Hedgeye initiated Materials coverage in Q4. Below, we outline the thesis on Newmont Mining. Please email or if you have more interest in the team's work.

----------

Overview

We hosted a Black Book call on December 22nd to outline our thesis on Newmont Mining. This presentation builds on our November ‘Gold Flush’ Black Book, which outlined a broader bearish thesis for the commodity. Please ping us back at or reply to this email, and we’ll send along the Presentations and Replays for both black books. We can also send our EQM Data Set/Model with the data behind our charts and other background.

Takeaway: We expect shares of NEM to trade toward $10/share amid continued gold price pressure, an inability to repeat prior reported production cost declines, and a return to a pre-commodity boom valuation profile.

Highlights

Gold Not Low, NEM Not Cheap: Gold prices are not even close to low by historical standards; a move away from negative real rates in a disinflationary/Fed tightening environment may prove unhelpful. Gold prices are highly dependent on investor purchases; investor purchases are holding their historical relationship to gold and trending lower with prices.

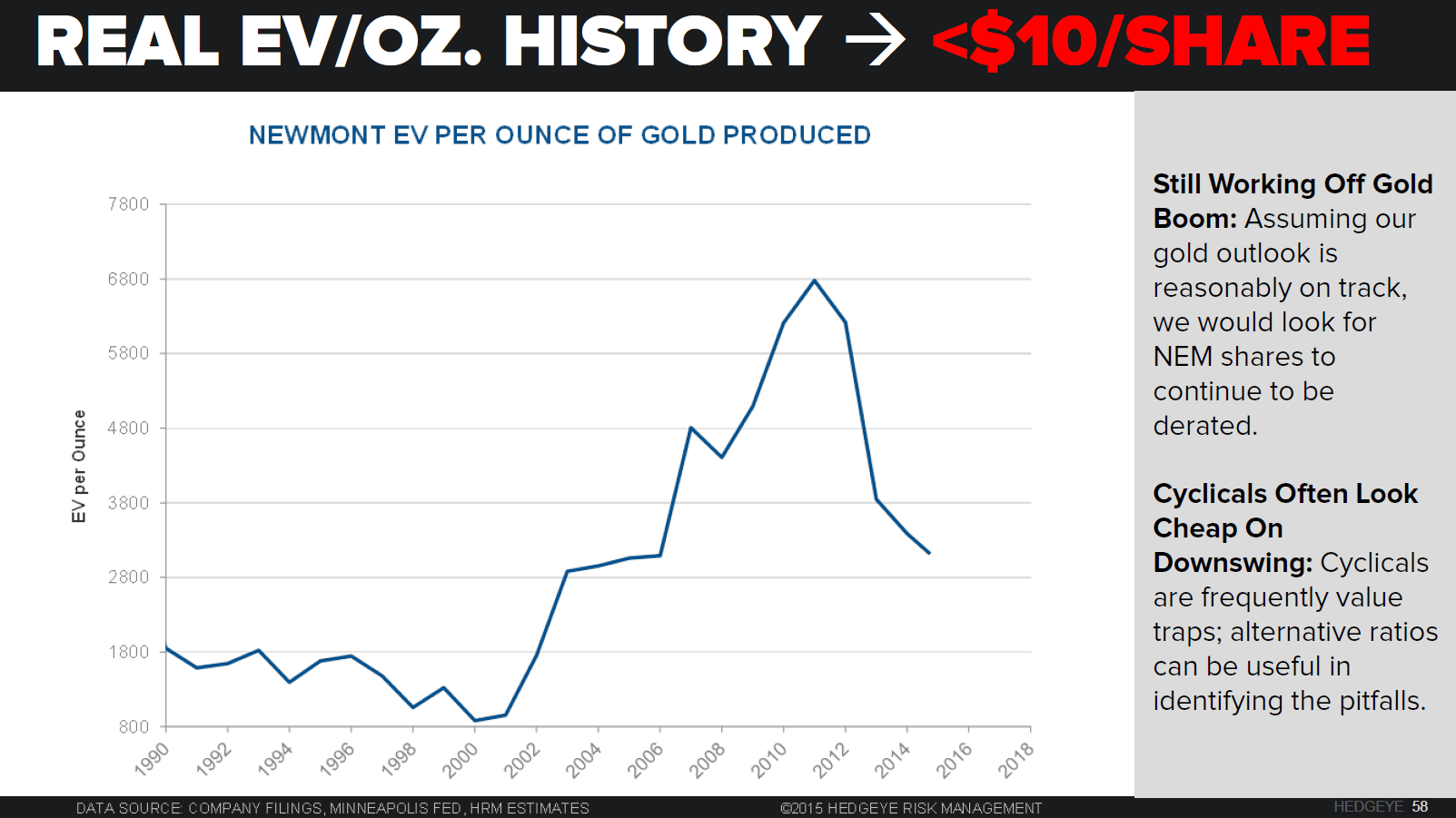

- Commodity Value Trap: Newmont, like many mining companies, has been a secular underperformer over the longer-term. Shares of low P/E cyclicals in an ongoing downcycle are typically ‘value traps’ that look cheap while continuing to underperform.

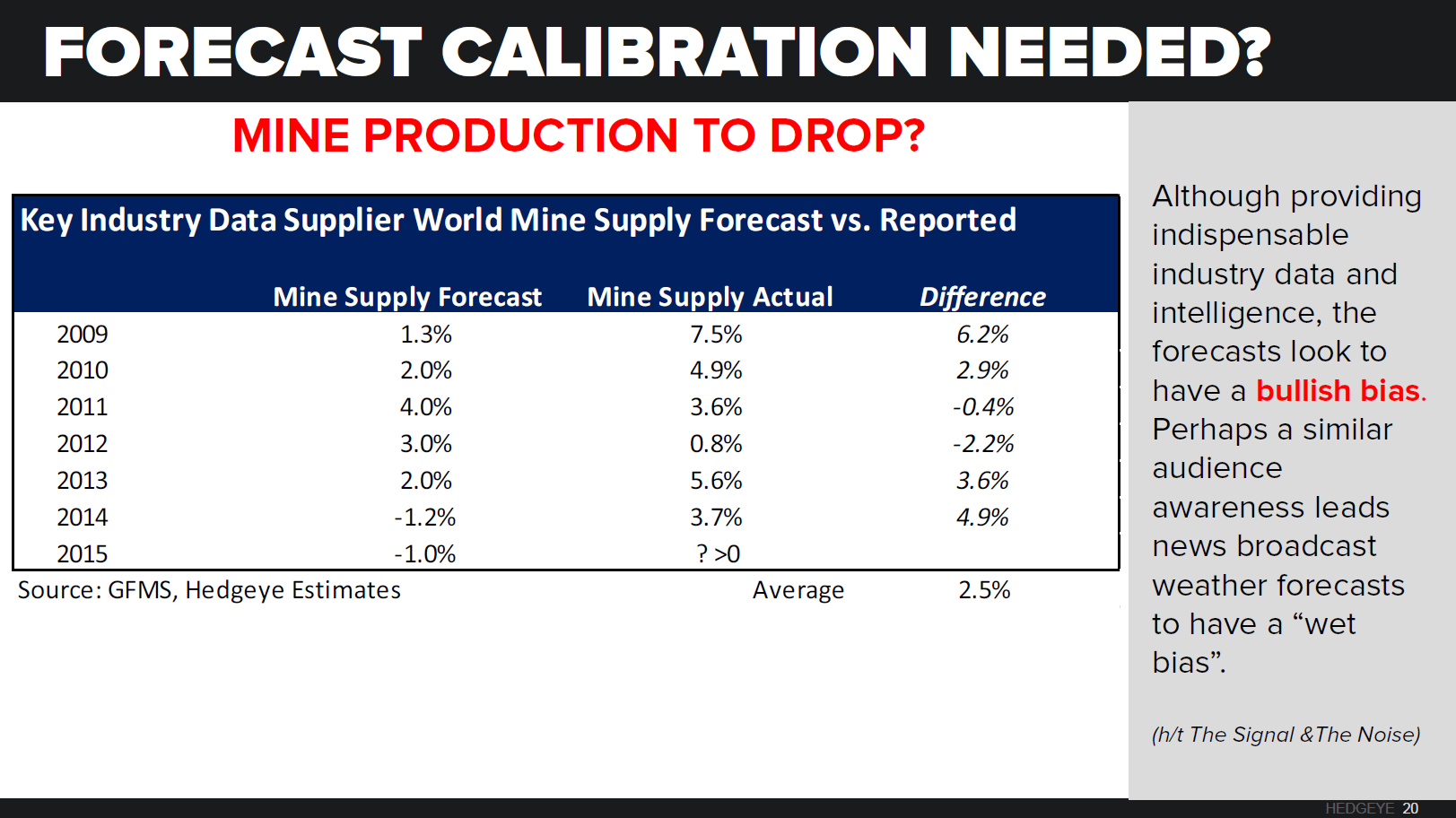

- Expectations For Gold Mine Supply Drop Misguided: Mine supply has historically been underestimated by consensus forecasters. We expect ongoing mine supply growth in 2016 and 2017.

- Newmont Higher Cost Producer, ~$800 Gold Price Would Be A Major Problem: NEM is a higher cost producer with known assets. We expect the company to struggle relative to competitors in the lower gold price environment.

- Cost Progress Not Credible Per HE Adjusted AISC: We believe that NEM’s lower cost profile has partly come from capitalizing costs based on an excessively bullish long-term gold price assumption. Gold is not near the $1,300/oz. assumed in the company’s stockpile assumptions, for example. While not necessarily inappropriate from a disclosure/accounting perspective, the imbedded above market price assumption nonetheless provides an economically unrealistic view of NEM’s production cost profile, as we see it.

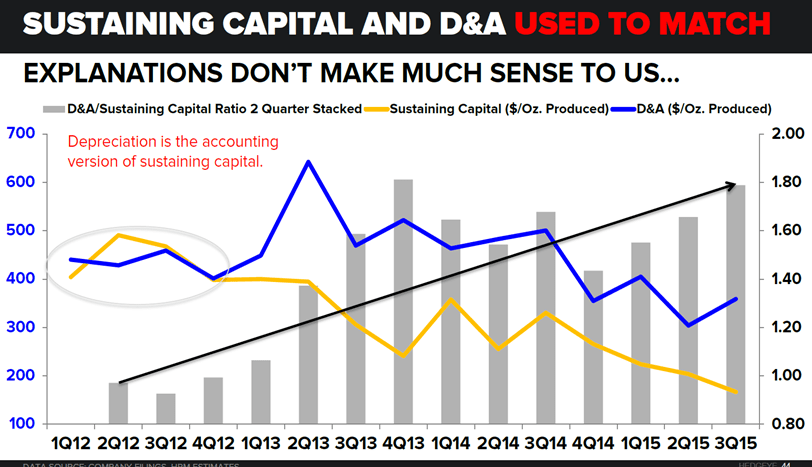

- Dubious Sustaining Capital Cost Cuts: Another component of the drop in NEM’s All-In Sustaining Cost (AISC) has been lower “sustaining capital” expense. However, the concept behind this slippery metric is already captured in accounting by “depreciation”. Not surprisingly, sustaining capital at NEM historically roughly matched depreciation expense. We do not see these cost reductions as credible since explanations for the subsequent deviation, such as longer mining truck tire life, should either be captured in depreciation or viewed as temporary deviations between cash and accrual metrics.

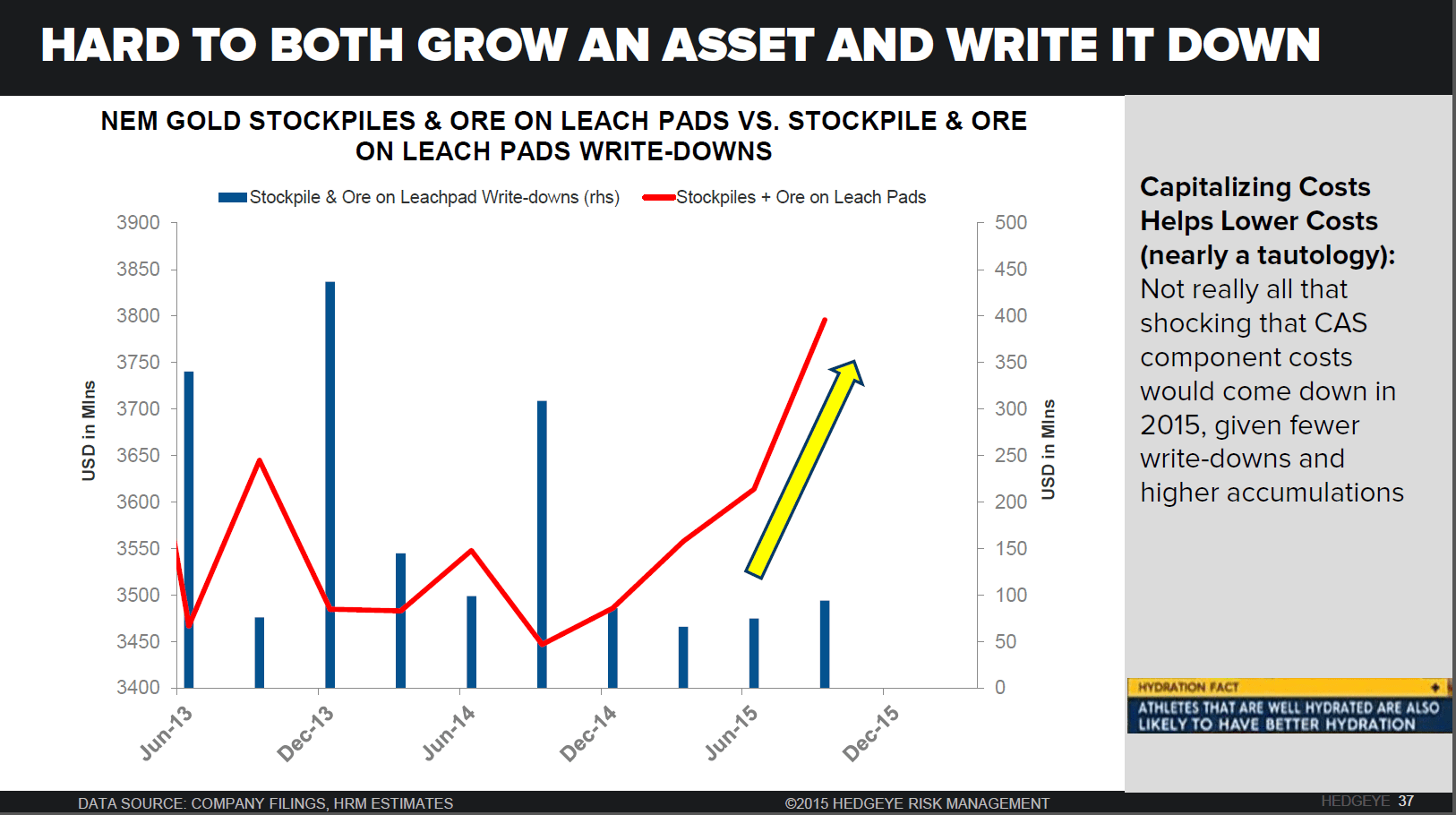

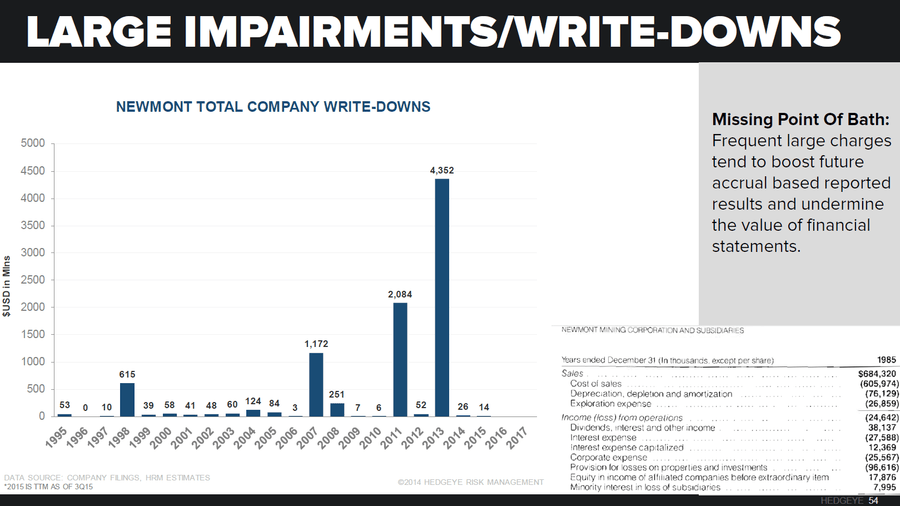

- Another Large Charge With 4Q15 Results: Frequent large charges tend to boost ‘adjusted’ profits over time. Stockpile & Ore on leach pad write downs for NEM have been higher than for peers such as Goldcorp and Barrick.

- Expect NEM To Trade Toward $10/Share: Ratios not based on trailing earnings can be helpful in valuing cyclical companies.

- 2016 EPS Expectations Far Too High By Our Estimates: We expect NEM to have flat to slightly negative EPS in 2016, well below consensus of $0.72/share. The write-downs and impairments in the upcoming 4Q15 results may impact our 2016 expectations.

Upshot: We expect shares of NEM to trade toward $10/share amid continued gold price pressure, an inability to repeat prior reported production cost declines, and a return to a pre-commodity boom valuation profile.