Nu Skin Enterprises (NUS) is on the Hedgeye Consumer Staples Best Ideas list as a SHORT.

Heading into the investor day we thought there was a chance the stock could rally based on the two products (ageLOC Me and ageLOC Youth) being rolled out in 4Q15 and 2016. Fortunately, the company’s other troubles continue to overshadow any other issue.

INCREMENTAL CONCERNS

Between the end of 3Q15 and the investor day (which was 37 days) was there an event that forced management to highlight an additional risk and uncertainty in its SEC filings?

In the recent 8-K, Nu Skin added an additional risk and uncertainty that was not previously there. It reads, “risk that litigation, investigations or other legal matters could result in settlements, assessments or damages that significantly affect financial results.”

Conveniently tucked away about three-quarters of the way into the paragraph this language signals to us that the SEC investigation is very real and could pose a threat to them. Although it would be pure speculation to think what the meaning of this is, we believe that the SEC investigation is coming to a head, and could have grown larger than its original scope, which was just looking into charitable contributions made in China.

HEDGEYE OPINION ON THE INVESTOR DAY

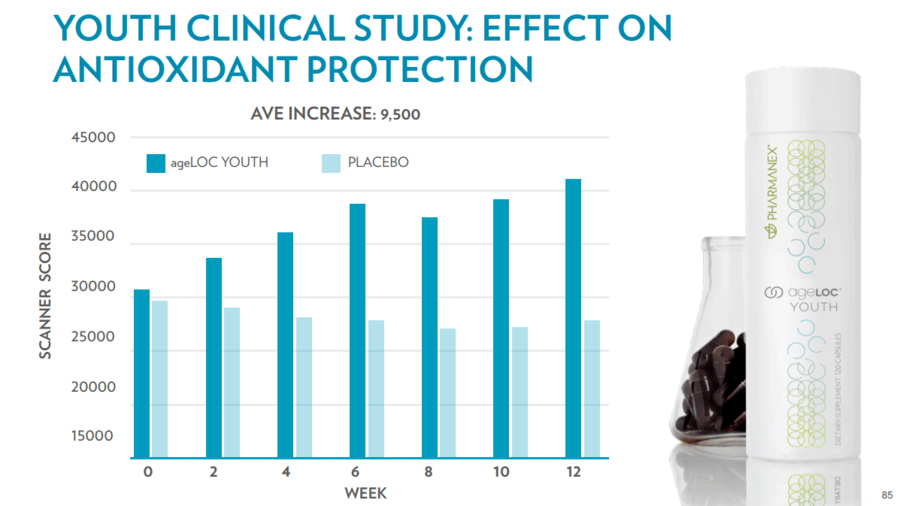

Nu Skin management did little to appease investors questions or concerns about the business during the investor day. The meeting started with addressing the recent controversy surrounding VitaMeal. Which added little incremental information to the discussion, and conveniently enough was untouched in the recorded Q&A session. Followed by a discussion about the overall MLM industry and how NUS plays within that, LTO’s / product launches, sales leaders and consumer retention. Subsequent to that, and possibly the most attention-grabbing portion of the meeting was presented by Joe Chang, Ph. D., NUS Chief Scientific Officer. Joe spoke to the age defying attributes of their new ageLOC Youth system, which in our opinion teetered on the edge of consumer deception as they claimed this “mother of all supplements” targets gene expressions so that they are able to influence the aging process in a positive manor. Management ceases to amaze us, as every time they say something they dig a deeper hole for us to look into, below we dig a little deeper into some top issues.

VITAMEAL

Yes, VitaMeal is a small portion of sales, but our numbers that we built out via company reporting (Smiles Reports) show that VitaMeal is 2.28% of revenue, 78bps above what management is claiming. Management went on to say that the average purchase of VitaMeal is 2.5 bags per month per purchaser, which represents $50 to $60 in revenue per month or $600 to $720 per year. To be conservative we took the $50 per month times three for the quarter, times 65,089 sales leaders, and this got us to 1.7% of sales for 3Q15, still 20bps above management’s number. Management’s next step should be becoming more transparent around their calculation of this number because it never adds up. Next up on the controversy surrounding VitaMeal is inventory loading. Truman Hunt, NUS CEO, stated that this issue is a possibility, but that it is insignificant given it is only 1.5% of sales. The controversy surrounding VitaMeal and the way it is distributed is not going away any time soon, as analyst and investigators are just starting to peel apart the onion.

(Source: Company Filings)

EXAGGERATED PRODUCT CLAIMS

Joe Chang was a true salesman during the investor meeting, pitching ageLOC Youth as the “mother of all supplements,” MOAS for short. It is clear from the recent DOJ announcement (for more info CLICK HERE) that they are cracking down on false product claims and consumer deception. Joe spoke very convincingly on the ability of ageLOC Youth to revert the aging of tissue so that you can appear younger; he made sure to say that it is “not in any way [intended for] life expansion.”

(Source: Company Filings)

(Source: Company Filings)

MANAGEMENT GUIDANCE

The company reiterated 4Q15 guidance of $570 million to $590 million in revenue and earnings per share of $0.70 to $0.73. The company anticipates 2016 revenue in the range of $2.29 billion to $2.33 billion, which would represent growth of 5% to 7%. Earnings per share in 2016 is projected to be $3.25 to $3.40.

12/4/15 Investor day presentation

11/24/15 NUS THOUGHT LEADER CALL WITH JARREL PRICE

11/11/15 NUS BLACK BOOK REPLAY

Please call or e-mail with any questions.

Howard Penney

Managing Director

Shayne Laidlaw

Analyst