Below are our analysts’ updates on our twelve current high conviction long and short ideas. As a reminder, if nothing material has changed in the past week which would affect a particular idea, our analyst has noted this. We will send CEO Keith McCullough’s updated levels for each ticker in a separate email.

IDEAS UPDATES

TLT | JNK

To view our analyst's original report on Junk Bonds click here.

Our bullish TLT, short JNK investment recommendation is well-documented and the Fed's rate hike has played out as expected during the second half of last week. But the dour outlook on the state of credit markets got worse as even investment grade corporate credit is beginning to crack:

- Glencore’s credit rating was cut by Moody’s to the lowest level to qualify as an investment grade credit (Baa3)

- BHP Billiton’s credit rating was put on watch by Moody’s: “The A1 rating the company has held since 2004 is likely to be cut”

- Kinder Morgan Inc., like Glencore, has a credit rating that sits at the lowest level to qualify as investment grade

Upon aggregating the bank debt of these three massive commodity producers, $120Bn is the notional credit value that might be tiptoeing the “Junk” line by mid-next year. We continue to expect our deflationary outlook to weigh on high yield credit markets into 2016.

As Hedgeye CEO Keith McCullough remarked on The Macro Show on Friday:

"In baseball-speak, we’re in the top of the third inning of this credit market move. And in six months, we might be in the seventh inning stretch. The real problem that is accelerating this slow moving nosedive is that everyone in the business of being long Junk is stuck right now and can’t get out.

And that’s why I’m not covering this short junk bond position. No way."

Now that the Fed finally hiked federal funds by 25bps into a late-cycle slowdown, the fact that TLT was up 1.8% (Wed-Fri.) on “lift-off” should be concerning to the growth accelerating bulls. After the dovish hike, the U.S. Treasury 10-Year Yield (THE GROWTH EXPECTATION PROXY) was down 10 bps (2.3% to 2.2%). And yes, the most telegraphed rate hike ever was dovish.

Just look at the Fed’s projections and the language in the FOMC's statement. Yellen, essentially, acknowledged what we have said for ~ a year and a half now:

- “The Committee expects that economic conditions will evolve in a manner that will warrant only gradual increases in the federal funds rate”

- “Market-based measures of inflation expectations remain low; some survey-based measures of longer-term inflation expectations have edged down”

- “Net exports have been soft”

... And on the Fed’s forward-looking economic projections:

- The Fed kept 2016 GDP estimates unchanged, and downwardly revised 2017 to 2.0-2.3% from 2.0-2.4%.

- 2016 PCE Inflation was downwardly revised to 1.2-1.5% from 1.5-1.8%.

On this week's data, economic gravity failed to be arrested by the Fed:

- CPI printed a goose egg “0%” m/m and +0.5% Y/Y

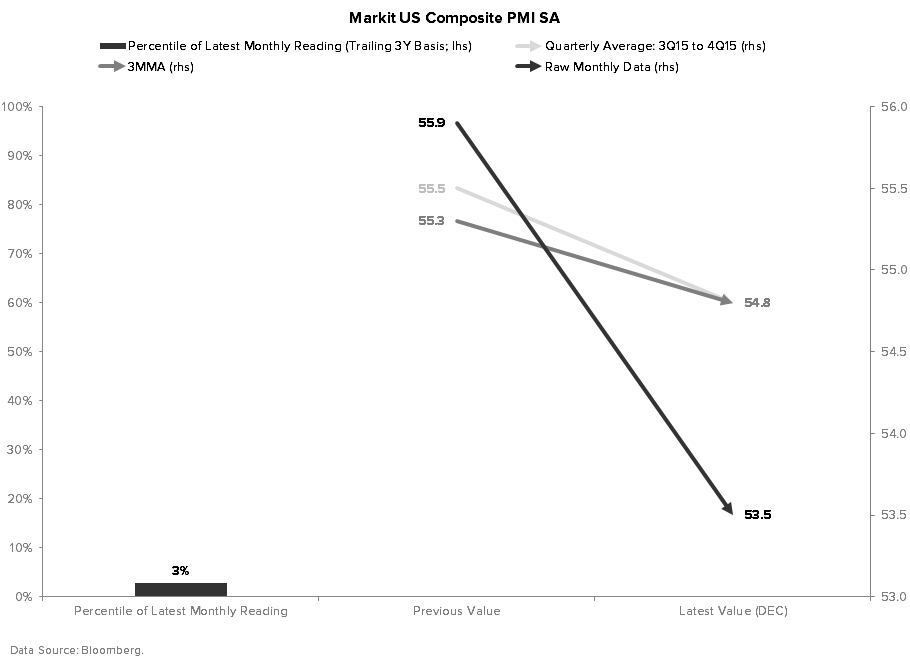

- Mfg. PMI slowed to 51.3 in a preliminary December reading from 52.8 in November

- Industrial Production printed -1.2% Y/Y in November which is recessionary territory for the manufacturing side of the economy. Note: November’s number was the first Y/Y decline on a rate of change basis since December 2009. As shown in the chart below, the trend in this series has been one of deterioration for a year now. As Keith McCullough called out in Thursday’s Early Look, “This isn’t transitory, it’s cyclical”

For anyone who wants to ignore the industrial side of the economy, Friday’s Services PMI number was also a total bomb:

Markit Services PMI decelerated to 53.7 in December vs. 56.1 in November, and is now decelerating on a sequential, trending, and quarterly average basis

Put Manufacturing and Services weakness together for a composite PMI reading that is also decelerating on a sequential, trending and quarterly average basis.

NUS

To view our analyst's original report on Nu Skin click here.

On Nu Skin (NUS), Hedgeye Consumer Staples analyst Howard Penney has no new update this week. The stock is still a strong short both fundamentally and due to the risks associated with investigations and legal matters.

Here's a brief excerpt on NUS from a note Penney sent to institutional clients last Sunday:

"... In terms of open questions, between the end of 3Q15 and the company's investor day (which was 37 days) was there an event that forced management to highlight an additional risk and uncertainty in its SEC filings?

In the recent 8-K, Nu Skin added an additional risk and uncertainty that was not previously there. It reads, “risk that litigation, investigations or other legal matters could result in settlements, assessments or damages that significantly affect financial results.”

Conveniently tucked away about three-quarters of the way into the paragraph this language signals to us that the SEC investigation is very real and could pose a threat to them.

Although it would be pure speculation to think what the meaning of this is, we believe that the SEC investigation is coming to a head, and could have grown larger than its original scope, which was just looking into charitable contributions made in China."

FII

To view our analyst's original report on Federated Investors click here.

Federated Investors (FII) profitability got a boost this week as the Fed boosted short term rates for the first time in 7 years. Even the slight 25 basis point hike improves profitability in the firm’s leading money fund business by +30% into the New Year.

In essence, the firm rolls 30-day paper throughout the short term fixed income curves and the new higher yields forthcoming into 2016 will allow the company to claw back some of the waived fees it has extended to its client base in money funds. Year-to-date the company has waived over $300 million in fees. With that firmly in the rearview, it becomes an opportunity set as FII gets higher yield from cash products next year.

In the financial sector, FII is the most asset sensitive name we cover, meaning it benefits most from even marginal interest rate hikes.

WAB

To view our analyst's original note on Wabtec click here.

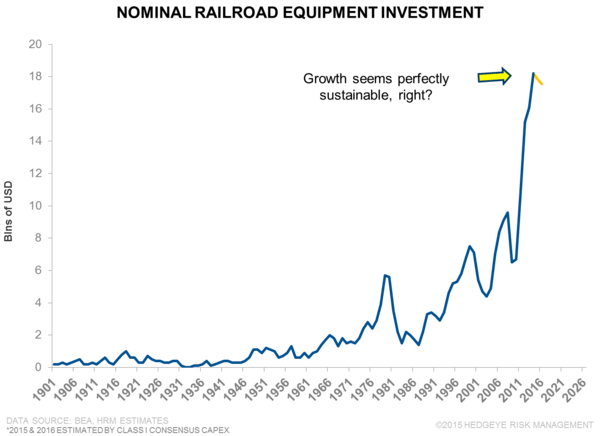

When you boil our Wabtec (W) short thesis down to its essence, it's really quite simple:

Q: Where will railroad equipment investment go in the next five years?

A: We believe freight rail equipment spending is just starting to enter a multi-year downturn. It’s a cyclical market, and WAB shares remain priced for growth.

TIF

To view our analyst's original report on Tiffany click here.

Shares of Tiffany (TIF) are down 2.5% since the company reported earnings in late November and off 11% from the post earnings rally. When we look at this name over a slightly longer duration this is where we stand: We have no doubts in the quality of the management team but the reality is that there are no obvious margin levers to offset the declining growth profile in the business, especially amidst increased late cycle risks.

The price has come off, but so have earnings. It is trading near a peak multiple on our numbers (18x) on peak margins (21%), and peak earnings that are not likely to grow for 2-3 years.

W

To view our analyst's original report on Wayfair click here.

Pier 1 Imports (PIR) reported earnings on Wednesday, and the company reported disappointing top-line numbers and echoed similar commentary we’ve heard across the industry about the highly promotional environment during the Holiday season this year.

Wayfair (W) reported Five-Day Holiday sales growth of 130% Y-o-Y. Management all but telegraphed a sequential increase from the 3Q results when it said it would up the ante during this holiday season in areas like seasonal décor, housewares, etc.

The company realized last year that could play the Black Friday game in areas less tied to furniture and more directly competitive with retailers like Bed Bath, Target, Walmart, Kohl’s, etc. Also, let’s not forget two things:

- Most people did not know what Wayfair was last Black Friday, and

- People don’t use Black Friday as an excuse to buy higher-ticket/margin furniture.

We think that W is one of the culprits driving the highly promotional environment, which won’t be good for either product margins or ad expense as it pays to drive traffic to its site in 4Q.

The longer-term call is that W is building the infrastructure for a TAM that we think is far overstated. By our math the online market for W categories today is $27bil with upside to $45bil by 2020. That’s a big delta from the $60-$90bil being presented to the Street.

RH

To view our analyst's original report on Restoration Hardware click here.

We have to give Restoration Hardware Chairman and CEO Gary Friedman props for his approximately nine minute segment on Cramer earlier this week. Let's face it, him going on what's arguably the most volatile and biased financial media platform, unscripted, is not what we wanted to see.

The risk of fireworks was high.

But he capped off a successful day RH (CFO and IR) had on the investor conference circuit by focusing on the real value drivers at Restoration Hardware (RH) -- growth in product concepts, and RH's real estate transformation. The appearance was planned well before the earnings release, by the way, coinciding with a business-focused trip to NYC.

All-in, it was a positive event for the stock.

MCD

To view our original note on McDonald's click here.

McDonald's (MCD) remains one of our top Long ideas in the restaurants space. Since we initiated our Long call on August 11th at a price of $99, the stock has gone up 17.4%, versus the S&P 500 which is down -4.7%.

All indications are that All Day Breakfast is working to drive incremental traffic to the restaurants with people matching breakfast items with lunch/dinner items driving tickets. We are currently running a survey to get a read on the effectiveness of All Day Breakfast and look forward to updating you in next week's edition.

We continue to love McDonald’s heading into the new year and maintain our price target of $150.

ZBH

To view our analyst's original report on Zimmer Biomet click here.

Zimmer Biomet's (ZBH) has been under pressure in recent weeks alongside the XLV and the S&P 500. The fears of a Fed liftoff in the midst of an economic slowdown, high yield distruption, funds shutting down, and slowing growth have all conspired to keep ZBH well below its 2015 peak of $121 and hovering around $100.

The BLS reported Non-Farm Payrolls and Job Openings (JOLTS) which are both important markers of underlying healthcare demand generally and orthopedics specifically. For Healthcare employment, growth was stable sequentially in November versus October and remained near multi-year highs of just over +3.0%. For Job Openings in Helthcare, levels recovered sequentially for October, but growth remained flat sequentially after beginning a long 18 month march higher off the 1Q14 lows. Our view is employment trends reflect the underlying patient demand, so the peaking in growth reflects a peak in demand.

While the broad market is worried about the Fed liftoff and slowing economic growth, the market seems even more concerned about ZBH’s growth. In the charts we can see expectations for ZBH to growth inline with their recent rate of ~10%. While we believe that is an aggressive growth rate, we may not be alone in a more sanguine view. While 10% growth is in the area code of where consensus expects the XLV to grow going forward, the multiple disparity suggests the market might be more suspicious.

The NTM P/E for ZBH has opened up a huge multiple discount to their HC peers in recent months. That can mean the market is presenting a great buying opportunity, or the market is skeptical of consensus earnings and growth assumptions. We’re obviously on the skeptical side and would like to believe the discount in the P/E multiple is saying the same thing.

Going forward we’ll continue to speak to surgeons about case volume, device pricing, the CCJR, and the ACA. Most importantly, we’ll keep monitoring monthly JOLTS, HC Employment, and our #ACATaper charts. So far, the wave has clearly crested, so grab your board, 2016 is going to be an epic ride.

GIS

General Mills (GIS) is a great stock for volatile times in the market, boasting style factors that we love; large cap, low beta and liquidity.

The fundamental business on the other hand has been struggling. GIS is anchored in the slowing center aisles, and it has struggled in large part to meet analyst expectations. We believe this is due, in part, to management’s overly bullish outlook on their own business during the 1Q16 earnings conference call, which they toned down a bit during the 2Q16 call.

This quarter was the perfect storm of internally and externally driven pressures that lead to downside in the business. Some of the pressures in the quarter included:

- Reduction in merchandise spending due to clean store policies at Walmart, the core contributor to the disappointing cereal performance.

- The yogurt category was especially competitive in the quarter, Chobani and others heavily merchandised while Yoplait held firm and in turn lost share in the quarter.

- The 1H of 2016 was also light on innovation and consumer spend (advertising was down 15% YoY) when comparing it to 1H of 2015.

The second half of 2016 is chock full of innovation, merchandising and strong advertising that should help lead General Mills back to the leadership position in their categories. We are staying long General Mills and view the near term weakness as a strong buying opportunity for a long-term position.

ZOES

Zoës Kitchen (ZOES) is down ~15% this week on the heels of a downgrade from Credit Suisse. We view this as overblown. If you are not in the name already, it is highly advisable to take this year-end sale and get in.

The Credit Suisse report cited valuation, growth and general industry softness as concerns going forward. The analyst may have a small case on the valuation front, but this company is a differentiated concept that has plenty of room to expand and grow into the valuation.

We reaffirm our long-term bullish thesis on ZOES.