Key Takeaway:

Our risk monitor is now tilted toward the negative across all 3 durations.

High yield backed up another 63 bps to 8.57% last week. Leveraged loans, meanwhile, shed 19 points to 1807 (-1.1%) and are down 30 points on the month (-1.7%). In spite of the emergent carnage in the high yield and leveraged loan markets, the Fed is poised to move forward this week with its first rate hike in almost a decade.

The confluence of a stronger US dollar and both a supply glut and demand uncertainty have crushed oil and the commodities complex generalyl. CRB shed another 3.3% on the week and is down 5.4% on the month. Chinese steel, our proxy for the health of China, is down 2.3% on the week and 9.0% on the month. Beyond this, the TED spread widened by +4 bps on the week to 28 bps.

We've been discussing the risk posed by energy hedges rolling off in the coming weeks. Here's an interesting Reuters article discussing the coming hedge expirations with none other than John Arnold himself being quoted saying (Article HERE):

"Come Jan. 1, revenues will experience a pronounced decline for many companies, coinciding with a time of severe stress for balance sheets across the industry." - John Arnold, Founder Centaurus Partners

Our Canadian bank short thesis should benefit from this coming expiration. Our favorite small cap plays remain CWB (Canadian Western Bank) and MIC (Genworth MI). Our preferred large cap plays remain Royal Bank (RY) and CIBC (CM).

Our heatmap below is more negative than positive across all time horizons.

Current Ideas:

Financial Risk Monitor Summary

• Short-term(WoW): Negative / 1 of 12 improved / 7 out of 12 worsened / 4 of 12 unchanged

• Intermediate-term(WoW): Negative / 3 of 12 improved / 8 out of 12 worsened / 1 of 12 unchanged

• Long-term(WoW): Negative / 1 of 12 improved / 3 out of 12 worsened / 8 of 12 unchanged

1. U.S. Financial CDS – Swaps widened for 14 out of 27 domestic financial institutions. The median spread increased by +4bps from 74 to 78 as investors worried about the effects of a Fed rate hike. Notably, Genworth saw its CDS blow out by +87 bps to 712 bps.

Tightened the most WoW: MMC, LNC, AIG

Widened the most WoW: GNW, CB, WFC

Tightened the most WoW: LNC, ACE, MMC

Widened the most MoM: CB, GNW, JPM

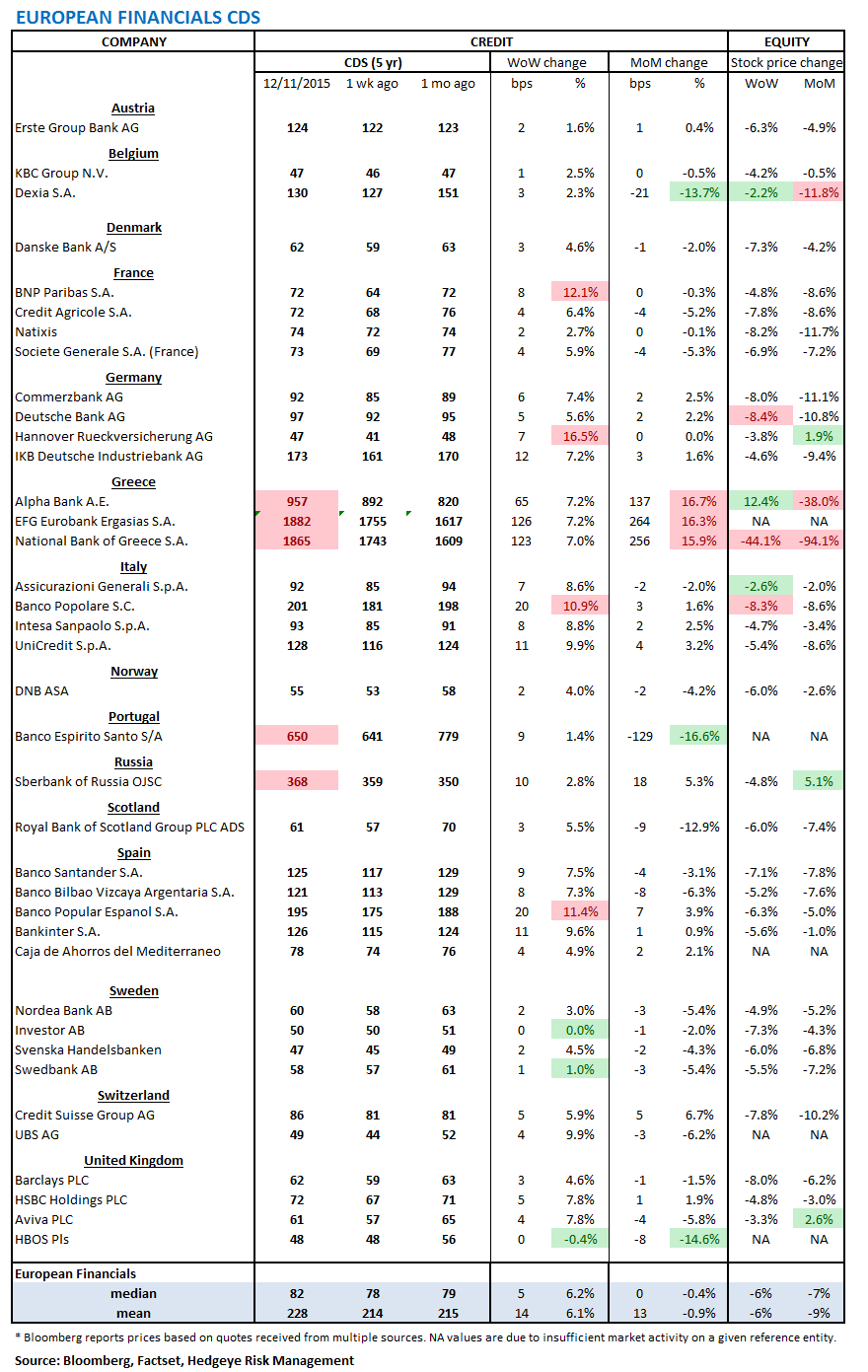

2. European Financial CDS – Swaps mostly widened among European banks last week as global markets were roiled over a likely U.S. Fed rate hike and oil prices falling to new lows.

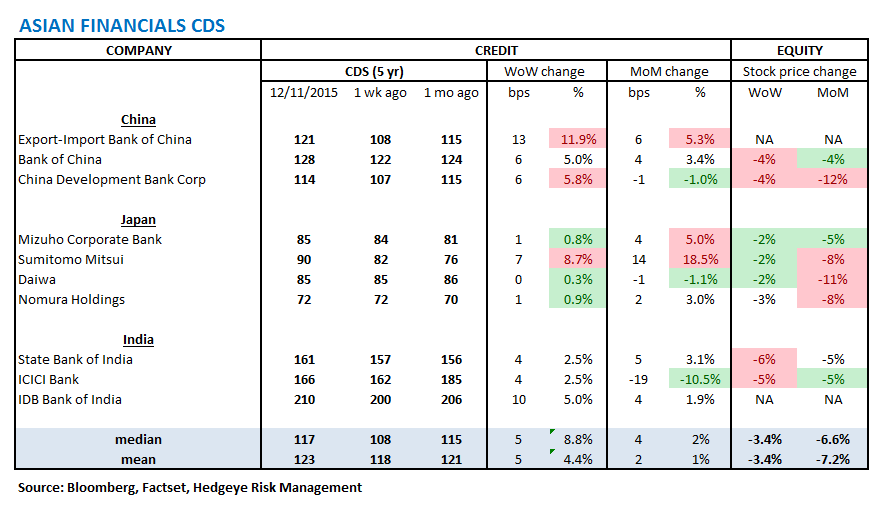

3. Asian Financial CDS – Swaps on Asia banks mostly widened amid global market volatility. The Export-Import Bank of China's CDS widened the most, by +13 bps to 121, followed by the IDB bank of India, which widened by +10 bps to 210.

4. Sovereign CDS – Sovereign swaps were little changed last week. The real takeaway here is the contrast between DM and EM sovereign swaps. Compare the table below with the same table for EM further down.

5. Emerging Market Sovereign CDS – Emerging market swaps widened across the board last week from the negative effects of rising dollar / rising U.S. interest rates and falling oil. Indonesian sovereign swaps widened the most, by +35 bps to 263, followed by Brazilian and Russian swaps, which widened by +34 bps to 479 and +27 bps to 307 bps.

6. High Yield (YTM) Monitor – High Yield rates rose 63 bps last week, ending the week at 8.57% versus 7.95% the prior week.

7. Leveraged Loan Index Monitor – The Leveraged Loan Index fell 19.0 points last week, ending at 1807.

8. TED Spread Monitor – The TED spread rose 4 basis points last week, ending the week at 28 bps this week versus last week’s print of 25 bps.

9. CRB Commodity Price Index – The CRB index fell -3.3%, ending the week at 175 versus 181 the prior week. As compared with the prior month, commodity prices have decreased -5.4%. We generally regard changes in commodity prices on the margin as having meaningful consumption implications.

10. Euribor-OIS Spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS spread was unchanged at 11 bps.

11. Chinese Interbank Rate (Shifon Index) – The Shifon Index was unchanged over last week, ending the week at 1.79%. The Shifon Index measures banks’ overnight lending rates to one another, a gauge of systemic stress in the Chinese banking system.

12. Chinese Steel – Steel prices in China fell 2.3% last week, or 46 yuan/ton, to 1917 yuan/ton. We use Chinese steel rebar prices to gauge Chinese construction activity and, by extension, the health of the Chinese economy.

13. 2-10 Spread – Last week the 2-10 spread tightened to 125 bps, -8 bps tighter than a week ago. We track the 2-10 spread as an indicator of bank margin pressure.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT