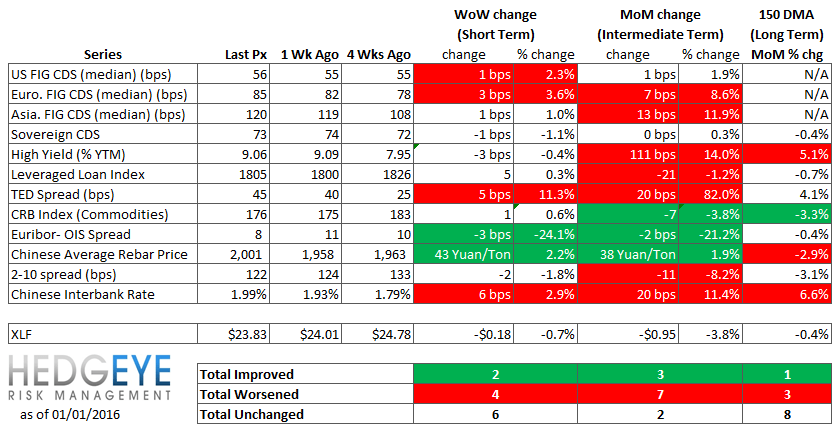

Key Takeaway:

While most of our risk monitor measures were quiet last week, the one that caught our attention this morning was the TED Spread. The TED Spread is notable both for its trajectory/trend and for its absolute level. It stands at 45 bps now, which is +5 on the week and +25 bps on the month. That's a large rise in a short span of time and brings the gauge to levels last seen in the Fall of 2011 - an environment characterized by growing angst over the risk of an EU Sovereign debt/banking crisis coupled with the fallout from S&P's downgrade of the US Credit rating.

As a reminder, the TED Spread - the spread between 3M Libor and 3M Treasuries - is the gauge of perceived systemic risk in the US banking system. In other words, it's a quantitative measure of the risks to the banking system posed by energy, EM, recession, etc. For more, see our labor note from Thursday last week (Initial Claims: Raise Shields!) highliting the recent degradation in the domestic labor market.

Current Ideas:

Financial Risk Monitor Summary

• Short-term(WoW): Negative / 2 of 12 improved / 4 out of 12 worsened / 6 of 12 unchanged

• Intermediate-term(WoW): Negative / 3 of 12 improved / 7 out of 12 worsened / 2 of 12 unchanged

• Long-term(WoW): Negative / 1 of 12 improved / 3 out of 12 worsened / 8 of 12 unchanged

1. U.S. Financial CDS – Swaps were little changed for US Financials on the week.

Tightened the most WoW: ALL, WFC, MMC

Widened the most WoW: COF, PRU, ACE

Tightened the most WoW: MMC, ACE, AIG

Widened the most MoM: ALL, COF, PRU

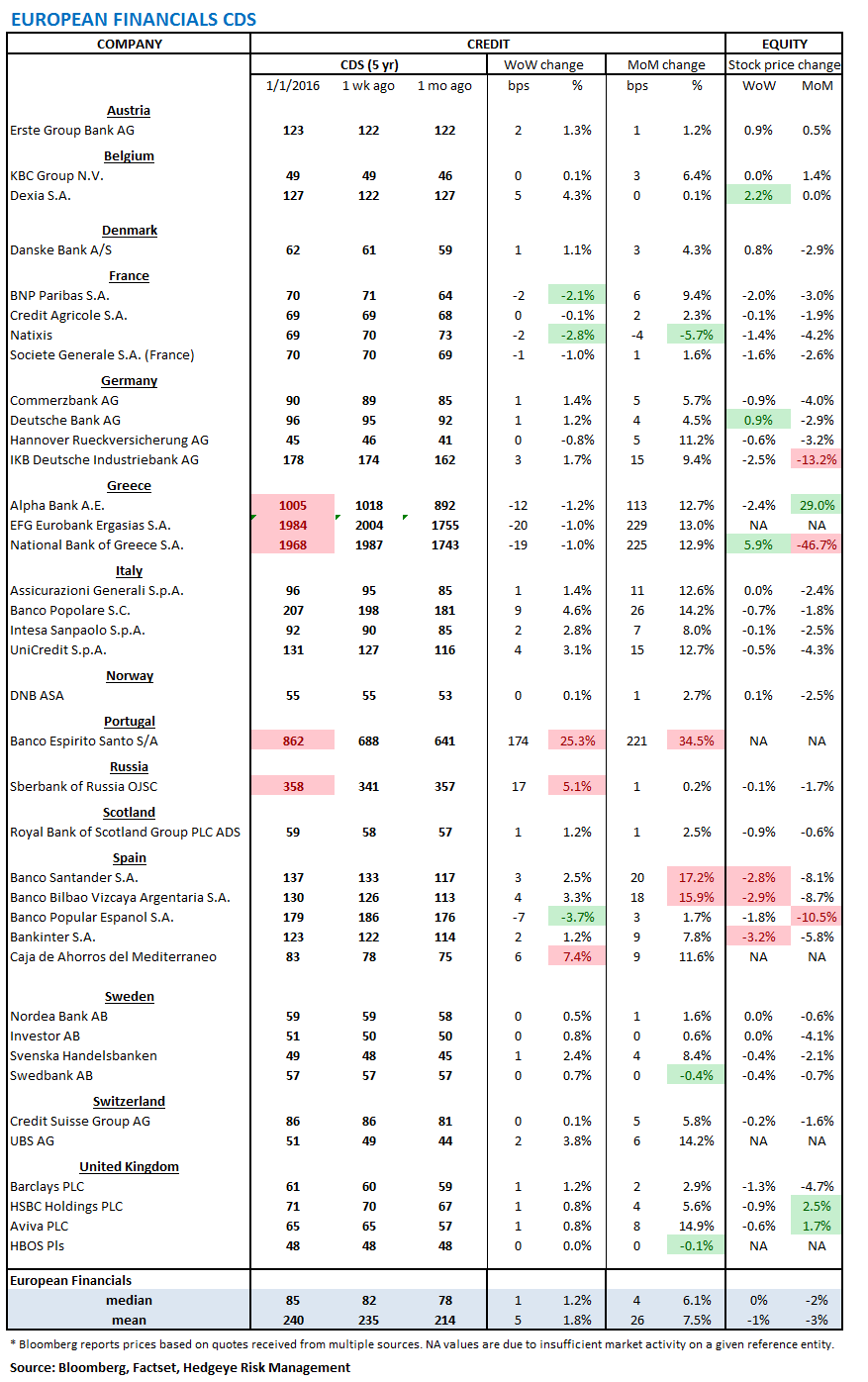

2. European Financial CDS – Swaps mostly widened in Europe last week. Portugal's Banco Espirito Santo widened by the largest margin, by +174 bps to 862.

3. Asian Financial CDS – Swaps of Chinese and Japanese banks were uneventful last week. However, Indian bank swaps had notable moves, both widening and tightening; changes in Indian bank CDS ranged from -7 bps to +19 bps.

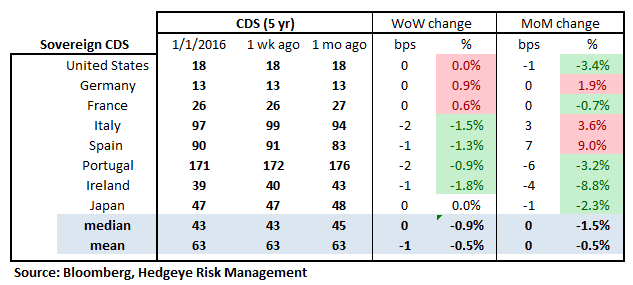

4. Sovereign CDS – Sovereign swaps in developed markets were little changed on the week.

5. Emerging Market Sovereign CDS – Brazilian sovereign swaps remain a major concern trading just below 500 bps.

6. High Yield (YTM) Monitor – High Yield rates fell 3 bps last week, ending the week at 9.06% versus 9.09% the prior week.

7. Leveraged Loan Index Monitor – The Leveraged Loan Index rose 5.0 points last week, ending at 1805.

8. TED Spread Monitor – The TED spread rose 5 basis points last week, ending the week at 45 bps this week versus last week’s print of 40 bps.

9. CRB Commodity Price Index – The CRB index rose 0.6%, ending the week at 176 versus 175 the prior week. As compared with the prior month, commodity prices have decreased -3.8%. We generally regard changes in commodity prices on the margin as having meaningful consumption implications.

10. Euribor-OIS Spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS spread tightened by 3 bps to 8 bps.

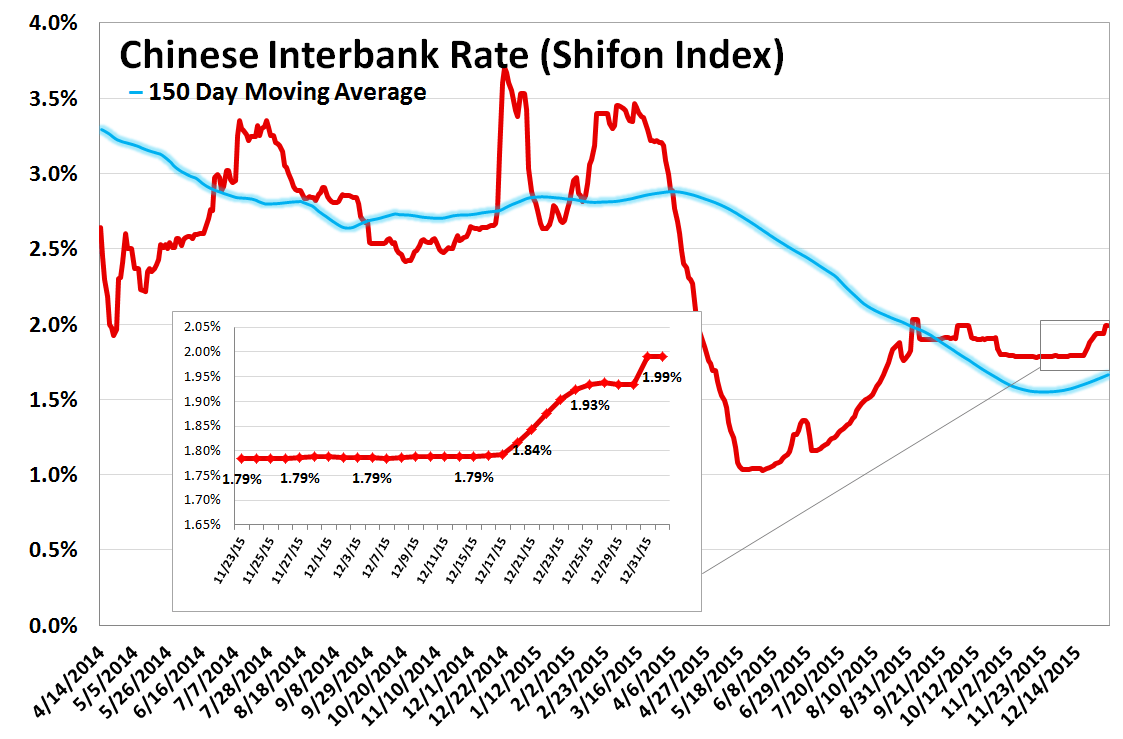

11. Chinese Interbank Rate (Shifon Index) – The Shifon Index rose 6 basis points last week, ending the week at 1.99% versus last week’s print of 1.93%. The Shifon Index measures banks’ overnight lending rates to one another, a gauge of systemic stress in the Chinese banking system.

12. Chinese Steel – Steel prices in China rose 2.2% last week, or 43 yuan/ton, to 2001 yuan/ton. We use Chinese steel rebar prices to gauge Chinese construction activity and, by extension, the health of the Chinese economy.

13. 2-10 Spread – Last week the 2-10 spread tightened to 122 bps, -2 bps tighter than a week ago. We track the 2-10 spread as an indicator of bank margin pressure.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT