FINL announced yesterday that it would be closing 25% of its existing fleet over a 4 year time period. That’s gross closures as the company will be working on the quality of its real estate portfolio to increase its penetration in better quality malls, i.e. more overlap with FL in better markets. What we know – each of the 150 stores earmarked for closure are doing about 1mm bucks per store, about 50% below the company average of $2mm. 65% of those sales are attributed to FINL loyalty members.

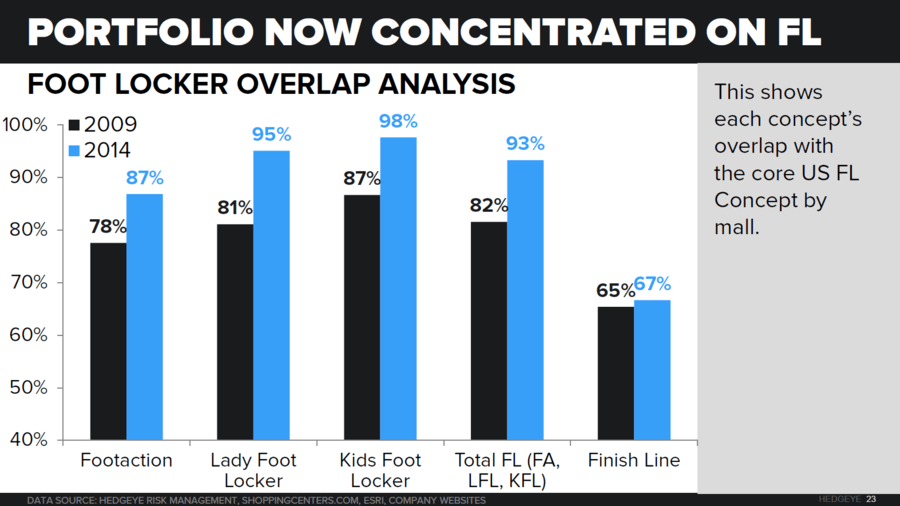

If we look at the store footprint overlap by mall between Foot Locker (banner) and Finish Line it’s only 67% (chart 2 below). And our sense is, there is more overlap on the top end of the spectrum compared to the bottom end where FINL will be closing locations. That’s because FL has been extremely prudent over the past 5 years as it stripped capital out the model by rationalizing its store footprint.

All in we get to a $0.03 benefit to FL’s bottom line, and $20mm to the top line per year through FY19 from the door closures assuming a high overlap ratio between the store locations. Less than 1% accretion per year. To get there we assume that FINL recaptures 40% of the lost sales, and 80% of the forfeited share shifts over to FL. We assume a 30% margin for dollars transferred, as FL won’t have to spend up dramatically to win those $. Worst case, assuming FINL recaptures 0% of the dollars lost, and FL gets 100% (ain’t going to happen as NKE pushes its DTC agenda), we could see a $40mm benefit to the top line and $0.06 on the bottom about 1.5% of earnings growth.