Jittery markets continue to trade all over the map with significant gap up and draw down days digesting a helter skelter of global market information in 2016. The S&P 500 put in a marginally positive holiday shortened week of +1.3% but still sports a decidedly negative -7% start to the New Year. Exchange activity however continues to propel higher with incremental volatility and investor uncertainty. Cash equity volume in 1Q16TD is now up +38% Y/Y, with equity options activity now up +33% Y/Y, with futures at a +25% growth clip over 2015. CME Group (CME) thus far, half way through January, has set all-time trading volume highs of 19.1 million futures and options contracts per day, taking out the former high of 17.5 million in average daily volume (ADV) in October 2014 on the potential for a Greek exit from the European Union. While CME stock has been caught up in the market swoon (with its valuation compressing), the earnings power of the Merc has increased (and is threatening to do so for the intermediate term with the swelling of open interest as well). Thus it will just be a matter of time in our view, before CME stock perks up (although it is already outperforming the broader market by ~150 bps).

Weekly Activity Wrap Up

This week, cash equity trading volume came in at 10.7 billion trades per day, bringing the quarter's ADV to 9.5 billion. Options traders exchanged 23.0 million contracts per day, bringing the 1Q16TD average to 20.6 million. Futures activity came in at 28.5 million contracts per day, bringing the 1Q16TD average to 24.9 million.

U.S. Cash Equity Detail

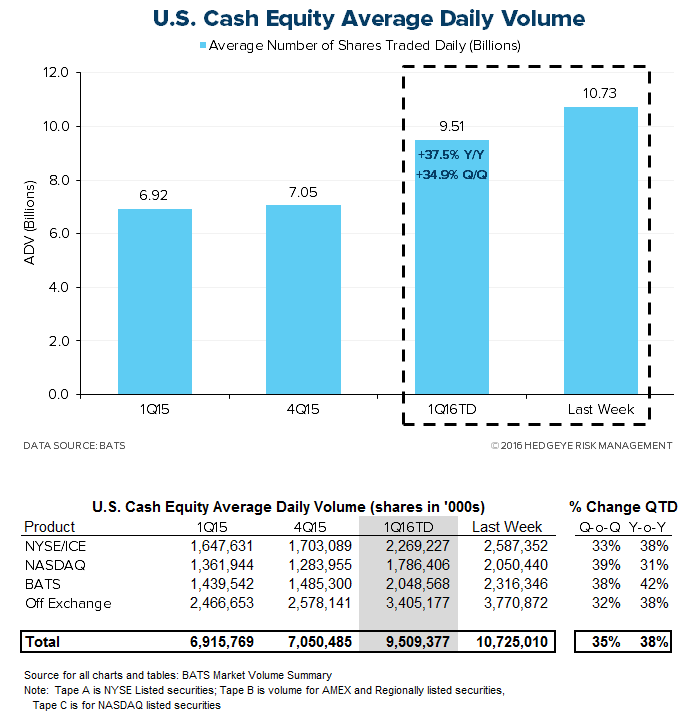

U.S. cash equities trading came in at 10.7 billion shares per day this week, averaging with last week to bring the 1Q16 average so far to 9.5 billion shares per day. That marks +38% Y/Y and +35% Q/Q growth. The market share battle for volume is mixed. The New York Stock Exchange/ICE is taking a 24% share of first-quarter volume, which is consistent with the prior quarter and year-ago quarter, while NASDAQ is taking a 19% share, +57 bps higher Q/Q but -91 bps lower than one year ago.

U.S. Options Detail

U.S. options activity came in at a 23.0 million ADV this week, bringing the 1Q16TD average to 20.6 million, a +33% Y/Y and +29% Q/Q contraction. In the market share battle amongst venues, NYSE/ICE has been trending downward at a moderate pace, but at an 18% share it is +125 bps higher than the year-ago quarter. Meanwhile, NASDAQ's recent declines bring it -440 bps lower than 1Q15. CBOE's market share is down -83 bps Y/Y but has improved recently; its 27% share of 1Q16TD volume is up +195 bps from 4Q15. BATS and ISE/Deutsche have been taking share from the competing exchanges, with BATS up to a 10% share from 9% a year ago and ISE/Deutsche taking 16%, up from 13% a year ago.

