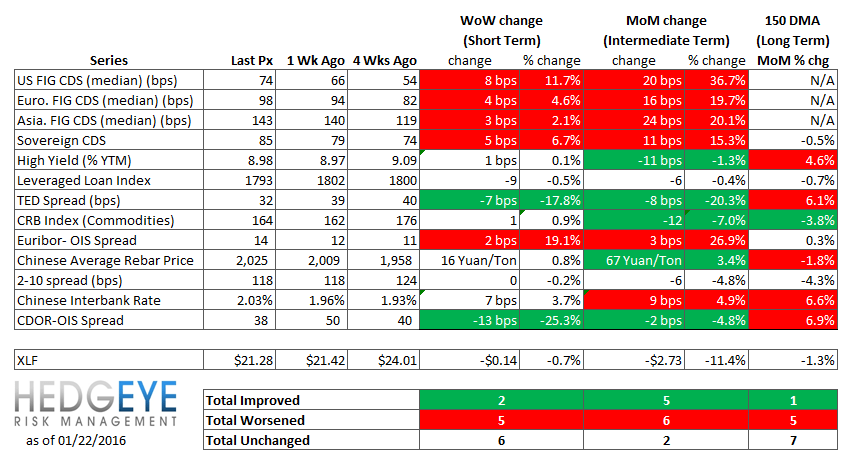

Key Takeaway:

Slowing growth continued to grip global markets last week. Data came out showing that Chinese 4Q GDP decelerated to 6.8% y/y from 6.9% in 3Q, driving CDS in the U.S., Europe, and Asia higher. Additionally, the Euribor-OIS spread, a measure of counterparty risk in the Eurozone, widened by +2 bps last week, and concern over non-performing loans has reached the point that the ECB announced it is investigating a number of Eurozone banks about their management of such loans. Italian Banco Popolare confirmed that it is undergoing such an investigation, and its CDS widened by +63 bps to 333.

Another measure of counterparty risk, which we have added to the bottom of our monitor this week, is the CDOR-OIS spread. It is the Canadian equivalent of the Euribor-OIS spread and measures the difference between the Canadian interbank lending rate and overnight indexed swaps. In other words, it measures counterparty risk in the Canadian banking system. The measure hitting a post-crisis high of 50 bps on January 15 prompted us to start tracking it. The spread has since tightened somewhat to 38 bps but remains elevated.

Our heatmap below remains mostly negative across all durations.

Current Ideas:

Financial Risk Monitor Summary

• Short-term(WoW): Negative / 2 of 13 improved / 5 out of 13 worsened / 6 of 13 unchanged

• Intermediate-term(WoW): Negative / 5 of 13 improved / 6 out of 13 worsened / 2 of 13 unchanged

• Long-term(WoW): Negative / 1 of 13 improved / 5 out of 13 worsened / 7 of 13 unchanged

1. U.S. Financial CDS – Swaps widened for 10 out of 27 domestic financial institutions with an average change of +2 bps as concerns over slowing Chinese growth and low oil prices continued to drive risk concerns. At the bottom of our U.S. CDS table below, we have added indices on investment grade and high yield CDS, which tightened last week by -6 bps to 104 and by -31 bps to 525, respectively.

Tightened the most WoW: ACE, MMC, CB

Widened the most WoW: AIG, AXP, BAC

Widened the least/ tightened the most WoW: CB, MTG, AGO

Widened the most MoM: AIG, AXP, COF

2. European Financial CDS – Swaps mostly widened for European banks last week. With low oil prices one of the driving factors in market weakness, Russian Sberbank CDS continued to be significantly affected, widening by +32 bps to 445. In Italy, Banco Popolare CDS widened by +63 bps to 333 as it announced the ECB is investigating the bank's management of non-performing loans. Additionally, in Portugal, with the issue of transferring risk between Novo Banco and Banco Espirito Santo remaining volatile, Banco Espirito Santo CDS tightened by -291 to 937.

3. Asian Financial CDS – Swaps mostly widened across Asian Financials last week, rising by +6 bps on average. Indian bank swaps saw the widest moves, increasing between +11 and +16 bps.

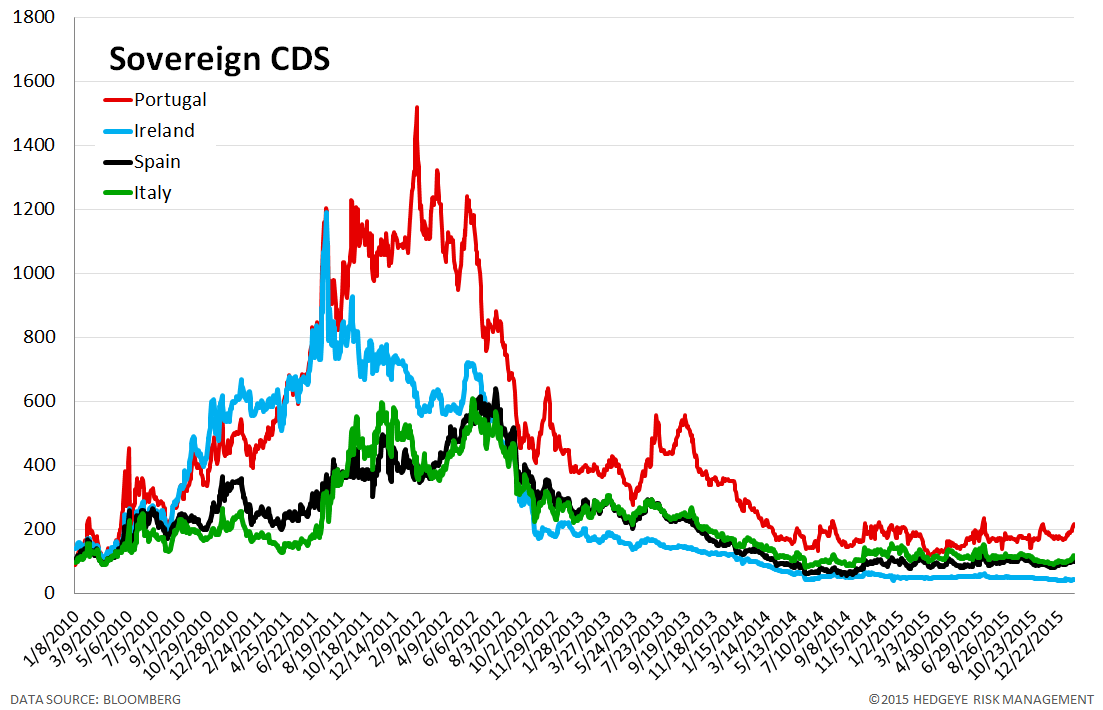

4. Sovereign CDS – Sovereign Swaps mostly widened over last week. Portuguese swaps widened the most, by +16 bps to 209.

5. Emerging Market Sovereign CDS – Emerging market swaps recovered somewhat from recent widening last week, tightening by -6 bps to 223 at the median, although still higher by +18 bps month over month.

6. High Yield (YTM) Monitor – High Yield rates rose 1 bps last week, ending the week at 8.98% versus 8.97% the prior week.

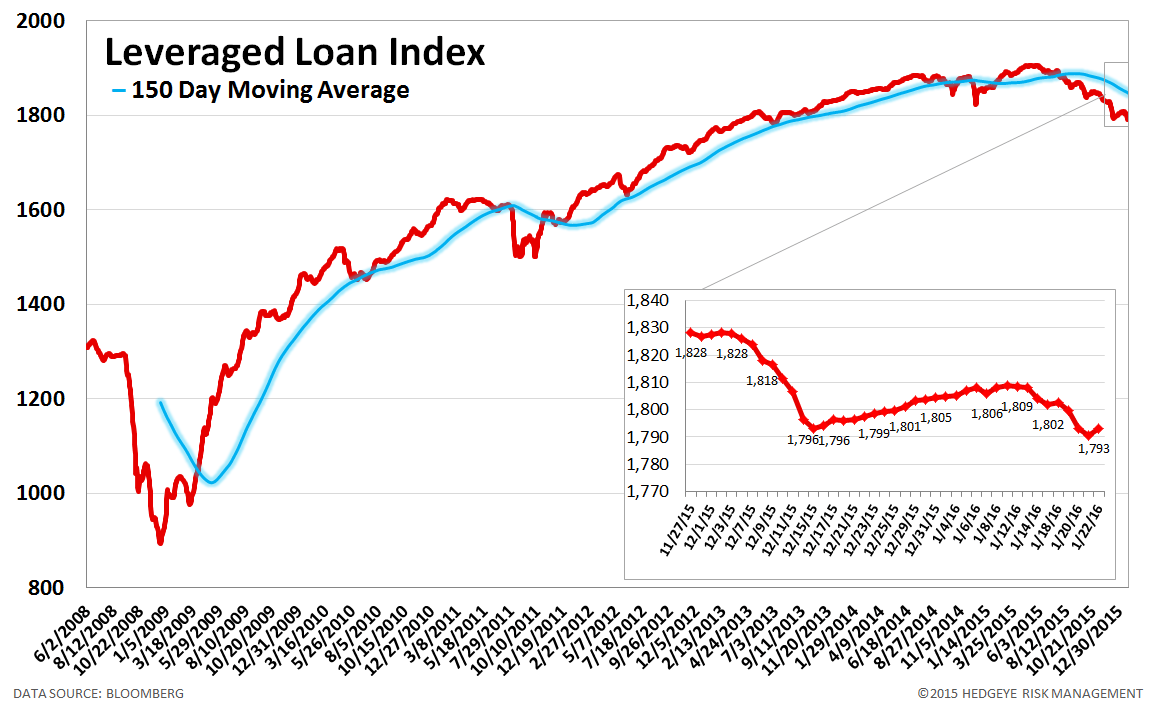

7. Leveraged Loan Index Monitor – The Leveraged Loan Index fell 9.0 points last week, ending at 1793.

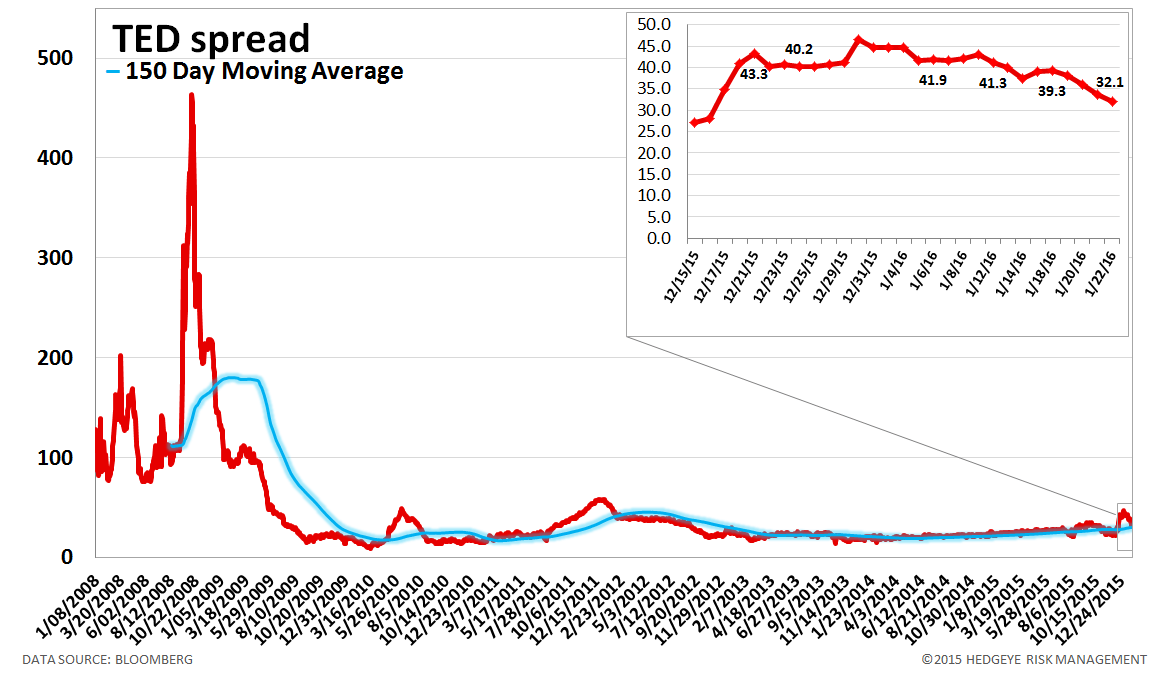

8. TED Spread Monitor – The TED spread fell 7 basis points last week, ending the week at 32 bps this week versus last week’s print of 39 bps.

9. CRB Commodity Price Index – The CRB index rose 0.9%, ending the week at 164 versus 162 the prior week. As compared with the prior month, commodity prices have decreased -7.0%. We generally regard changes in commodity prices on the margin as having meaningful consumption implications.

10. Euribor-OIS Spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS spread widened by 2 bps to 14 bps.

11. Chinese Interbank Rate (Shifon Index) – The Shifon Index rose 7 basis points last week, ending the week at 2.03% versus last week’s print of 1.96%. The Shifon Index measures banks’ overnight lending rates to one another, a gauge of systemic stress in the Chinese banking system.

12. Chinese Steel – Steel prices in China rose 0.8% last week, or 16 yuan/ton, to 2025 yuan/ton. We use Chinese steel rebar prices to gauge Chinese construction activity and, by extension, the health of the Chinese economy.

13. 2-10 Spread – Last week the 2-10 spread was unchanged at 118 bps lats week. We track the 2-10 spread as an indicator of bank margin pressure.

14. CDOR-OIS Spread – The CDOR-OIS spread is the Canadian equivalent of the Euribor-OIS spread. It is the difference between the Canadian interbank lending rate and overnight indexed swaps, and it measures bank counterparty risk in Canada. The CDOR-OIS spread tightened by 13 bps to 38 bps last week.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT