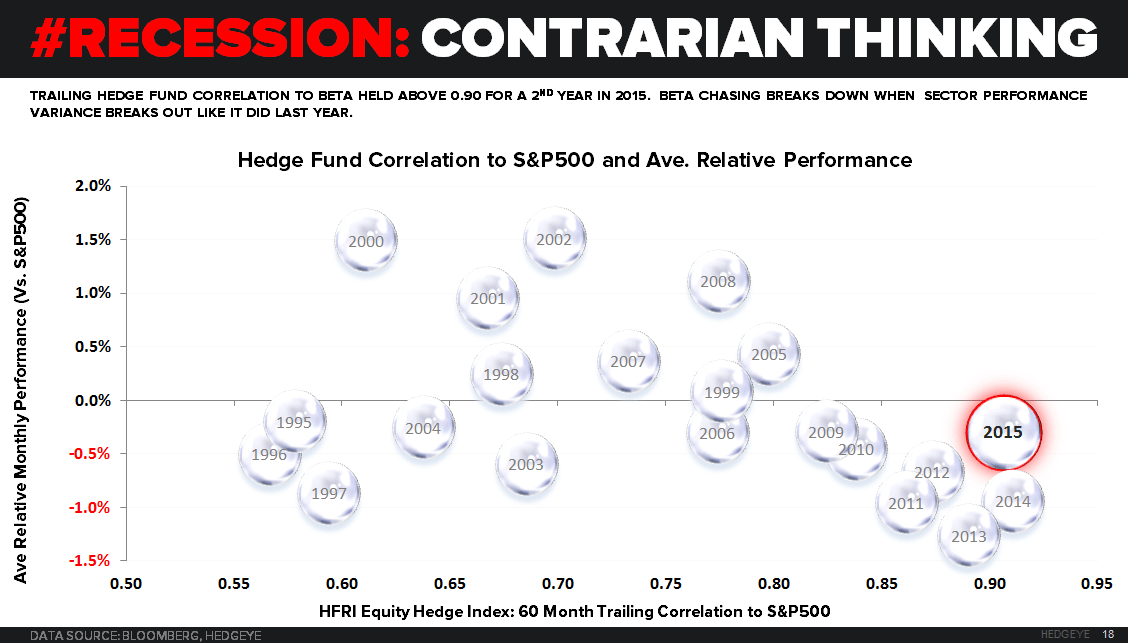

Editor's Note: Below is a brief excerpt and chart from today's Early Look written by Hedgeye CEO Keith McCullough. Click here to learn more.

"... While I shall not love (or hate) stocks, one thing I thoroughly enjoy is fading what has become an epic “Hedge Fund” consensus. As you can see in today’s Chart of The Day (slide 18 in the Macro Deck), there is a raging #Recession in Contrarian Thinking."