U.S. Futures Detail

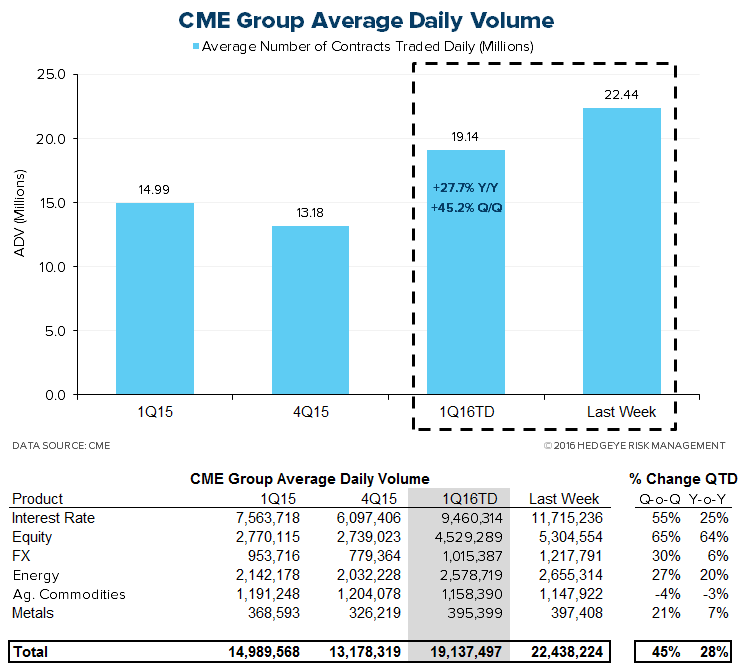

22.4 million futures contracts traded through CME Group this week, bringing the 1Q16TD average to 19.1 million, a +28% Y/Y and +45% Q/Q expansion. CME open interest, the most important beacon of forward activity, currently tallies 104.0 million CME contracts pending, good for +14% growth over the 91.3 million pending at the end of 4Q15, an improvement from last week's +12%.

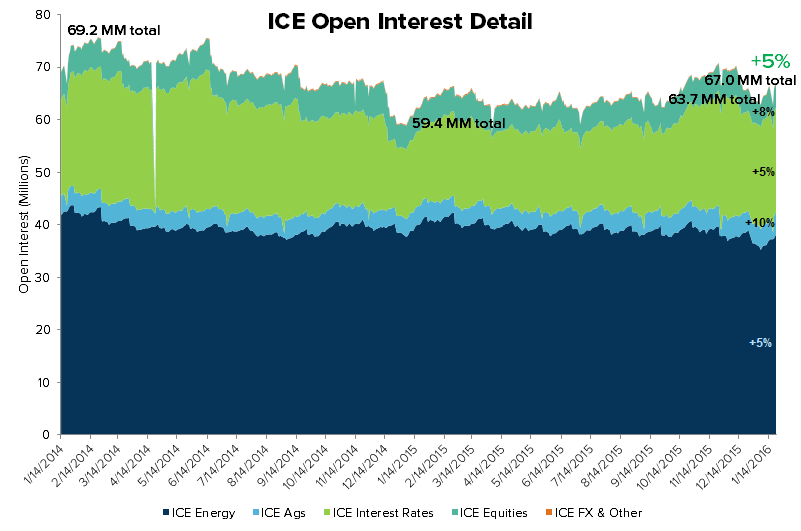

Contracts traded through ICE came in at 6.0 million per day this week, bringing the 1Q16TD ADV to 5.8 million, +15% Y/Y and +21% Q/Q growth. ICE open interest this week tallied 67.0 million contracts, a +5% expansion versus the 63.7 million contracts open at the end of 4Q15, consistent with last week.

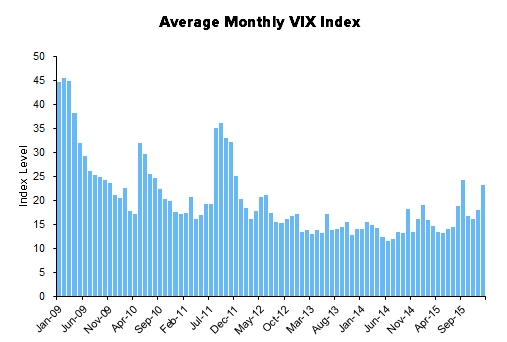

Monthly Historical View

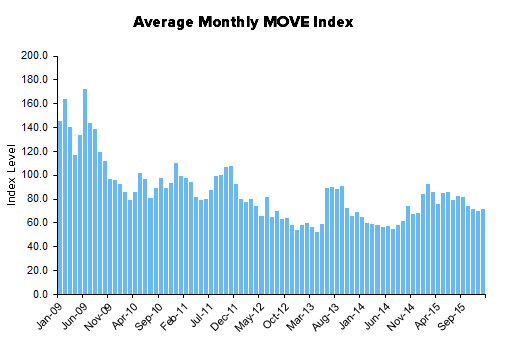

Monthly activity levels give a broader perspective of exchange based trends. As volatility levels, measured by the VIX, MOVE, and FX Vol should rise to normal levels after the drastic compression this cycle, we expect all marketplaces to experience higher activity levels.

Sector Revenue Exposure

The exchange sector has broadly diversified its revenue exposure over 10 years as public entities with varying top line sensitivity to the enclosed trading volume data. The table below highlights how trading volumes will flow through the various operating models at NASDAQ, CME Group, ICE, and Virtu:

Please let us know of any questions,

Jonathan Casteleyn, CFA, CMT

Joshua Steiner, CFA