“Gentlemen, I am going to fly.”

-Wilbur Wright

And that, the Wright Brothers did.

But will Janet Yellen?

Ladies and gentlemen, you are about to see an exhilarating political liftoff whereby a dove will pretend to look like a hawk. Then, (within minutes maybe) you’ll be considering a dove being a dove again. I’ll have LIVE analysis @HedgeyeTV at 2:10PM EST.

Click here to join Hedgeye CEO Keith McCullough live on The Macro Show at 9am.

Back to the Global Macro Grind…

Ahead of this historical Fed decision, I’m running out of original content, so bear with me while I update you with yet another data-driven perspective – that of the Bank of England (BOE).

Mark Carney (head of the BOE) stole some headlines this morning by reversing his hawkish course, saying that “rate hike conditions are unfulfilled.” Yep. He told the truth and said that both the growth and #deflation data has slowed since July.

Ultimately, you don’t need a central-planner who is analyzing data (and market moves) on a political lag to remind you what part of the world has already had precipitation. But it is nice to see that some of these people are somewhat objective.

Dollar Up, Pound Down on that…

And what you’d expect to happen on the 1st US rate hike day in 9 years (1st hike into a corporate profit slow-down since 1967), in FX and Rates markets, is happening right now too:

- US Dollar +0.1% vs. the Euro to $1.09 EUR/USD with bearish TREND resistance for EUR/USD = $1.13

- US Dollar +0.3% vs. British Pound to $1.50 with bearish TREND resistance for GBP/USD = $1.54

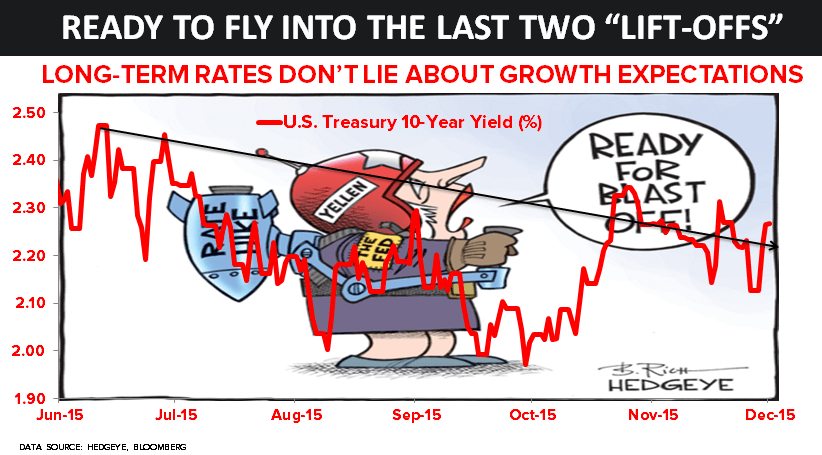

- US 10yr Yield +3 bps on the day to 2.27% (after dropping to 2.13% on last week’s US #GrowthSlowing news)

Interestingly, Global Bond Yields have “bounced” off the lows into this Fed hike too:

- Swiss 10yr +19 basis points (bps) month-over-month to -0.19%

- German 10yr +11 bps month-over-month to 0.64%

- Italian 10yr +11 bps month-over-month to 1.67%

Notwithstanding the basic observation that all of the aforementioned 10yr Yields remain below that of the US 10yr Yield, it’s important to note that British Yields are actually down (1 beep on the 10yr) in the last month on this dovish BOE pivot.

When the growth and inflation data slows, I pivot – what do you do, Sir (and Madame)?

So, let’s say that after an hour (or day) of rate-hiking, the market forces Yellen to pivot. Yesterday’s 0.0% CPI (consumer price inflation reading) and this morning’s US Industrial Production report (reminder, it’s in a recession) definitely support that.

Then what?

Does the Dollar go down? What if it doesn’t (because the Euro, Pound, and Yuan are being centrally planned down)? What if the Dollar doesn’t do anything but rates start going down (again)?

Damn that data. It’s been crashing those who have been betting on higher-rates for almost 2 years.

For those of you who are new to following Hedgeye, we were bullish on US #GrowthAccelerating and bearish on the Long Bond (bullish on #RatesRising) for all of 2013. That, incidentally was the year consensus was actually bearish on rates!

You don’t have to be the Wright Brothers to understand the very basic physical nature of long-term bond yields vs. the rate of change in real-growth:

- When GROWTH is accelerating on a TREND basis, long-term yields rise

- When GROWTH is decelerating on a TREND basis, long-term yields fall

That’s why the longest of “long-term investors” have been right to bet on Lower-For-Longer at every long-term-lower-high in the 10yr Yield. It’s Slower-For-Longer, eh.

With neither growth nor inflation accelerating, you’re probably going to witness the most dovish “rate hike” in US history today. Ladies and gentlemen, she is going to fly alright – in 10yr Yield terms, if she’s lucky maybe 10 beeps.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.12-2.36%

SPX 2003-2060

RUT 1105--1163

VIX 17.98-25.21

USD 97.01-99.54

Oil (WTI) 34.08-37.97

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer