Editor's Note: Below is a brief excerpt and chart from today's Early Look written by Hedgeye Director of Research Daryl Jones. Click here to learn more.

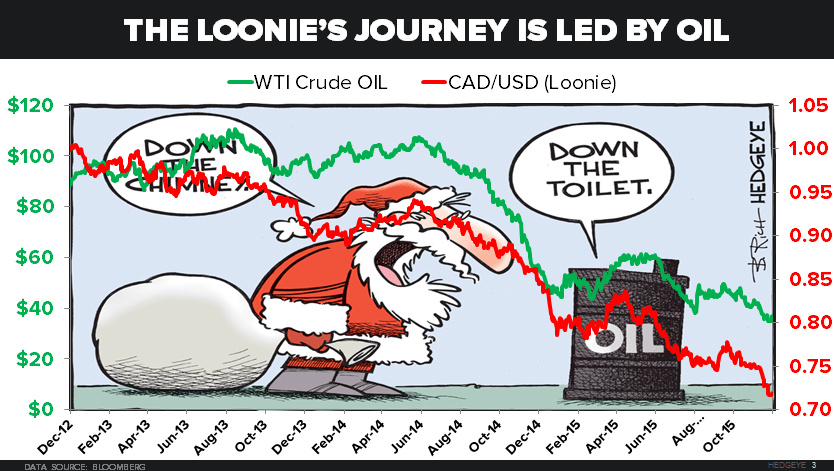

"... Unfortunately for many Canadians, the Chart of the Day shows the real driver of the Canadian economy. In this chart, we look at the relationship between the Loonie and Oil. As shown, historically the relationship between the two is very tight, but this relationship has only tightened and now has a correlation of about 0.94. So as oil goes, so too goes the Canadian economy, despite what politicians might tell you."