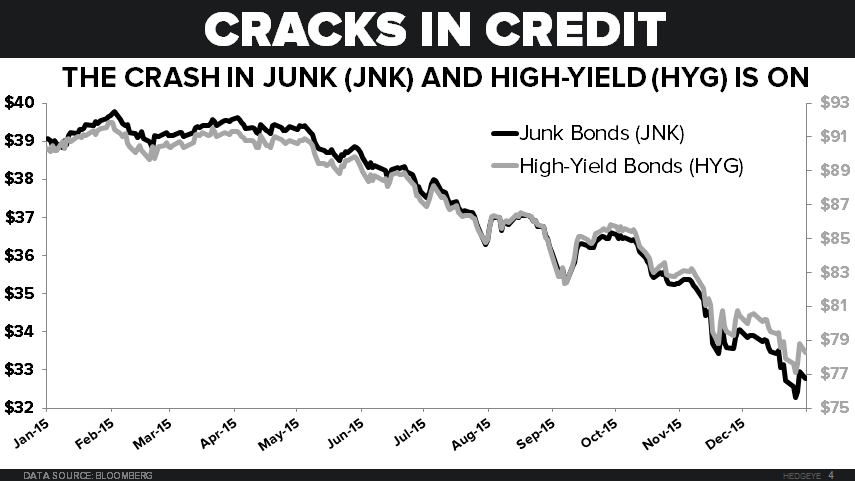

A move to HY from IG should perpetuate spread risk with forced selling from institutional money. As mentioned above and with regards to our short JNK position, the insurance on low-IG credit in the commodities space that hasn’t moved as much (YET) is worth a look into a potential recession as a way to play our short JNK view outlined in the Q1 Themes deck.

One of the bubbliest charts we’ve put together alongside the above slide as it relates to commodity producer balance sheet leverage is one that shows interest expense skyrocketing despite unprecedented lows in financing expense. We continue to think the deleveraging here is in the early innings.

Ben Ryan

Analyst