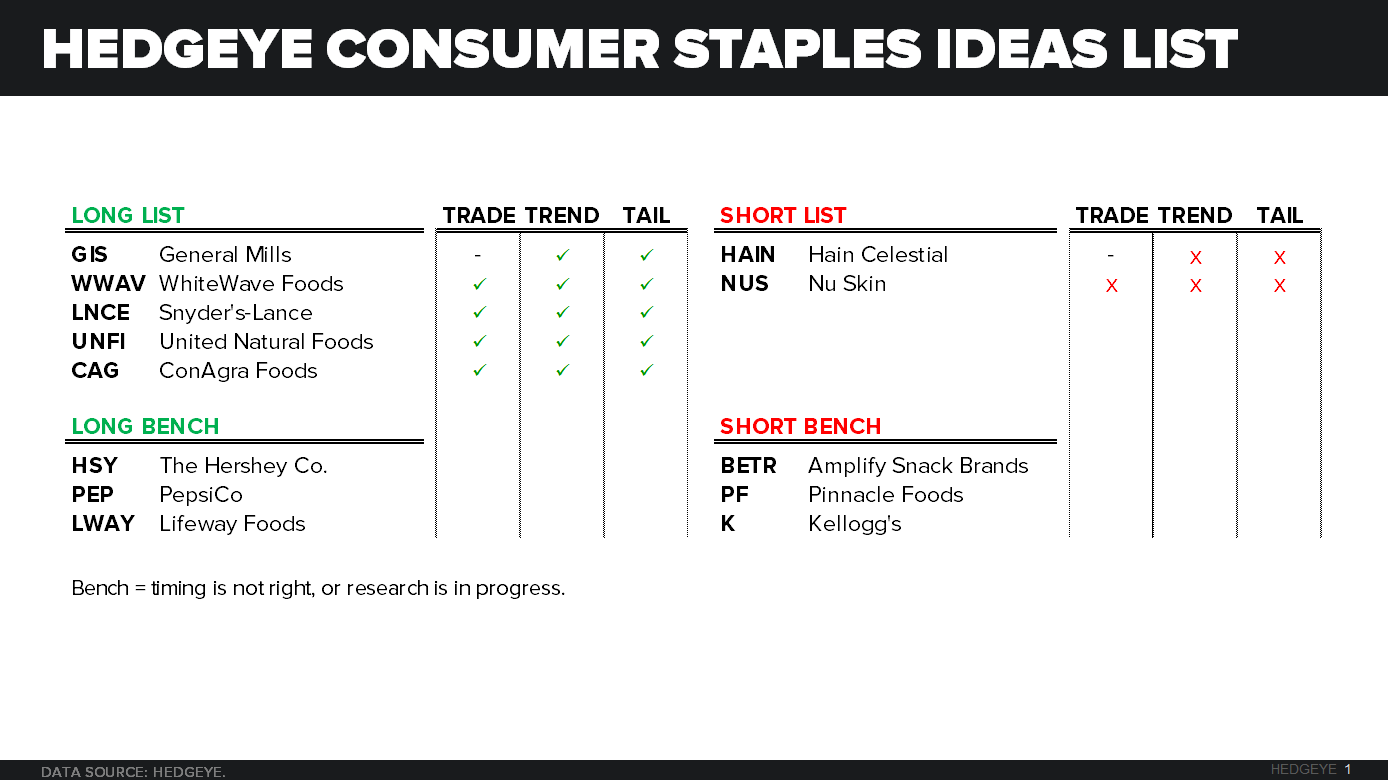

RECENT NOTES

12/6/15 NUS | DIGGING A DEEPER HOLE

11/24/15 NUS THOUGHT LEADER AUDIO REPLAY

11/24/15 THOUGHT LEADER CALL MATERIALS | NUS | ON NOTICE

11/18/15 CAG | SMOOTH MOVES

11/13/15 NUS | SHOW ME THE MONEY!

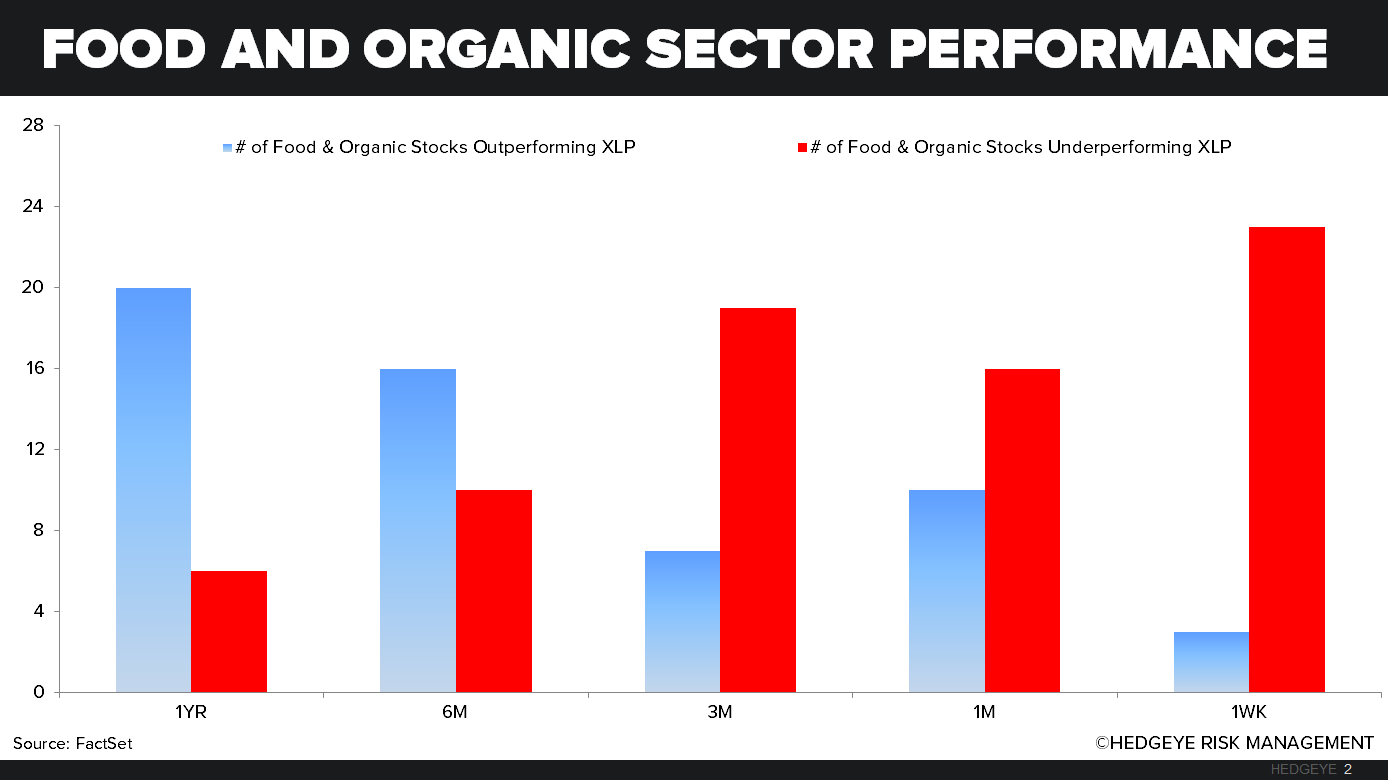

SECTOR PERFORMANCE

Food and organic stocks that we follow underperformed the XLP last week. The XLP was up +1.0% last week, the top performers on a relative basis from our list was Hormel (HRL) and Lifeway (LWAY) posting increases of +2.5% and +1.0%, respectively. The worst performing companies on a relative basis on our list were Amira Natural Foods (ANFI) and Flowers Foods (FLO), which were down -22.6% and -8.1%, respectively.

XLP VERSUS THE MARKET

QUANTITATIVE SETUP

From a quantitative perspective, the XLP is BULLISH in the TRADE and TREND duration.

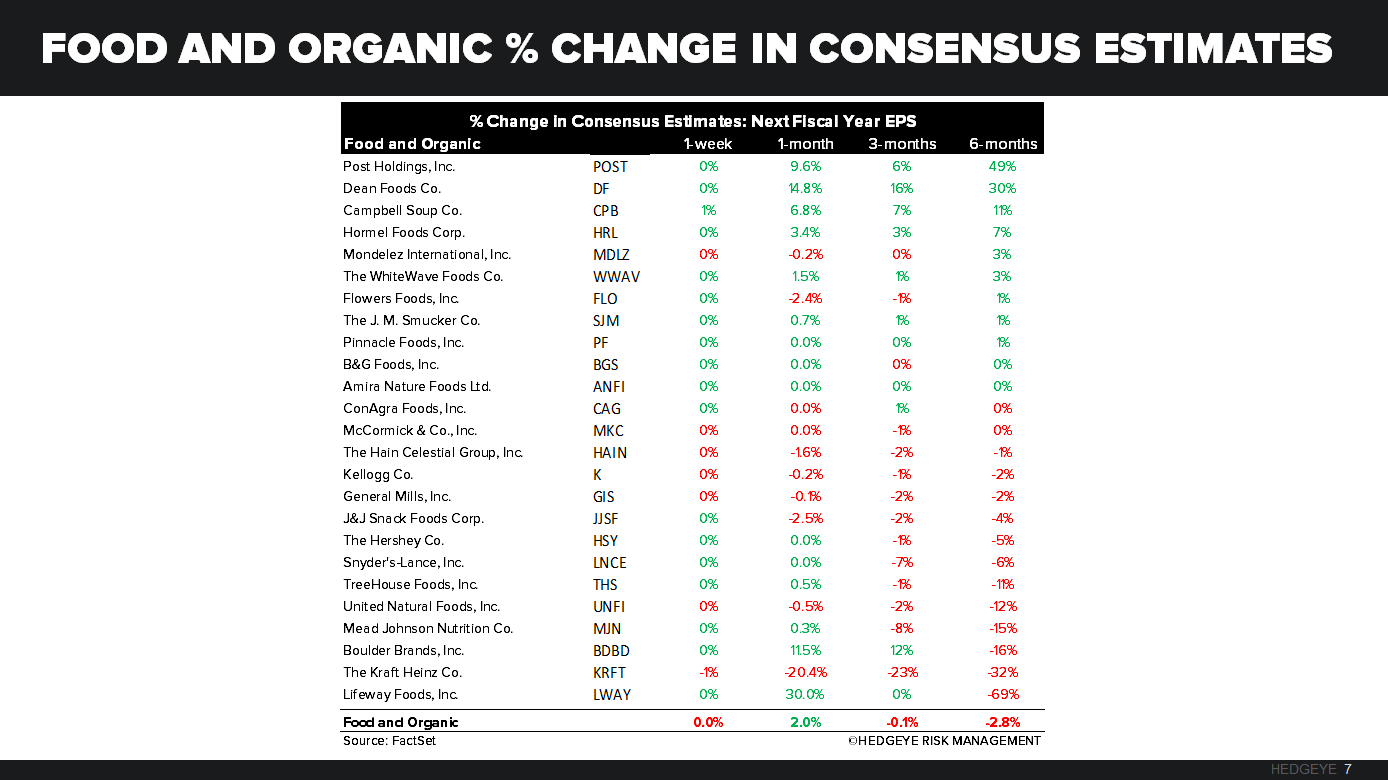

Food and Organic Companies

Keith’s Three Morning Bullets

In rate of change terms, at 1.88% y/y that was the slowest NFP print since the cycle peaked in Q1, but the Fed is going to hike on that:

- EURO – that’s why I signaled buy USD on last week’s Euro ramp of +2.7% - it’s back down -0.6% this morning to $1.08 and has no immediate-term support to $1.05; the data doesn’t matter to the Fed – the SP500 does

- OIL – #StrongDollar (rate hike catalyst DEC 16th) driven #Deflation Risk definitely matters to most asset classes – after a -3.8% decline last week, Oil is down another -1.1% this morning to $39.53 and the Commodities complex remains in crash mode

- EM – Japanese Equities +1% on the Dollar Up move overnight – EM Asia continued lower (no likey Up Dollar); Thailand -0.7% (-6.4% in the last month is one of the ugliest); EM (MSCI Index) deflated another -0.9% last wk to -14.3% YTD

SPX immediate-term risk range = 2057-2112; UST 10yr Yield 2.19-2.33%

Please call or e-mail with any questions.

Howard Penney

Managing Director

Shayne Laidlaw

Analyst