WisdomTree announced a suite of dynamically hedged ETFs yesterday. In concert with its main currency hedged Japanese fund the DXJ, and the Euro-zone ex. Euro ETF, the HEDJ, the firm has launched 4 new products. The firm is now adjusting an "always on" FX hedge (on the HEDJ and DXJ) to a rules based approach that will dynamically apply and remove the FX hedge depending on market conditions. These latest products have been launched on European equities, Japanese equities, small cap foreign equities, and a broader international equity fund (see WETF info HERE). The latest information on the firm's website outlines the following new rules based approach for the new "dynamic" FX hedge:

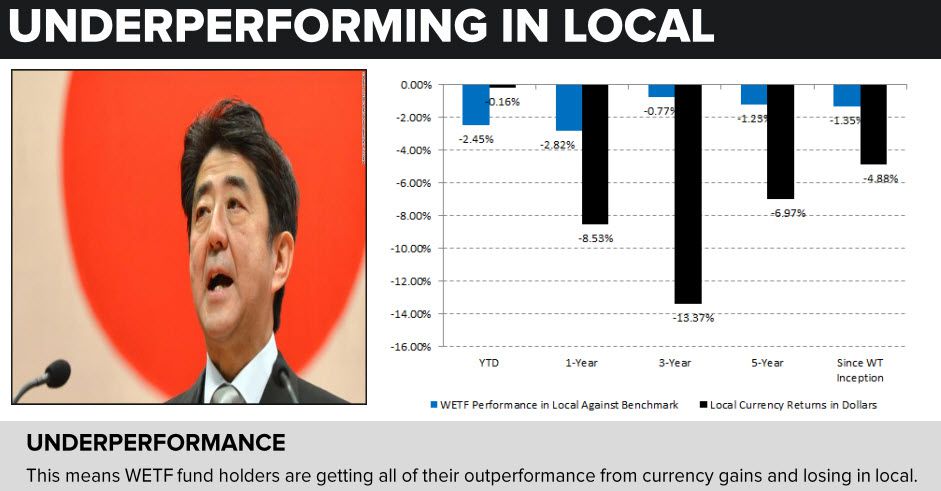

While dynamically hedged products allay some of our concerns that historically, local currency exposure has been beneficial for foreign investors (and thus the FX hedge nullifies important returns), we remind investors that the HEDJ and DXJ underperform in local currency outside of the FX hedge because of a beta construction issue. Both DXJ and HEDJ construction is weighted by dividend paying stocks, with also favorable weightings for export driven companies. This benchmark construction thus far has proven to underperform standardized benchmarks in local currency.

The main issue with the new dynamically hedged products is that the WisdomTree products underperform in local currency outside of the FX hedge (in both Japan and Europe).

Thus it's a double edged sword with the WisdomTree's hedged FX products as the FX hedge has been the source of most of the ETF's returns recently for both the DXJ and the HEDJ:

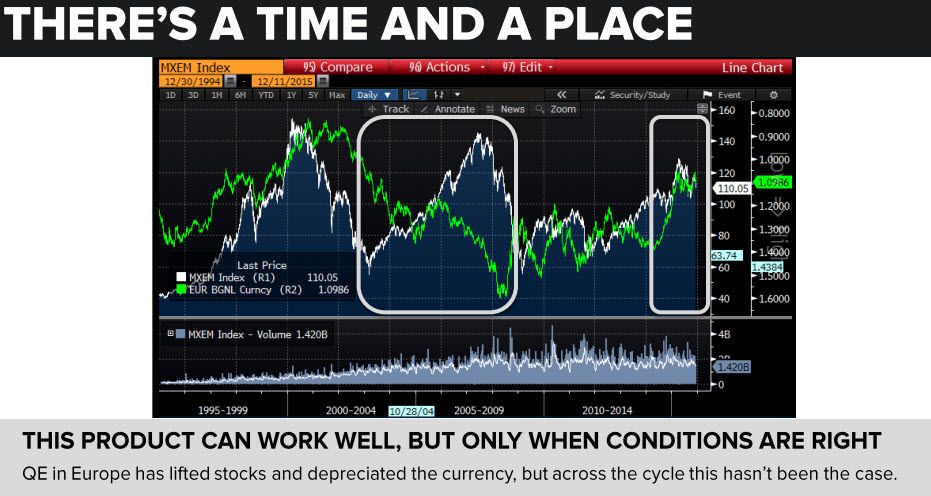

But there are plenty of historical references that foreign investors would have benefited from having local currency exposure (see first grayed boxes versus the second grayed periods).

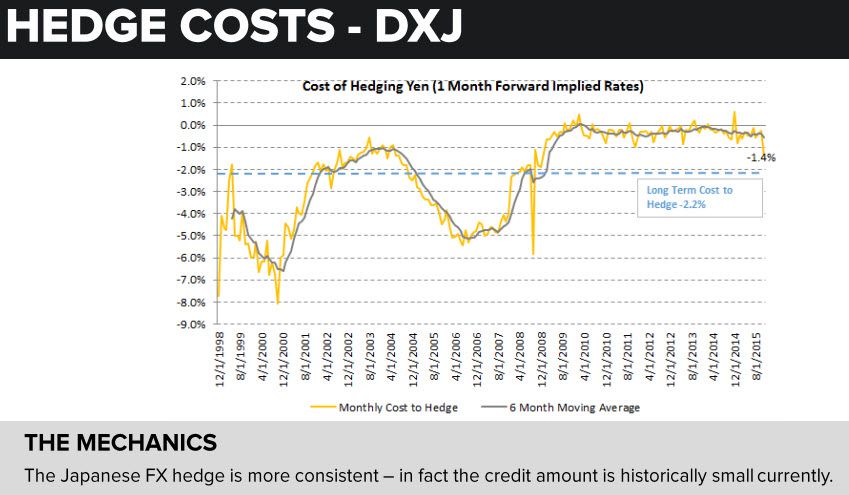

The last question on the new dynamically hedged products is will overall fund returns suffer when the hedge comes off. Currently the hedge ADDS credits or returns to fund holders out of the gate as overnight interest rate differentials and liquidity pay the manager to undergo the FX hedge:

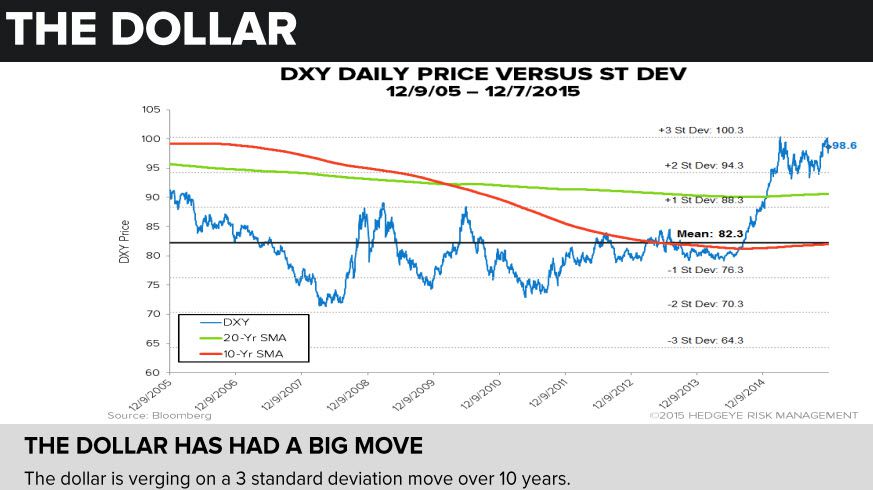

Dynamically hedged ETFs could be signaling our view that the U.S. dollar move higher has already experienced the bulk of its move. Our main basis for this stance is that the dollar has already made a 3 standard deviation move over a 10 year period and is also bumping up against its historical 20% year-over-year rate of change ceiling.

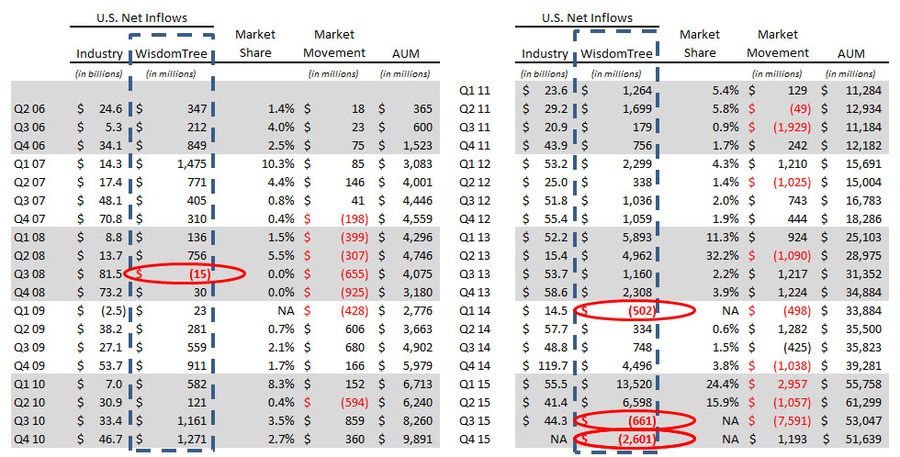

WisdomTree trends are inflecting negatively with the firm just having put up its worst quarter from an asset raising standpoint in 4Q15 with a $2.6 billion redemption (and an unprecedented second consecutive quarter of outflows in the firm's now 9 year history). Prior to 3Q and 4Q '15, the firm only had redemptions in 3Q 2008 and 1Q 2014. Trends accelerated to the downside to finish 4Q15 to boot with the HEDJ and DXJ losing $3 billion and $2 billion respectively in the last 10 business days of 2015.

We think 2017 estimates (the best way to value this growth stock) are implying an unacheivable ramp in the firm's AUM to over $80 billion from the current tally of ~$50 billion. This assumption supports the Street's estimate of $0.97 per share. Our estimate of $0.79 per share is supported by a slower ramp to just over $70 billion.

WisdomTree shares continue to trade ahead of median takeout multiples implying further downside. We think shares start to look attractive at $10 pending no substantial degradation of recent trends. We hosted our best ideas Short call on December 17th with the stock at $17.30.

WisdomTree Best Ideas Short - Not So Smart Beta

Please let us know of any questions,

Jonathan Casteleyn, CFA, CMT

Joshua Steiner, CFA