Below we offer three different conclusions to supplement the credit-cycle section in our Q1 themes deck:

- Planned capital spending cuts are only the first leg of the capital flush needed in commodity related sectors.

- There is a gross excess of capital chasing current production levels, and this excess greatly overshadows the near-term effect of planned capital spending cuts – The market needs an extended period of underinvestment to reduce the excess capital deployed.

- The non-GAAP reporting splurge should get worse with impairments and write-downs as the back side of the cycle plays out.

----------

We outlined the risk that is beginning surface in credit markets in the themes presentation. Coming off the summer 2014 lows in spreads and volatility, credit spreads are now widening on an unprecedented amount of corporate credit outstanding.

Moreover, commodity producers in mature industries have chased inflation expectations with free money to gain a much larger share of this expanding ‘debt pie’. One rhetorical question that we’ll ask with regards to monetary policy’s attempt to create inflation post-crisis:

Has monetary policy, in its attempt to create inflation, actually perpetuated deflation? Or, taking the policy discussion off the table, have inflation

expectations from producers created deflation?

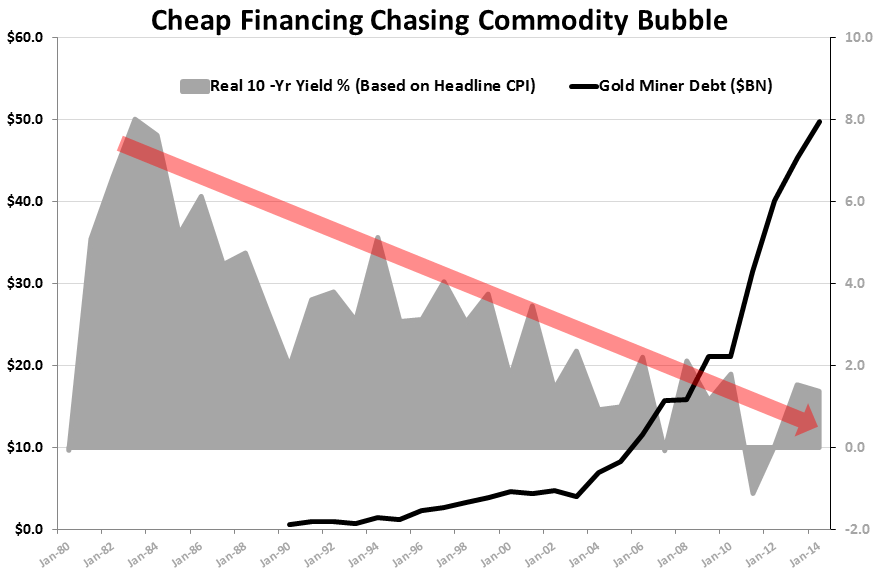

The answer is elusive, but we can probably make at least one conclusion: Free-money policy harvested a credit binge from commodity producers anchoring on higher prices:

Investment banker A says “don’t bother predicting commodity prices. Assume today’s prices (at the highs) and model the economics of digging a hole, pulling something out of it, and selling it. Then we can pitch this free money capital raise to Company X” - Leverage yourself up, and undertake projects at peak margins while everyone else is doing it.

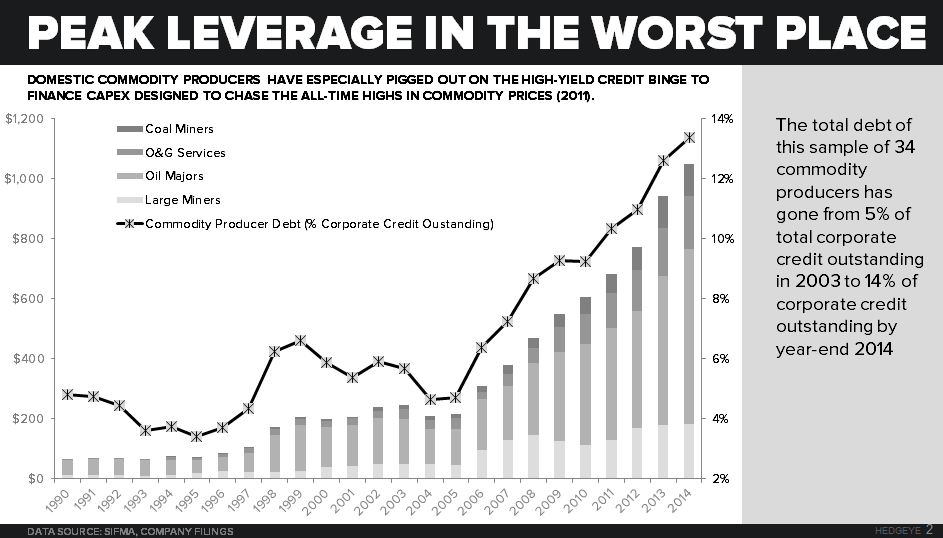

Using a sample of 34 different producers in 4 different subsectors, commodity producer debt as a % of corporate credit outstanding has multiplied ~2.5x in 10 years. This group’s aggregate debt level is up ~5x in 10 years. The chart below shows the jump in commodity producer debt as a share of aggregate corporate debt levels.

To help illustrate the height of the leverage problem as rates move wider, the chart below shows interest expense charges for that same group of 34 producers. Every interest rate cycle since coming out of the early 1980s has led to lower lows in rates, and near the lower bound in rates commodity producers splurged.

Even though a bulk of the financing happened near this lower bound, interest expense has gone straight up over the last 10 years.

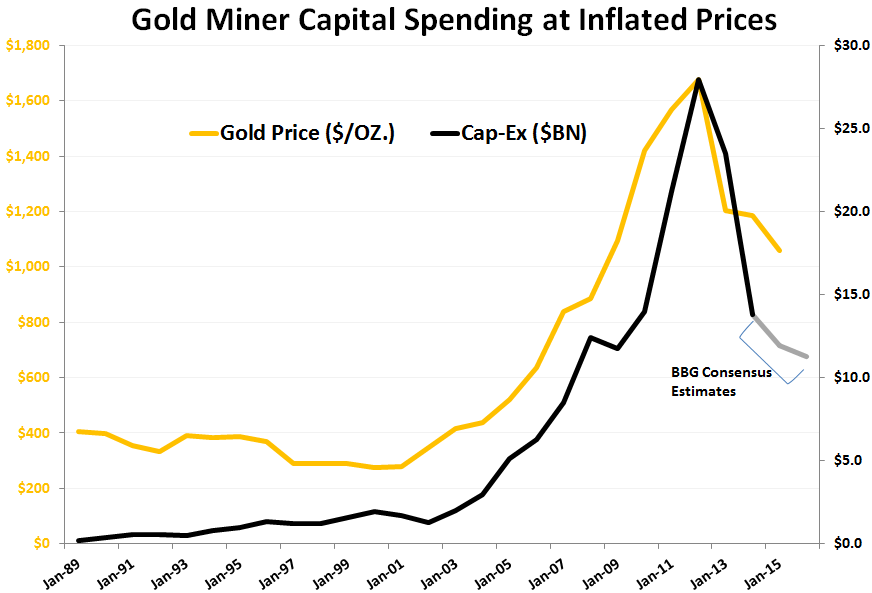

Looking at three completely different markets (Energy, Gold Mining, and Potash), these price chasing charts paint the same picture. Projects look attractive to all of the same people at the same time at peak margins:

With one of the conclusions in the deck yesterday being that the deflation sewing investment splurge has taken credit markets to peak leverage, the cyclical bubble charts below show that the move off the low in rates and volatility of mid-2014 is in transit.

And now that spreads are widening, the leverage problem worsens. Once credit spreads begin to widen for an extended period of time, they don’t revert within the same cycle without the commencement of a recession.

A key call-out to monitor with regards to balance sheet trouble with spreads now moving is that a large amount of credit in the commodity space is on the edge of high yield even though much of it still trades like investment grade credit. Looking at a number of large producers in our sample of 34 companies above:

- 9 of the larger producers have $211Bn in credit outstanding that could be tiptoeing the high yield line by late 2016 (arguably longer for BHP and Rio Tinto, but our macro view is not in their favor). That $211B is nearly 3% of corporate credit outstanding

- Several IG credits trade like high yield is inevitable

- 5 of the 9 listed below are on negative watch by Moody’s

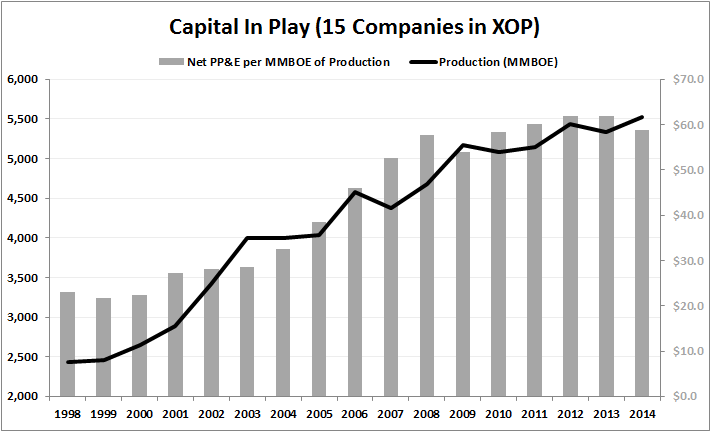

To conclude with the most important point of the note, the capital in play chasing each unit of production is excessive and is just beginning to inflect. As mentioned at the top, the market needs an extended period of underinvestment to flush at the excess capital deployed per unit of production across the space, with energy and gold mining exemplified below:

While we look at the delta in aggregate capex as an indicator of capacity coming online, on the unwind, looking at capital in play or capital on balance sheet for every unit produced may be the best metric to gauge the flush.

There is still way too much capital chasing every unit produced, especially when considering the empirical evidence to support that, in general, producers have gotten better and more efficient at producing commodities over the long haul. The supply-side backstop that builds the foundation for a favorable long-term outlook for these businesses takes time to surface.

Ben Ryan

Analyst