On The Macro Show this morning, Hedgeye CEO Keith McCullough observed that during last week's market rout — the S&P was down -3.8% — volume spiked as equity markets continued to make lower highs. That's a tenuous setup, at best, for equity market perma-bulls as we head into 2016:

"There was a very obvious breakout in volatility on Friday as deflation risk continues to manifest itself in the face of growth slowing.

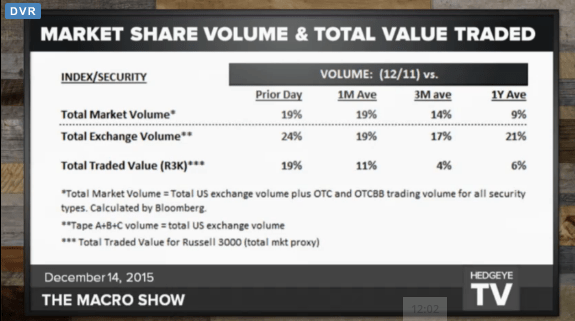

Interestingly, but not surprisingly, volume spiked on Friday. I’ve been waiting for a big flush, down move because we’ve only had three big up moves in the past 26 days of trading. In fact, there have been just eight up days in the last 26. Those up days came after terrorist events and with relatively low volume.

What this visual tells you [see chart below] is that volatility was up 19% versus the 1-month average. So here was the huge spike in volume on the down move.

In other news, small caps continue to be an absolutely atrocious thing to hold long. The Russell was down 5.1% last week and is down 7% year-to-date. That’s not a good year. So don’t believe anybody that is looking for a Santa Claus rally because the S&P 500, for December, is not saying ‘Ho Ho Ho.’ It's down 3.5% for the month to date.

Now, talking about sectors, Consumer Staples is the only one that looks good from a trade and trend perspective. Meanwhile, just one of the many, many, many signals that confirms growth is slowing, consumer discretionary broke down pretty hard last week, alongside the financials. For any of your friends who were long financials in advance of a Fed rate hike, Merry Christmas. The sector is down 5.2% for the year to date.

And yet there are still people out there looking for Santa Claus and PMIs to bottom. This will be fun to watch. For anyone on top of economic reality, you know you don’t have to just sit back and buy stocks into year end. There are plenty of better ways to spend your holiday."