Wait... didn't the Fed just hike interest rates? Why are interest rates falling?

Good question.

Here's the lowdown from Hedgeye CEO Keith McCullough in a note to subscribers earlier this morning:

"The yield spread (10Y's - 2Y's) compressed another -2 basis points yesterday back down to a 52-week low of 122 basis points with the retreat in the long-end driving most of the compression. Into year-end, the bond market continues to price in what it has all year long... Slower-and-lower-for-longer (i.e. slower growth and lower rates)."

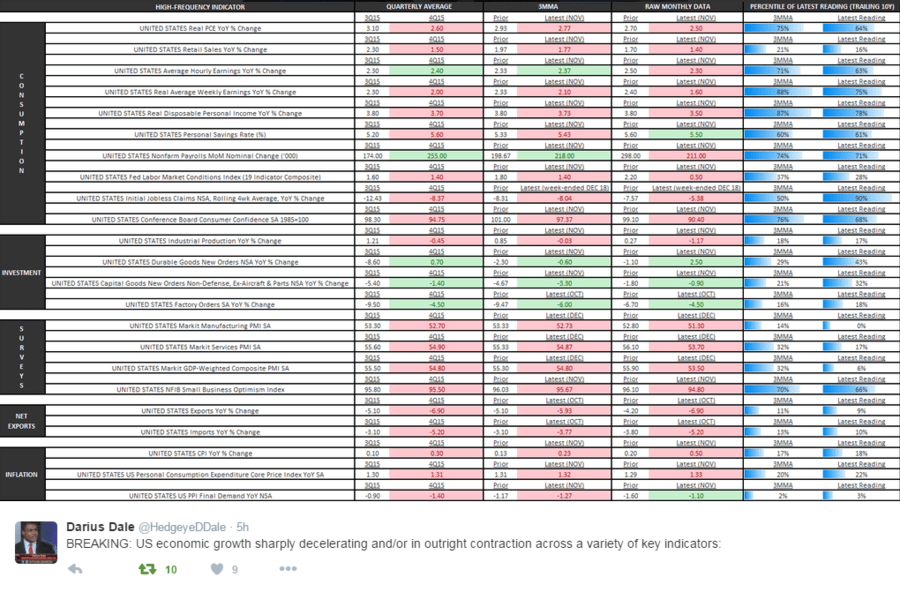

Unconvinced that growth is slowing?

Check out this compendium of contractionary macro data put together by Hedgeye Senior Macro analyst Darius Dale. (Please note the abundance of red.)

CLICK THE IMAGE BELOW TO ENLARGE.

... Or, for good measure, watch Dale on Fox Business this morning where he discusses our economic outlook for 2016. (Spoiler alert: It's not looking good.)

Let's not mince words. Our Macro team has been sounding the alarm on the increasing probability that the U.S. will enter a recession in 2016.

So... how should investors play the compression of the yield curve and coming economic slowdown? Three letters:

T-L-T

Yesterday afternoon, McCullough advised subscribers book some gains in their Long bond (TLT) position in Real-Time Alerts.

Make no mistake though, McCullough is very bullish on long-term Treasury bonds. It's a linchpin for investors who subscribers to our #GrowthSlowing theme, hence the bullish green indicators above over all three of our durations, "trade," "trend" and "tail." (TLT has been a core holding in our longer-term oriented product Investing Ideas. As McCullough is fond of saying, he's "the most bullish guy on Wall Street" ... on Long bonds.)

In Real-Time Alerts, McCullough is simply risk managing entry and exit points in an effort to maximize returns in that core, longer-term TLT position.