“A leader must be a true believer in the mission.”

-Jocko Willink

I didn’t win Powerball last night, so I’m back at it, peddling non-fiction to Obama’s “folks” at the Fed this morning.

In all seriousness, like many of you, Laura and I had a Powerball discussion with our kids at the dinner table last night. Laura told them that “if we won”, we’d keep it anonymous and donate a large part of it to charity. The kids liked that.

Yes, I know. A certain type on the Old Wall is all about the money. And a mother’s moral lessons to her children can sound idealistic. But the reality is that a lucky ticket wouldn’t have changed the mission we’re on this morning. As parents, we’re already winning.

Back to the Global Macro Grind…

As a parent, coach, or professional (or anyone in any position of leadership) our goal should always be to be on a mission – one that we can feel in our bones – one that we truly believe in. As Navy SEAL Jocko Willink went on to write in Extreme Ownership:

“Leaders must always operate with the understanding that they are part of something greater than themselves and their own personal interests. They must impart this understanding to their teams.” (pg 76)

I realize I am as flawed and fragile as any other human being. Without the blessing of good health, everything I’ve ever “wanted” can be disrupted. That’s why, every day, I re-commit to being part of something that’s a lot bigger than I’ll ever be.

Back to the belief system of a Powerballer…

A lot of people played who have never played. Why? If you’re not in it, you can’t win it. But it was also a cultural craze that transcends the bubble in “wealth.” From “internet stocks” to housing, we’ve had plenty of bubbles pop in the last two decades. This one will too.

Some people play Powerball because they want a short-cut. They’ll gamble their kids meal money away for the hope of a better life. I don’t judge that. People have wants and needs. But we also have a culture that is fixated on cheap leverage.

“Cheap” leverage has a ton of downside if the principal investment goes to zero. When I think about all the mistakes I could have made in the last 6 months, the biggest one would have been getting sucked into “missing the move” in a lottery stock.

Fortunately, saying no to gambling, drugs, and leverage is a choice. Together, many of us made that choice.

To review the biggest catalyst for a US stock market crash:

- The perception that “0% rates” = 0% risk is a centrally planned fraud

- Real risk is measured in terms of both volatility and credit spreads

- As #Deflation becomes pervasive instead of “transitory”, both volatility and credit spreads breakout

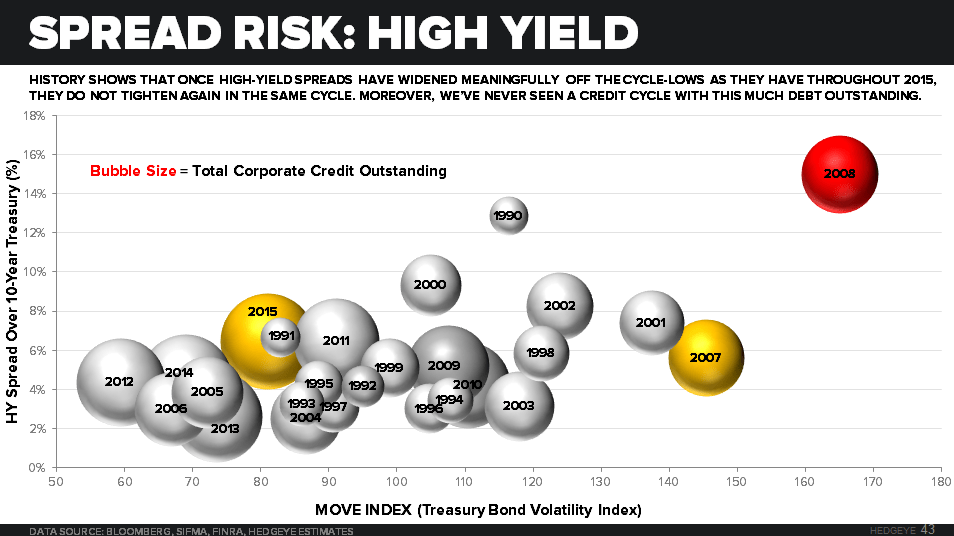

As you can see in the Chart of The Day, the volatility of levered investments is starting to move up and into the right of this 3-factor SPREAD RISK chart:

- High Yield Spread (over 10yr Treasury) = y-axis

- Bond Market Volatility (MOVE Index) = x-axis

- Total Corporate Credit Outstanding = Bubble Size

History shows that once High Yield Spreads have widened meaningfully off the cycle-lows (as they have for the last 7 months), they do not tighten again in the same economic cycle.

Moreover, we’ve never seen a Credit Cycle with this much debt outstanding. This is the biggest corporate credit bubble in human history and leverage, as we all very well know, can amplify returns in both directions.

So, if you’re looking for reasons why the German stock market (DAX) and Russell 2000 (IWM) are in crash mode (down -21-22% from their cycle peaks in April-July of 2015), the combination of:

A) LEVERAGE (most equity hedge funds run 150-250% gross invested to lever up low nominal returns)

B) LIQUIDITY (lots of hedgies own the same small-mid cap stocks; when they go down fast, they can’t get out)

I’ve never been a fan of levered-long strategies – especially at economic cycle peaks. Personally, I don’t believe in levering myself up with assets I can’t afford either. But that’s just me – the guy who spent $5 on Powerball, just for fun.

It’ll be fun putting those tickets in the garbage this morning. My mission is not to have you chase charts, buy high, and hope that stocks never go down. Like bonds, they go up and they go down. I’m a big believer in a risk management process that goes both ways.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.04-2.18%

SPX 1

RUT

VIX 21.19-29.21

Oil (WTI) 28.61-33.52

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer