Below are our analysts’ new updates on our fourteen current high conviction long and short ideas. As a reminder, if nothing material has changed in the past week which would affect a particular idea, our analyst has noted this. We will send CEO Keith McCullough’s updated levels for each ticker in a separate email.

IDEAS UPDATES

MDRX

To view our analyst's original report on Allscripts Healthcare Solutions click here.

We presented our Short Case on Allscripts Healthcare Solutions (MDRX) earlier this week to Institutional Investors. The problems facing Allscripts could very well be terminal, as they continue to lose share among the largest of Health Systems.

This is a problem because as hospitals and health systems continue to merge, Allscripts' addressable market rapidly shrinks. Attrition also becomes a major issue, as Allscripts' current clients are acquired by health systems using competing solutions from Epic, Cerner, MEDITECH and athenahealth.

Our work suggests that attrition is much worse than management is letting on, and is an underappreciated reason why the correlation between bookings, sales and backlog have broken down in recent years. In fact, two of Allscripts largest clients have signed contracts with competitor Epic, for a system wide integrated EHR in 2015, with an implementation scheduled for mid-2017.

Nowhere in the press releases, filings or transcripts does management address these pending losses and what it means for the business. Instead, they are communicating a message of stability and market share gains, which according to the data, is a misleading narrative.

Bottom line: We continue to see more than 30% downside on a trend duration, with tail risk of 50% or more.

TLT | XLU | JNK

To view our analyst's original report on Junk Bonds click here and here for Utilities.

The volatile week ended with a big squeeze in equity and commodity markets, but more cracks in credit emerged, especially those bonds related to inflation expectations:

- The U.S. 10-Year yield went nowhere, declining 2bps to 2.05%

- TLT lost -0.4% -- small pullback given last week’s rip

- JNK bounced +0.3% -- weak response to last week’s sell-off if you’re a bull

Meanwhile, in 2016, Utilities (XLU) continues to be the bright spot in the equity markets. XLU is up 1% this year, having edged out all other S&P 500 subsectors by a wide margin. Last week, XLU was down marginally but was still second best among the subsectors, beating all but Healthcare (XLV). Essentially, it's paying off to own low-beta XLU in a crashing market.

Back to the bond market. Taking a longer term view, as the unwinding of the unprecedented corporate credit bubble gathers steam, the JNK move was a weak bounce in what we see as a developing crash in high yield and junk bond markets:

Rating agency S&P disclosed on Thursday three concerning stats as it relates to the wellness of credit oustanding:

- More companies were at risk of having their credit ratings cut at the end of December than at the close of any other year since 2009

- The number of potential downgrades was at 655, compared with 824 reported by the finish of 2009

- The year-end total for 2015 was "exceptionally" higher than a yearly average of 613

Then on Friday, S&P followed with additional action:

- Disclosure that oil-exporting countries face fresh downgrades as crude prices fall further and that it could repeat last year's move when it made a big group of cuts all at once

- S&P currently has Azerbaijan, Bahrain, Kazakhstan, Oman, Russia, and Saudi Arabia on negative outlook in its Europe, Middle East and Africa region, as well as Brazil and Venezuela in Latin America

Moody’s echoed the shaky state of credit markets by announcing it was putting the ratings of 120 oil and gas companies on watch Friday.

Strap on your seatbelts as we expect that credit spreads will continue to widen. If the Fed pivots on its “4 rate hikes” in 2016 as the data continues to slow, Treasury bond yields get pushed lower and high-yield spreads widen into a late cycle deleveraging. This should continue to generate alpha in a Short JNK, Long TLT trade.

The Atlanta Fed snuck in a revised growth rate expectation after the close last Friday (what timing!). It’s becoming more probable that other Fed Heads will follow and acknowledge what we have echoed for a year and a half now.

NUS

To view our analyst's original report on Nu Skin click here.

Nu Skin (NUS) has been crushed so far this year. The stock is already down roughly -16% YTD. While it did jump higher on Friday, we view this as another good opportunity to short the stock. The company is dealing with slowing distributor growth, small market share in its category, and the continued impending implications of further government intervention. This is not a company you want to be long.

FII

To view our analyst's original report on Federated Investors click here.

In 2016, the asset management sector has been hit hard on market exposure and the -7% start to the year for the S&P 500. Market depreciation is especially impactful for the asset managers as negative market returns decreases billable assets and generally compresses valuation multiples for the sector.

With many questions on the solvency of the energy sector at low current oil prices, a U.S. central bank that is incrementally hawkish, and Chinese economic results coming in well below expectations, the environment is cautious at best.

With that said, the defensive nature of Federated Investors' (FII) business, with 70% of the firm’s assets-under-management in money market fund assets is outperforming the rest of the asset managers and we expect this divergence to widen as we get further into the year.

As investors get incrementally defensive and move to cash, industry money fund balances will increase. With ~10% share of cash products, FII assets-under-management will be more resilient than the rest of the industry.

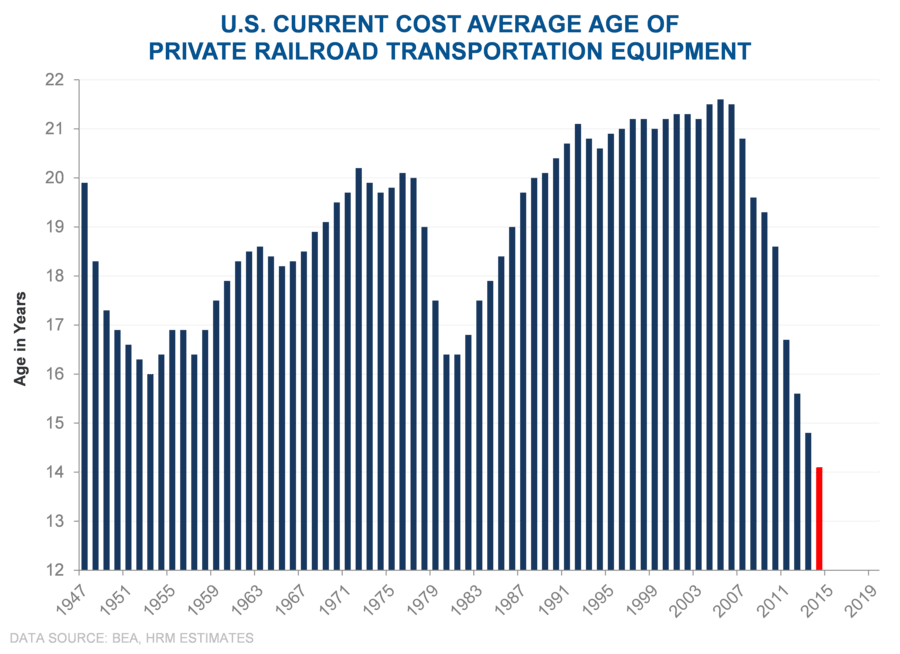

WAB

To view our analyst's original report on Wabtec click here.

Locomotives are continually being stored even while the total equipment fleet is young. Equipment heading to storage hurts Wabtec (WAB) in two ways. First, as equipment heads to storage, new equipment demand decreases.

Second, WAB’s aftermarket business is hit as their customers choose to either delay maintenance and/or scavenge for parts off of stored equipment. This is particularly problematic with slowing freight rail capital spending on equipment for 2016.

TIF

To view our analyst's original report on Tiffany click here.

Tiffany (TIF) missed yet again, blowing up the bull case that this is a great company at a defendable valuation. The forecastability of this cash flow stream is the worst we've ever seen outside of the Great Recession. If you did not think we were headed for a recession last week, you've got to give it serious credence today.

Unfortunately, in a recession TIF earnings could still go meaningfully lower (i.e. $3.00).

