“I will be conquered; I will not capitulate.”

-Samuel Johnson

That’s what one of the 18th century’s most renowned writers had to say right before his death. Having published A Dictionary of the English Language in 1755, Samuel Johnson died at the age of 75 in 1784 in London, England.

Not to go all mortality on you this morning, but there is a cycle to big macro expectations. And, yes, some of them die of old age. Being long what the central planners have promised (the illusion of growth, i.e. inflation expectations) killed “reflation” returns in 2015.

What is “reflation”, you ask? I guess it’s the hope that global demand and/or growth “bottoms” and we magically see an end to the best call you could have had in Global Macro in the last 18 months - #Deflation. But hope is not a risk management process.

Back to the Global Macro Grind…

Reflation (per Wikipedia) “is the act of stimulating the economy by increasing the money supply… seeking to bring the economy (specifically price level) back up to the long-term trend.”

That, my friends, is central-planning-cheerleading 101. So whoever’s research you are reading that continues to cheer on “600 rate cuts globally” being the elixir for perma-asset-price-inflation is still looking for Waldo (i.e. demand accelerating).

Newsflash: global demand doesn’t bottom and accelerate when an academic tells it to. It most certainly doesn’t accelerate in the things that have already inflated to all-time-bubble price highs which perpetuated all-time-supply-to-demand-ratio highs.

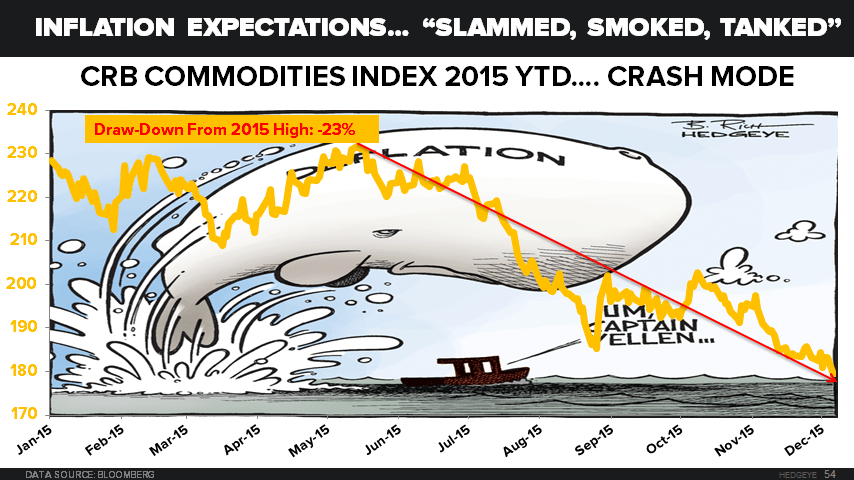

Here’s how “reflation” looked in commodity portfolios yesterday:

- CRB Commodities Index down another -2.6%, taking its crash to -29.2% year-over-year

- Oil (WTIC) smoked for another -5.9% drop, taking its epic deflation to -42.9% year-over-year

- Natural Gas tanked another -5.2% to, taking its crash to -45.6% year-over-year

- Copper deflated another -1.4%, taking its epic deflation to -30.1% year-over-year

- Cattle prices dropped another -2.3%, taking its crash to -26.2% year-over-year

- Coffee prices got tagged for another -1.1% loss, taking its epic deflation to -31.5% year-over-year

Aren’t epic deflations and crashes fun? Ex-all-of-it, “price stability” seems to be tracking right at the Fed’s transitory target!

If you didn’t back out the “transitory” (Fed speak for anything they miss) nature of what was an awesome year (if you shorted every “reflation” hope – and, yes, there were plenty of opportunities to do so), you also nailed the following #Deflation Risk links:

- Foreign Currency Devaluations

- Corporate Revenue and Profit Pressures

- Credit Cycle Risks

When we talk about conquering complacent consensus, we’re talking about making obvious connections in our Macro Themes across asset classes. That’s why it should be no surprise that the following prices hit lower-lows (vs. their SEP lows) alongside commodities yesterday:

- The Canadian Dollar (FXC)

- Ex-Energy names like Freeport-McMoran (FCX)

- Junk Bonds (JNK)

Oh no you didn’t. You didn’t go all FXC or FCX on me this morning did you? Say those tickers really fast and you’ll get a second derivative of a word guys who are long “reflation” are yelling at their screens going into year-end. It’s too bad the PMIs didn’t bottom.

Up next in narrative drift? They definitely have to blame China. The Chinese Yuan is under some pressure this morning and their reserves don’t look so sweet either. So, whatever you do, don’t blame the #LateCycle in both US consumption and employment. Blame Canada too.

In other pure-play US domestic short-selling news, after falling -1.6% last week, the Russell 2000 (80% of its revenues are pure play USA) got slammed for another -1.5% loss yesterday, taking its draw-down from its “reflation” highs in July to -10.1%.

Slammed, smoked, tanked – them be fighting words “folks.”

It’s a good thing we didn’t capitulate and chase those JUL and OCT “reflation” charts.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.14-2.32%

SPX 2049-2109

RUT 1152--1178

VIX 14.01-18.69

USD 97.54-99.46

Oil (WTI) 36.64-39.98

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer