“As soon as you trust yourself, you will know how to live.”

-Johann Wolfgang von Goth

Who do you trust? In both your personal life and profession that’s one of the most important risk management questions there is. If you trust the un-trustworthy, you will ultimately pay the price for that. If you trust the trustworthy, you’ll have peace of mind.

For starters, do you trust yourself? Depending on what it is, I assume the answer should often be no. Would I trust myself operating on a loved one? No. I’d look for the most competent and trustworthy professional in the world for that.

Alongside your health, I’d say your wealth ranks right up there. So why put so much blind faith in the Davos Establishment and its conflicted and compromised banking, brokerage, and media sources to tell us what we should do next? I don’t know.

Back to the Global Macro Grind…

Saying “no” and “I don’t know” are two liberating exercises. If you wanted to say “yes” to buying every crash/dip, you’ve had every opportunity to try that for the last 6 months. You’ve also had plenty of chances to say, “hold on, I don’t know what’s going on here.”

I’m not your shrink. I’m not going to take a victory lap this morning either. With global stock markets finally catching up to crashes we’ve trusted as “non-transitory” in currencies, commodities, and credit (for the last 12-18 months), it’s time for me to take a knee.

Some of you may not like that. Many of you like it when I run the ball right up the middle on the Old Wall. But we’ve arrived at the part of the game where a lot of people are getting hurt. If they keep getting hurt, they’ll eventually hurt you.

Here’s what’s going on this morning in global equity markets:

- Russell 2000 closed down another -1.2% yesterday, taking its crash to -23.2% vs. its July 2015 peak

- Russell 3000 (98% of US listed stocks) now has an average peak/trough crash (per stock) of -35%

- Japan’s Nikkei moved into crash mode overnight, dropping -3.7% (deflation of -21.2% vs. its July 2015 peak)

- Singapore’s stock market dropped another -3% overnight, taking its crash to -27.4% since its April 2015 peak

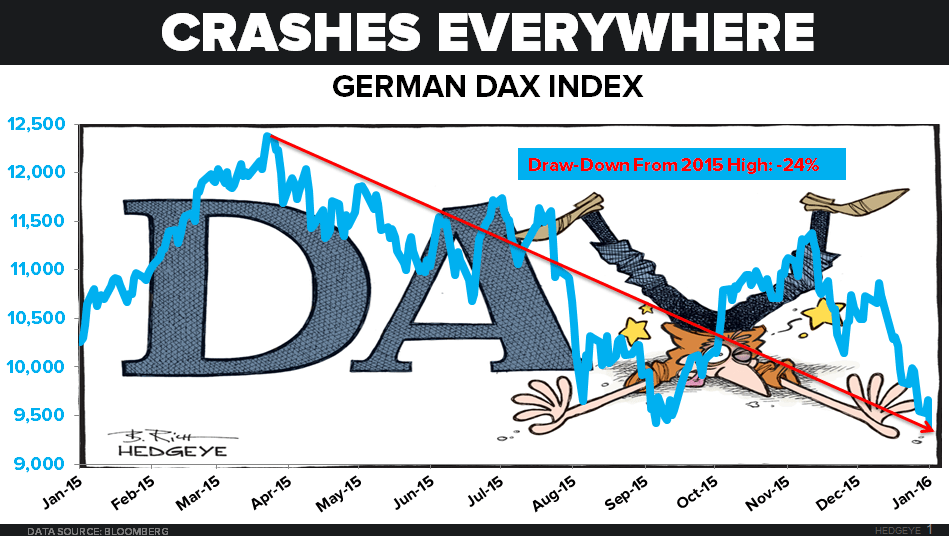

- Germany’s DAX is down another -2.7% this am, taking its crash to -24.2% since its April 2015 peak

In other words, from USA to Asia to Europe, major stock market corrections have turned into crashes. And the only way to get this over with faster than slower is for consensus to wake up to trusting what Mr. Macro Market has been signaling all along.

Put another way, once we can all trust that the establishment sees what we all see, we move from the end of the beginning to the beginning of the end. And we’ll stop with the nonsense of calling trustworthy economic and market sources “peddlers of fiction.”

As they say in Thunder Bay, the fish rots from the head down. And that’s why it’s important for our said “leaders” to start telling the truth about what’s going on in macro markets and economies, as opposed to what their political agendas want us to think.

Instead of the Political Class, let’s check in with business people on this:

- American CEOs – “confidence hit a 6yr low” in the most recent Price Waterhouse Coopers CEO survey. Only 35% of CEOs were “very confident that revenues would grow in the next 12 months.” (lowest confidence interval since 2010)

- US Homebuilders – with a 60 reading yesterday, the NAHB (National Association of Home Builders – one of the largest trade associations in the USA) reported its 3rd straight monthly decline in builder confidence (the cycle peaked in OCT 2015 at 65)

- US Investors – US Equity Volatility (VIX) is +43% YTD and +136% since US corporate profits peaked at the end of Q2 2015. Meanwhile, long-term bond yields (10yr = 1.97% this am) are hitting their lowest levels since the “rate hike”

I don’t care which Presidential candidate the manic media gets ratings from or who they vote for. Until centrally-planned otherwise, CEOs, builders, and investors in this country still have the free market liberty to vote with their wallets, every day.

I trust their collective confidence on that.

For all of today and tomorrow I’ll be meeting with Institutional Investors in both Boston and New York. These have been very difficult times for many, and my hope is that our risk management #process starts helping more than a few.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.94-2.10%

SPX 1

RUT

Nikkei 162

DAX 9

VIX 21.30-29.87

USD 98.35-99.81

EUR/USD 1.07-1.10

Oil (WTI) 26.95-31.63

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer