“They are who we thought they were”

- Dennis Green (Arizona Cardinals head coach), infamous rant

Today’s Focus: November Housing Starts/Permits & MBA Purchase Apps

The current macro and housing cross-currents are many, the monthly data deluge is ceaseless and, at times, mind-numbing and the propensity for taking a myopic view of every incremental data point is acute - so let’s take a step back:

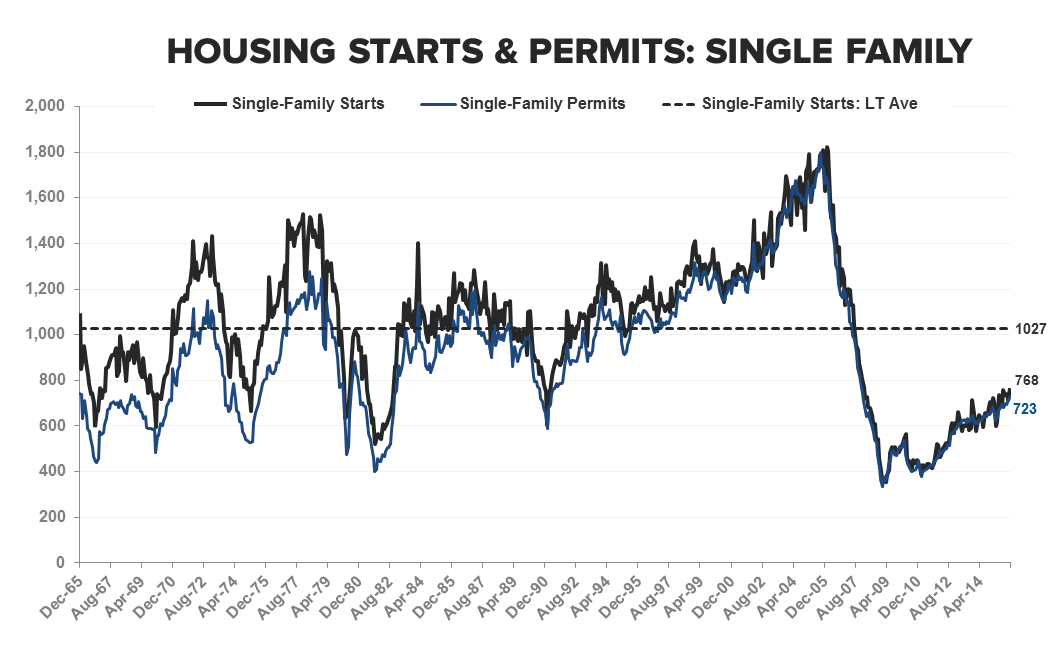

STEPPING BACK: The housing recovery started almost a full three years after the broader recovery. Inclusive of this morning’s Starts data, new single-family construction activity remains 34% below historical averages (and ~90% below average peak levels – remember, housing tends to be autocorrelated, running fully from troughs to peaks). Affordability continues to favor ownership, the labor recovery is late-cycle but ongoing and the labor/income recovery in housing’s key demand demographic (20-40 year olds) has only recently matured beyond the 3Y mark and just begun to drive ownership, household formation and headship rates higher. Lending is pro-cyclical and resi lending standards continue to ease while the regulatory pendulum, after hitting peak tightness in 2014, has begun to swing the other way with the credit box baby-stepping towards expansion. Those dynamics continue to drive crawling but ongoing market normalization (↑ entry level demand, ↑ conventional mortgaged purchases, ↓ distressed/investor sales, etc) alongside the recovery in equity values and underwater/negative equity share.

(Note: We’ll fully detail the opportunity & challenges facing the market in our 2016 Outlook and Themes call on January 8th)

Given that broader, prevailing reality, how would the Trend line in the housing data be expected to look?

Probably exactly like the trend line in the Single Family Starts activity below with construction continuing to stair-step higher. In other words, it is what a common sense expectation of the cycle thought it would be.

