“Volatility is an outcome revealed in markets: volatility is not causality; it is result.”

-David Kotok, Cumberland Advisors

Yesterday, Japanese equities rallied following a comment by a central bank aide who said that current circumstances would allow more easing by the BOJ, then sold off when another aide said it was too soon for incremental easing.

A few hours later, the EUR gapped lower and S&P500 futures reversed and gapped higher as Draghi said downside risks have opened up and hinted at incremental policy action come March.

Oil then rallied hard on a rise in inventories and the SPX held its gains alongside a 4th month of contraction in the Philly Fed Index, a rise in rolling jobless claims to their highest level since April of last year and SPX earnings for 4Q16 tracking at -4.0% YoY.

The 2016 equity casino is officially open.

Back to the Global Macro Grind ….

With oil higher, commodity and EM equities and currencies gaining overnight and Chinese officials vowing to “look after” stock investors, the central bank intervention trade is hoping to extend yesterday’s 1-day Viagra reflation rally another day.

A new movie, this is not. Manic price action in markets and reactionary policy responses out of central banks are not outcroppings of improving fundamentals.

Keith likes to say: Play the game that’s in front of you.

In other words, investing in the market you want rather than the one you have is a nebula for negative alpha.

Policy aimed at hitting a misestimated potential growth target (or some unrealistic growth rate that, on paper, allows sovereigns to meet forward liabilities) represents negative policy alpha.

While the illusion of growth can be maintained for a period, sustained real growth can’t be printed and the accumulation of latent risk eventually manifests in prices.

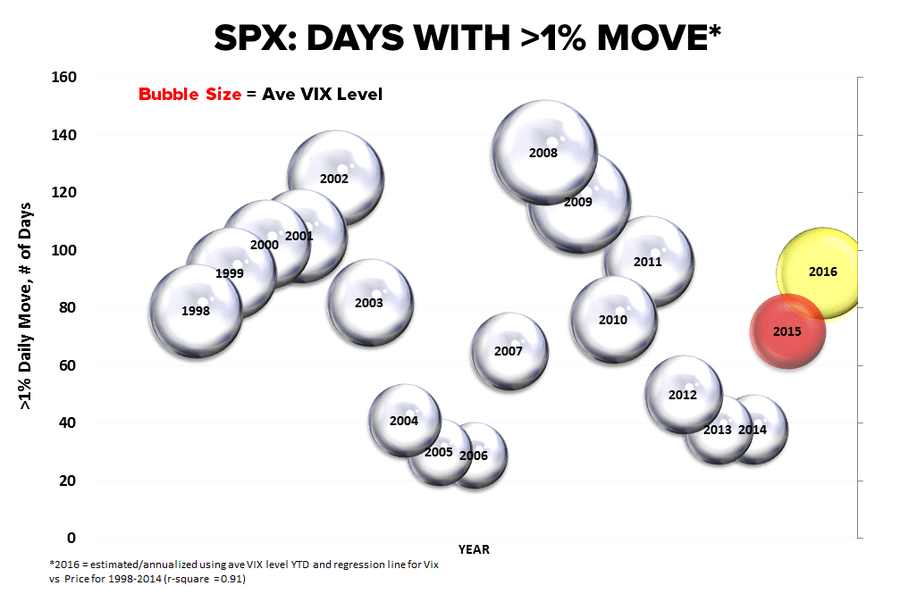

In the Chart of the Day below we plot daily price moves >1% in the S&P500 by year. The bubble size corresponds to the average VIX level for the period.

2014 marked the peak in policy induced complacency (implicit in the transition from explicitly “lower for longer” to “data dependence” is elevated uncertainty & the removal of a structural policy anchor on volatility) and with the Fed now attempting divergent policy action into a slowdown, volatility won’t be re-interred anytime soon.

In fact, if all you did was draw a line connecting the bubbles in the chart below and adjust gross/net exposure and asset allocations counter-cyclically as we predictably traversed the sine curve, you would have crushed it.

So, what’s driving the crescendo in investor angst? Is it China …. Is it oil? … elevated geopolitical risk?

In a sentiment update note from the road on Wednesday my colleague, Darius Dale, highlighted the above as consistently offered narratives attempting to explain the swoon in financial markets.

Attempting to assign definitive causes to events is a natural cognitive trapping. In viewing markets as a complex system, it’s less that those explanations are not true (in isolation) but that they are all true.

As Kotak notes “the yin and yang of data flows and interdependency influence the Sturm und Drang (Storm & Stress) of human behavior” … a cauldron of reflexivity where data, prices, expectations and behavior mix to both birth and propagate volatility.

The yin and yang of expedited price moves in commodities comes with duration sensitivity (i.e. the implications are different based on the time horizon taken).

Lower oil represents a diffuse benefit to domestic consumers. However, the flow through to reported growth is hostage to the prevailing trend towards higher savings and the benefit to non-energy consumption can show up on a variable lag (not to mention that aggregate income growth – which represents the capacity to consume – is and will continue to decelerate from here) .

On the flip side, the nearer-term concerns are both acute and highly visible as domestic producer profitability gets crushed directly, related sectors feel the follow-on effects, credit markets and spreads get stressed, and commodity export economies come under increasing pressure (with impacts ranging from higher current account deficits to revolutionary social unrest).

Further, to the extent commodity deflation is a function of a strong dollar, the cost of trade for import heavy countries rises, driving current account deficits higher and potentially stocking local inflation.

The impact to growth in developing markets can be equally severe given the proclivity for capital flows to reverse alongside policy tightening in developed markets.

When portfolio capital starts to exit, asset prices deflate and credit gets tighter, investment and consumption both decline. The currency depreciates, driving local inflation higher at the same time that aggregate demand accelerates to the downside. If demand is local and the debt is denominated in foreign currency, the debt burden on business is amplified. Declining demand in the face of a crashing currency and elevated inflation can leave policy makers handcuffed.

With $9 Trillion+ in non-bank dollar denominated debt outstanding outside of the U.S., the prospect for a resurgent wave of defaults is certainly real and rising.

Domestically, the earnings/profit/industrial recession won’t be ebbing in the next few months and expectations around a reversal in domestic monetary policy may be rightly placed - but let the data breath a bit.

Central Bank rhetoric follows the data flow and market prices on a lag and actually policy action lags the rhetoric.

When volatility rises we compress the measurement parameters in our TRADE, TREND models to more dynamically manage the risk of the probable range – it’s our way of objectively measuring and managing the stress of a roughening storm.

We’ll assuredly get more price volatility and relief bounces but we remain sellers of strength, for now.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.96-2.10%

SPX 1

RUT

VIX 22.24-29.83

USD 98.57-99.56

To poach the sign-off from our own Howard Penney …

Function in Disaster, Finish in Style.

Christian B. Drake

U.S. Macro Analyst