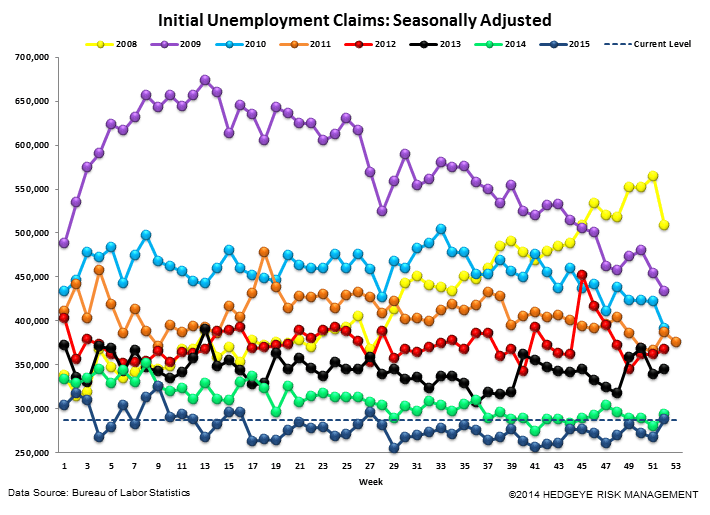

The holiday period is rife with seasonality-related adjustments that may or may not paint an accurate picture of underlying labor market conditions. This is the disclaimer to keep in mind when interpreting the latest week's initial claims data. On its face, however, the recent trend in the data isn't particularly auspicious.

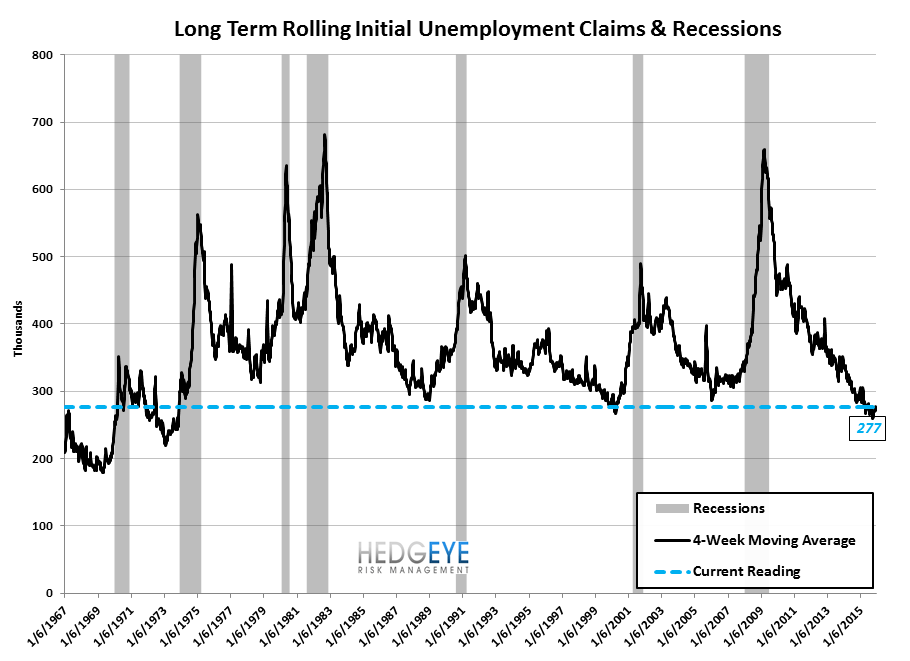

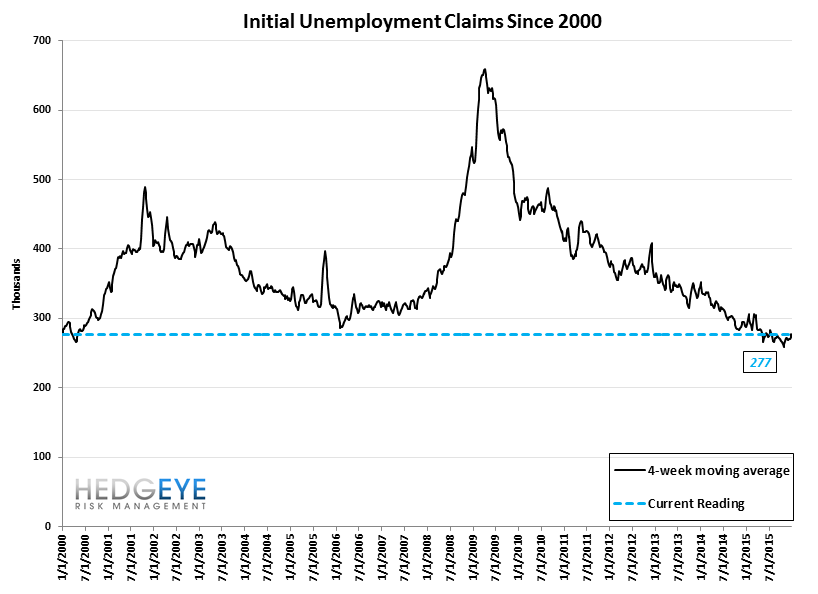

Initial claims on a single week basis jumped 20k to 287k, but, more importantly, the 4-wk rolling average rose another 4.5k to 277k. While 277k is still very low on an absolute basis, it's the highest reading since mid-July. It's also worth noting that rolling intial claims have been moving steadily higher for the last two months.

Amid various other macro data series showing signs of weakening (see Chicago PMI 42.9 this morning), we've been focused more intently than usual on the claims data for any signs of flow through on the labor front. This most recent trend isn't reassuring. That said, it is the holidays so we'll have to wait a few weeks to see whether January confirms.

If this were Stark Trek, we'd offer something along the lines of Raise Shields!

Meanwhile, employment in the oil patch continues to reflect the price of crude. In the week ended December 19, energy state claims continued their trajectory of deterioration versus the country as a whole. As energy companies continue cuts into YE2015 hedge expiration, the spread between energy state claims and total US claims rose from 59 to 62.

The Data

Initial jobless claims rose 20k to 287k from 267k WoW. The prior week's number was not revised. Meanwhile, the 4-week rolling average of seasonally-adjusted claims rose 4.5k WoW to 277k.

The 4-week rolling average of NSA claims, another way of evaluating the data, was -5.8% lower YoY, which is a sequential improvement versus the previous week's YoY change of -5.3%

Yield Spreads

The 2-10 spread fell -5 basis points WoW to 122 bps. 4Q15TD, the 2-10 spread is averaging 136 bps, which is lower by -17 bps relative to 3Q15.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT