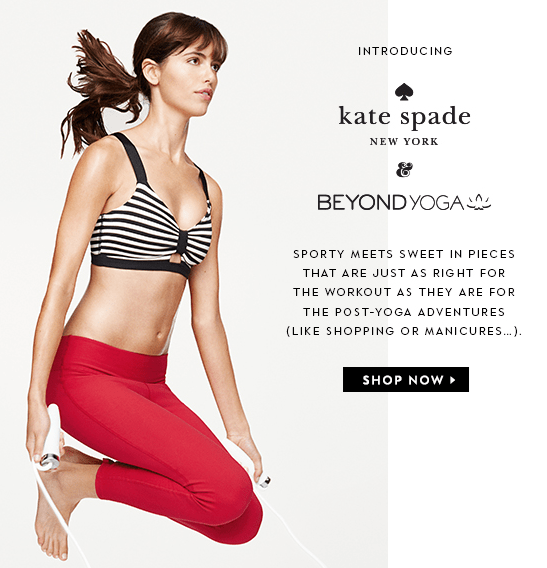

KATE - Yoga Partnership Out. Like the Setup For 2016

KATE rolls out new yoga line in partnership with Beyond Yoga. Just one of two handfuls of licensing deals that will be incremental to 2016. That's just one of the drivers of an accelerating top line we expect to see in 2016. Not only do the reported headwinds roll off in the new year (Jack/Saturday closures, SE Asia JV, quality of sale initiatives, etc.), but KATE has a lot of incremental drivers on the top line. Licensing, international growth through distributors/JV, and a flat promotional posture after working to improve quality of sale through all of 2015.

We think timing here is absolutely critical, and that timing finally favors the long side. Keep in mind that this company has been a serial restructurer, having traded under three different tickers in five years, and the only constant during that time period has been a lot of red at the bottom of the P&L. Even though KATE has been executing extremely well on its plan, the fact is that the stock has looked extremely expensive to the average investor who cared about nothing but current year earnings. This is why the stock got annihilated when the category (Kors) hit a wall. It simply had no valuation support. That’s why we think that the quarter we’re currently in (4Q), will be critical, in that the company should earn 30% more than it did in all of 2014. In fact, we’re a few short months away from people focusing on $1.00 in earnings power for next year – a level it hasn’t seen since 2007. People will be looking at a name trading at 17x an earnings rate that should grow 50%+ for 3-5 years.

HIBB - Roll Tide

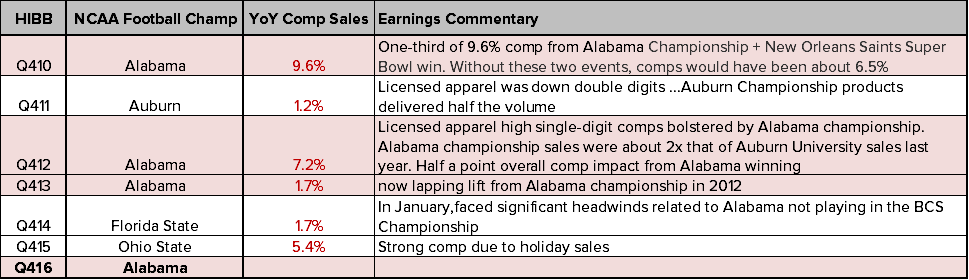

This is the only retailer we can think of that actually has a material comp benefit when its local team wins big. Bama winning it's 4th National Championship in 7 years last night could at most add 1.5% in comp for the company's 4th quarter. We saw the same benefit in 4Q10 and 4Q12, and the store weight on Alabama hasn't changed materially since then, with Bama representing 9.1% of the store base at the end of FY15 vs. 10.3% at the end of FY10. But, there are two things to keep in mind…

1) HIBB is up against a 5.4% comp from Holiday of last year, its best comp number in over 3 years.

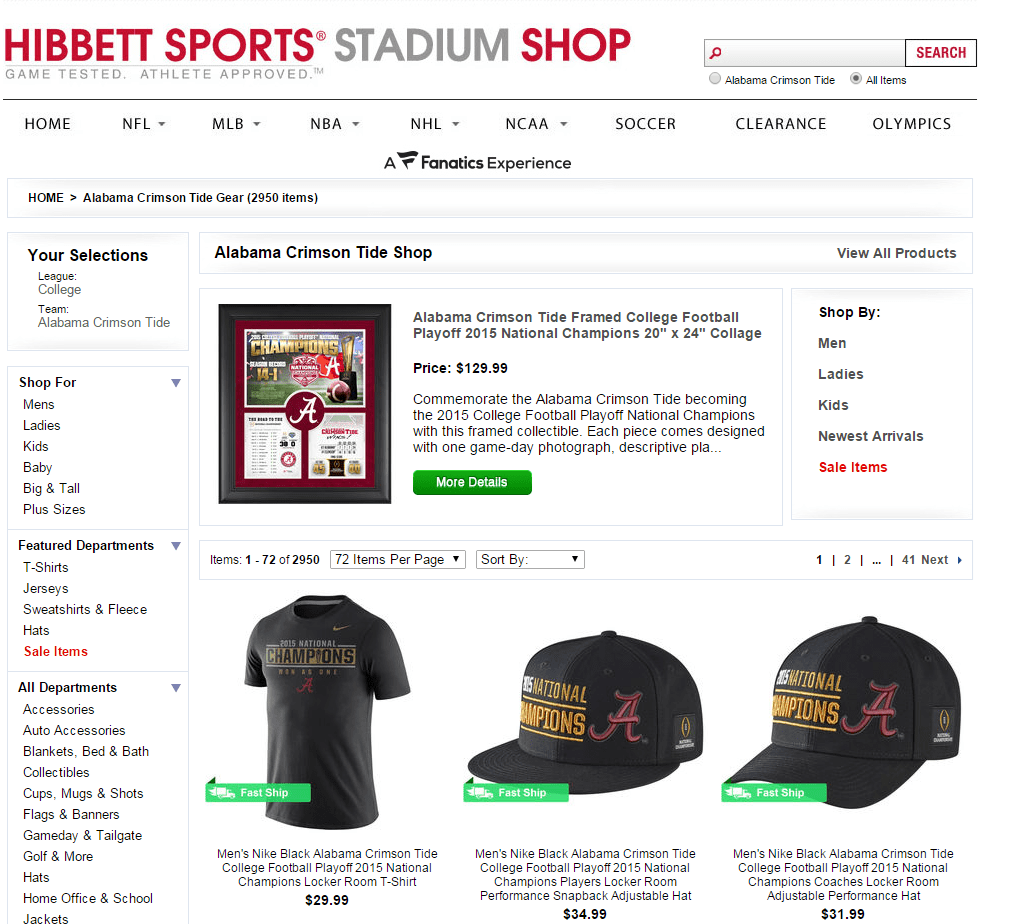

2) Want to buy your Bama gear on Hibbett.com, well consumers are in luck, except that Bama's website isn't serviced by Hibbett but Fanatics (see image below). Logically it would make sense that the lack of an e-commerce presence wouldn't hurt HIBB materially for merchandise that consumers want now, but it will be interesting to see how consumers vote with their wallets. Either by driving 5miles to a HIBB store, or ordering from dickssportinggoods.com.

LULU - Beat Expectations. Low Earnings Quality

The old guide down and beat lowered expectations before the company gets on stage and in front of Investors at ICR. The mid-point of the guide on the top line is just $2mm higher than where consensus stood before the company lowered the bar for 4Q in its 3Q earnings release just one month ago and the mid-point on the earnings guide is $0.07 lighter on a lower share count, which means lower margins. Since then, the stock has appreciated 15% taking the multiples from 23x P/E and 12.5x EBITDA to 28x P/E and 15.5x EBITDA on lowered 2016 numbers. Maybe investors are looking at the Street's implied 19% earnings growth for FY16 (after 2 years of down earnings) in the context of the broader retail landscape where its tough to find a double digit grower in 2016. But, we'd argue that the expected growth is more than priced in at this point.

In the out years, numbers have come in by 10% since the company reported 3Q15 earnings. Still high by $0.50. Ultimately, we think LULU will miss again, and then again - until the ‘new’ CEO is likely to be out of a job. Spin it any way you want, but he's just not right for that job in that culture. Until then, LULU is marching towards $2.50 in EPS with the Street at $3.00. We still think it’s a short.

UA - UA signs the mother of all deals. Yale at 10 years/$16mm (vs. Notre Dame at 10 years/$90mm). Maybe we are a bit biased.

NKE, DIS - Mark G. Parker Elected to The Walt Disney Company Board of Directors

WWW - Wolverine Worldwide Names Pat O'Malley as President of Saucony Brand

(http://phx.corporate-ir.net/phoenix.zhtml?c=88408&p=irol-newsArticle&ID=2128332)

BKS - Barnes & Noble names Mary Amicucci as its new head merchant

(http://www.retailingtoday.com/article/barnes-noble-names-new-head-merchant)

Joyce Leslie, a 47 store women's clothing chain located in the northeast, filed for Chapter 11 and is a likely candidate for liquidation

(http://www.chainstoreage.com/article/young-womens-apparel-retailer-files-chapter-11)

NKE - Nike Unveils Cleat For FIFA Women’s Player of the Year Carli Lloyd following U.S. 2015 World Cup win

AMZN - Amazon reportedly scaling down its Echo device to size of a 'beer can'

Christmas sales in the UK "disappointing", growing just 1% in December

(http://uk.reuters.com/article/us-britain-retail-brc-idUKKCN0UQ0OM20160112)

APP - Dov Charney Seeks to Block American Apparel Bid to Extend Exclusivity Period

(http://wwd.com/business-news/legal/dov-charney-block-american-apparel-bid-exclusivity-10311796/)