Given the magnitude of mean reversion upside back to average levels of activity, how would one expect the MT/LT Trend line in construction activity to look from here?

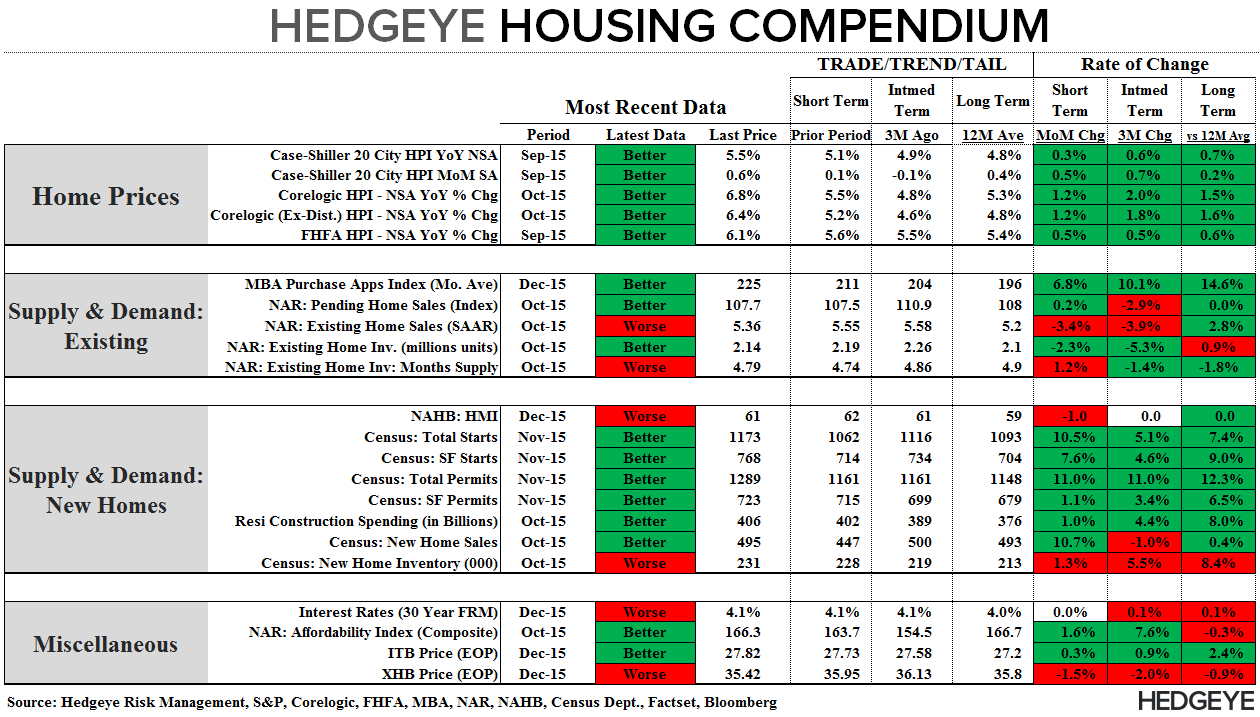

Single family starts rose +7.6% MoM in November to +768K, accelerating to +15% YoY and marking the highest level of activity since January 2008. Single-family permits followed suit, rising +1.1% MoM, making a new 8-year high.

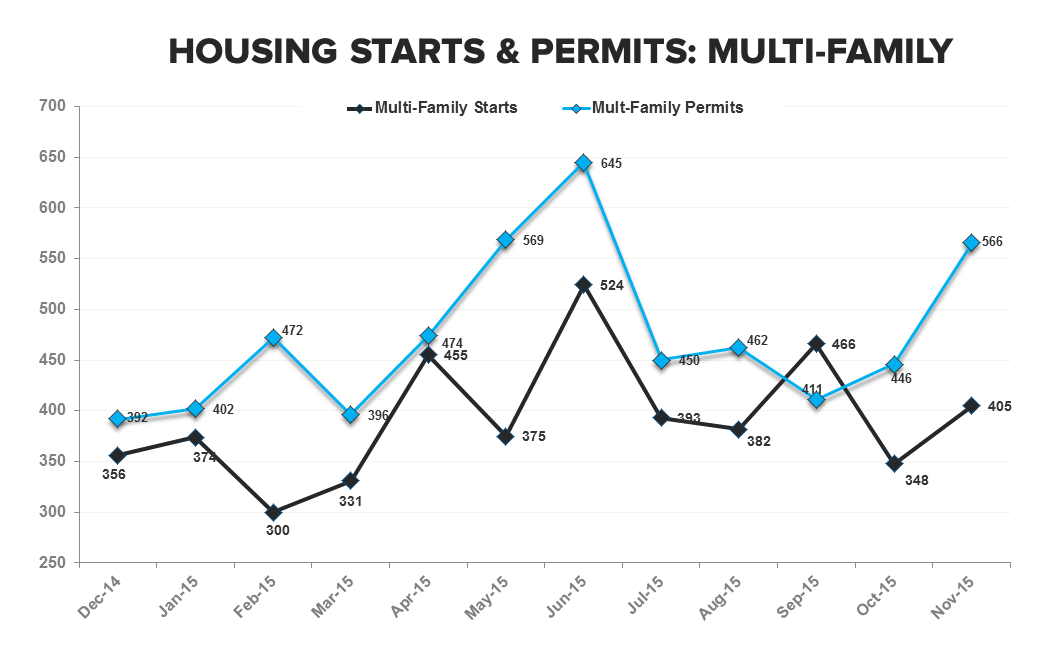

On the multifamily side – which was responsible for last month’s headline decline (see: Starts & Purchase Apps | Neither One Is As It Appears) - activity rebounded, rising +16.4% MoM and accelerating to +20% year over year.

