Here's the latest from Bloomberg last night:

"At least 40 stock markets around the world with a total value of $27 trillion are in bear territory, as investors witness the worst start to a year on record."

No worries. Just buy the dip, right? Oh wait, that was Old Wall's pitch three weeks ago. Now that equities have plunged -9% year-to-date, today, the mantra is "sell everything."

That's great.

To be clear, the Hedgeye Macro team got this right before the selloff. And no, we're not getting bullish. Not yet anyway. We're still waiting for the market to fully price in our U.S. #Recession call.

#Patience...

watch this video for more on our recession call.

Upon further reflection, our proprietary asset allocation model has been largely devoid of U.S. equities and Emerging market exposure for some time. Critically, we warned subscribers to bail on U.S. equities before the July/August crash when market fundamentals were breaking down.

Macro markets aren't looking up. Going forward, investors should be wary of the Fed rate hike ramifications. Remember, Yellen & Co. are implicitly tightening into a U.S. economic slowdown.

And that's perpetuating massive market volatility, as Hedgeye CEO Keith McCullough wrote in a note to subscribers this morning:

"In prior US economic slowdowns, the Fed would A) devalue the Dollar and B) try to smash equity market volatility but that's impossible to do when tightening into a slowdown. This perpetuates the liquidity trap and with the VIX's current risk range 22-31 that’s why equity bulls are selling every bounce – they need to take down exposure to being wrong."

In other words, the Fed is trying to arrest economic gravity by calling #Deflation and the preponderance of #GrowthSlowing data "transitory" while the macro market clearly disagrees.

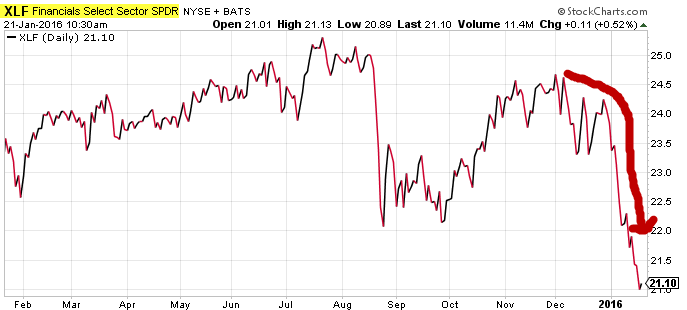

A prime example? Take a look at Financials. Here's more analysis from McCullough:

"On the margin we said the US Financials (XLF) were one of the best non-consensus shorts in 2016 as consensus was long them on the “rate hike." Well, now the 10yr is at 1.98% and the XLF led losers again yesterday -2% to -11.9% YTD. It won’t be long before consensus is begging for no more hikes, and then a rate cut."

This slow moving train wreck is bound to get more interesting.