Editor's Note: Below is a brief excerpt and chart from today's Early Look written by Hedgeye U.S. Macro analyst Christian Drake. Click here to learn more.

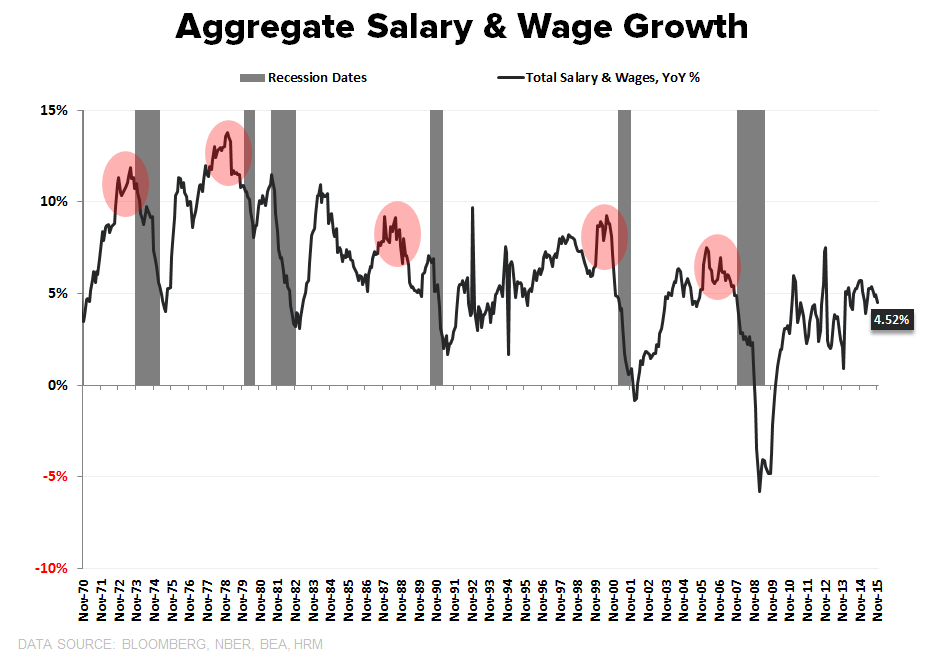

"... Aggregate wage and salary income remains a particularly pronounced driver of consumption in the present cycle with credit growth remaining modest and the long-term capacity for consumer re-levering to drive incremental consumption growth remaining constrained.

Both disposable personal income and aggregate Salary and Wage Income growth decelerated on a 1Y and 2Y basis in November as employment and comp dynamics continue to define the 2nd derivative trend. Aggregate income growth will remain positive over the nearer-term but will continue to slow against steepening comps."