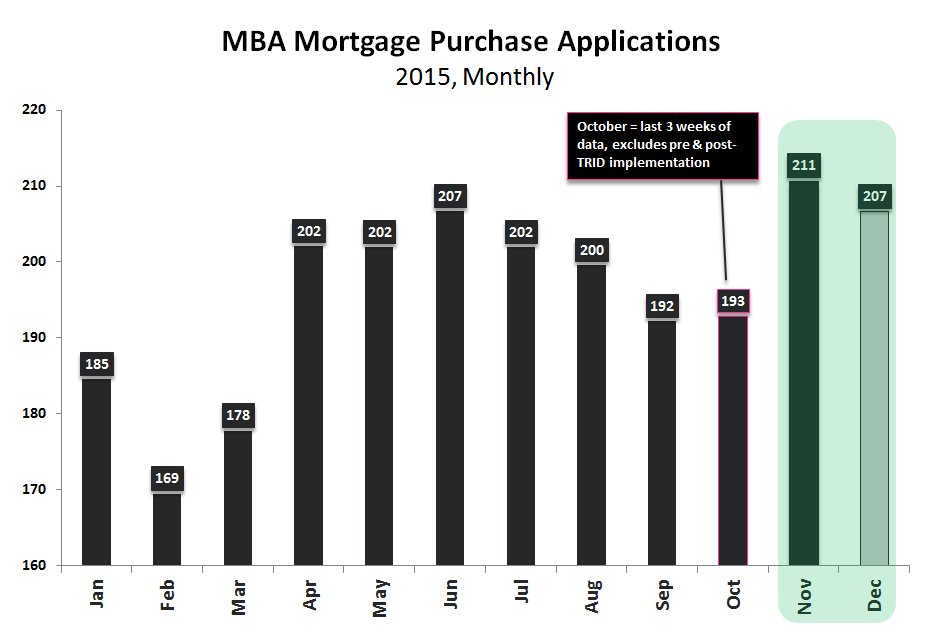

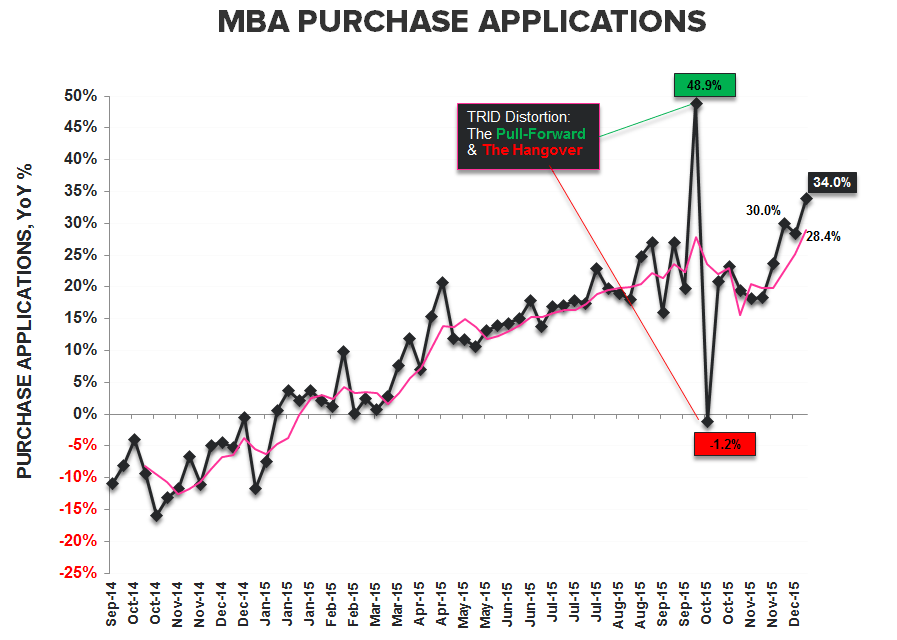

Purchase Applications: Purchase activity declined -2.8% on the latest week but at 221.7 on the Index, the elevated level of demand observed over the last 5-weeks persisted. On a year-over-year basis, purchase demand accelerated to the fastest rate of growth YTD at +34% YoY with 4Q15 currently tracking

+3.4% QoQ and +25% YoY.

Now that we’ve got you all bulled up, let’s handicap next week’s EHS release.

November Existing Home Sales (reported next Tuesday, 12/22) will largely reflect October contract activity and Purchase Application demand was relatively soft in October following TRID's implementation.

Further, the first evidence of any TRID related delays to closings would show up in the November EHS data - we don’t have any hard quant on the magnitude of impact but anecdotal commentary suggest some impact and the risk to the reported numbers is asymmetrically negative. There also exists some modest downside to a full-re-convergence with the trend in Pending Home Sales.

It’s also worth noting that while the longer-term upside in new construction activity off still-depressed levels remains conspicuous, activity in the existing market has already mean reverted back above average historical levels.

Volume growth in the 90% of the market that is existing sales should be more moderate with further market normalization, ongoing improvement in entry level demand, flow through demand from the rental market and credit box expansion anchoring incremental gains from here.

About Housing Starts & Permits:

The US Census Bureau records the number of new housing units that have obtained permits for construction and those that have begun construction. This data includes new buildings intended primarily as residential units. The US Census Bureau defines a start as, “Start of construction occurs when excavation begins for the footings or foundation of a building.”

About MBA Mortgage Applications:

The Mortgage Bankers’ Association’s mortgage applications index covers more than 75% of mortgage applications originated through retail and consumer direct channels. It does not include loans delivered through wholesale broker and correspondent channels. The MBA mortgage purchase applications index is considered a leading indicator of single-family home sales and construction. Moreover, it is the only housing index that is released on a weekly basis.

Frequency:

The MBA Purchase Apps index is released every Wednesday morning at 7 am EST.

Joshua Steiner, CFA

Christian B. Drake