In terms of both economic data and macro market read-throughs, last week was really ugly. The reality is that it was the worst start in history for U.S. stocks. Ever.

Well, for equity investors at least, not Hedgeye subscribers.

Our subscribers were spared the August equity market drubbing and the most recent market rout as our contrarian Macro team has been way ahead of consensus warning about ongloing risks including #Deflation and #GrowthSlowing.

In other words, we made the call.

Hedgeye CEO Keith McCullough dissected last week's data and the resulting financial market reverberations in a note sent to subscribers this morning:

"Let’s not forget we had a trifecta of “misses” on Friday with Industrial Production and Producer Prices (PPI) in recessions at -1.8% and -1.0% year-over-year, respectively (and control group for Retail Sales only +1.5%). The U.S. 10YR Yield broke 2.0% intraday (and should have on that data) and GDP is a lot slower than consensus (our favorite Macro Long idea remains the Long Bond)."

Meanwhile, equity markets ripped to the downside, in all but one sector, Utilities (XLU) (which just so happens to be the one sector that we like.) Here's additional analysis from McCullough:

"U.S. Equity Sector Styles continue to reflect #Recessionary expectations accelerating, with Utilities (our favorite sector currently) +0.7% last week (+0.3% year-to-date) and Basic Materials -4.5% on the week (-11.9% year-to-date) and Financials -3.1% on the week (-10.1% year-to-date) underperforming what’s an already -8.0% year-to-date S&P 500."

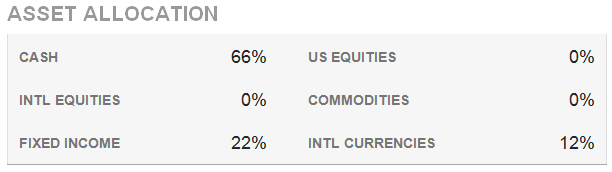

The fizzling in U.S. equities doesn't surprise us at all. Here's an inside peak at our proprietary asset allocation model which has been largely devoid of U.S. equities since last July.

Bottom line: We're going to ignore consensus and stick with our process. It's working.