We acknowledge that TIF is a very good (once great) brand and company. But let's be honest...this company guided down more in the past year than it had it the preceding decade. That's hardly financial management befitting a Best-in-Breed company.

Barring a complete reset in Street numbers (down to the $3.50 range) we'll stay short.

W

To view our analyst's original report on Wayfair click here.

On Wayfair (W), management is selling high. Insider sales are nothing new at Wayfair as insiders have sold over $80mm net since the lockup expired at the end of March 2015. The chart below shows sale volume relative to the stock price. We view management's overall appetite to unload shares as a negative for the W business model long term. Insider sales accelerated in December driven mainly by higher sales from CFO Fleisher after filing a new 10b5-1 plan in November. January to date shows no signs of slowing.

We think this online only business model is one that will not be profitable in the home furnishings space in the long run. Management’s presentations may be bullish on the business model, but their trading activity points to the opposite.

RH

To view our analyst's original report on Restoration Hardware click here.

With a $1.2 billion loss in market cap since the 3Q print (-34%), the market is suggesting that things are getting downright nasty at Restoration Hardware. Bad market style factors (small cap, high beta/high short interest) have been an enormous driver here, though they come on the heels of a sloppy 3Q print when for the first-time-ever concerns were raised about promotions to drive sales. Oh yeah, all that, plus there’s a very good chance we’re heading into a recession, as our Macro team has highlighted.

Regardless of where any of us stands on the recession debate, there’s one thing that matters to RH under $60 (and even under $70) – and that’s downside earnings support.

We’re going to host a call and issue a Black Book on Wednesday, January 27th to show the stress points in the business, and where we shake out on the model. More to come next week.

MCD

To view our analyst's original report on McDonald's click here.

We remain the bulls on McDonald's (MCD) as we expect them to beat consensus estimates once again. With a full quarter of all-day breakfast under their belt, Restaurants Sector Head Howard Penney expects to see a big lift in comps. We will give you a more thorough update next week following the 4Q15 results on Monday January 25th.

FL

Foot Locker (FL) remains one of Retail analyst Brian McGough's favorite short ideas. We added the company to Investing Ideas last week. McGough will send out a full stock report early next week.

Below is a brief excerpt from a research report McGough recently sent to institutional subscribers.

"FL is at the top of our Best Ideas Short List. While our short thesis goes far beyond a few unfavorable data points, the question around timing has been a big issue for people who agree with our TAIL call, but can’t quite get there over the near term.

For many reasons, we think that $4.20 will likely prove to be the high water mark in this economic cycle, and the consensus estimates in years one through three are high by $1-$2 per share.

We think that emerging competition from its top vendor, Nike (≈80% of sales), will stifle growth, and leave the company with an earnings annuity somewhere around $3.50-$3.75 per share. Is that worth $64? Not a chance. Not for a company that is Nike’s best off-balance sheet asset. And definitely not when the Street is in the stratosphere approaching $6.00 in EPS (#NoWay)."

ZBH

To view our analyst's original report on Zimmer Biomet click here.

Healthcare analyst Tom Tobin has no new update this week on Zimmer Biomet (ZBH). Tobin reiterates his short call on ZBH, which is down -3.1% versus the S&P 500's -2.6% since the company was added to Investing Ideas in September. Remember the core thesis:

- "Employment growth slowing and fears of a recession will certainly dampen investor appetite for what is viewed as an elective procedure."

- "Our team's long-term view calls for slowing/declining unit volume and deteriorating pricing. The impact to gross margins should be significant with very little spending flexibility within the organization."

GIS

If you haven’t noticed yet, General Mills (GIS) has turned on its advertising for no artificial colors and flavors in its cereal, as well as an increased effort for its gluten free campaign.

Click here to view the 30 second spot TV commercial.

These steps taken on cereal, coupled with improved merchandise planning across their portfolio in the second half should bode well for the company’s future performance. Additionally, General Mills fits neatly into the style factors that we like from a macro point of view, large cap, low beta and liquidity.