Click HERE to watch the replay of this presentation.

Click HERE to listen to the audio replay. Click HERE to access the assosciated slides.

The Wisdomtree business is a very good one that has been smartly launched to gather assets in the market share shift from mutual funds to ETFs. That being said however, expectations are sky high for this small cap company and the stock has substantial growth to backfill to grow into its near 30x forward earnings multiple. We are currently forecasting earnings over -20% below the Street for 2017 and see downside risk in shares.

Our main contention is that the important international hedged equity products have a beta construction weakness and actually underperform local benchmarks in local currency:

The proposition then becomes that this benchmark underperformance has to be made up by the firm's rolling currency hedge. Historically, the hedge has consummed the local underperformance however this is risky considering that across cycle there are more instances than not of local currency exposure actually stabilizing foreign equity returns:

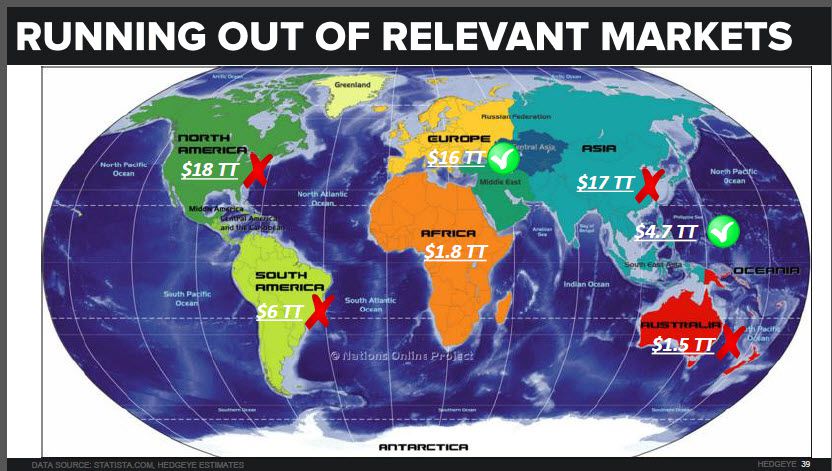

The foreign FX products require liquid and favorable interest rate differentials in the non deliverable forward (NDF) market, which mean that only a few currencies and hence geographies qualify for FX hedged products. Currently only the UK pound, the Euro, the Yen, and the Swiss Franc would be available for FX hedged products. Thus, because the company already has product in the Yen and Euro, the firm has likely already launched it most successful funds in our view:

There is a lot of wood to chop to backfill the Street's high growth expectations. The stock sports nearly a 30x P/E before evening thinking about that Consensus is some 20% too high for 2017.

Please let us know of any questions,

Jonathan Casteleyn, CFA, CMT

Joshua Steiner, CFA