Below are our analysts’ updates on our thirteen current high conviction long and short ideas. As a reminder, if nothing material has changed in the past week which would affect a particular idea, our analyst has noted this. We will send CEO Keith McCullough’s updated levels for each ticker in a separate email.

IDEAS UPDATES

NUS

Earlier this week we sent out a stock report outlining Consumer Staples analyst Howard Penney's bearish thesis on Nu Skin. Click here to read the report.

FII

Earlier this week we sent out a stock report outlining Financials analyst Jonathan Casteleyn's bullish thesis on Federated Investors. Click here to read the report. Below is an update from Casteleyn.

With the economic cycle eclipsing 72 months, we think it is time to get defensive. In addition to improved profitability from even marginally higher rates, the money fund business is attractive to us as it is about the time for capital to flow back to cash products as investors get defensive.

Over $1 trillion has come out of money funds sourcing the big bull market in stocks and bonds which becomes the longer term opportunity set for leading money fund managers.

With roughly 9% market share in industry money fund assets, Federated Investors will recapture these funds as returns in risk assets subside as the economy enters late cycle returns. We have modeled +$200 billion in positive money flow for the money fund industry in 2016 and +$400 billion for 2017. This assumption reflects some conservatism allowing for some funds to remain outside the money fund channel.

Every $100 billion in industry assets returning to money funds translates into $0.05 in annual EPS for Federated. Our FII estimates are $2.50 into next year versus the Street at $2.20.

TLT | JNK

To view our analyst's original report on Junk Bonds click here.

On went the game of slowing this week with a little central planning un-secretive sauce. Despite the ECB’s move to cut the deposit rate to -0.30%, Draghi didn’t ring the cowbell loud enough. Meanwhile, Friday’s jobs report might have been just enough for Janet to hike rates into a late cycle slowdown. The consensus long USD crowd was crushed on the ECB news. The dollar lost over 2% on Thursday and rates were pushed higher.

If growth is going to continue to slow, with a rate hike on the horizon, a relative fixed income spread play (long TLT, short JNK) is exactly what you want on.

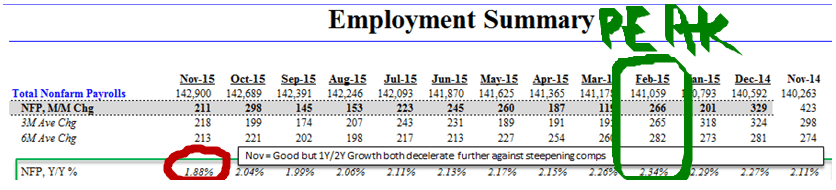

The Jobs Report Friday highlighted a continuation of late-cycle labor market strength:

- On an absolute basis, +211K jobs were added in November on a positive revision from October

- On a rate of change basis NFP gains decelerated to +1.88% Y/Y for October, down from +2.04% in October (the peak on a rate-of-change basis was February at +2.34% Y/Y)

In classic #late-cycle fashion, the reported labor/income/consumption data will remain good over the next month+ but the slope of the line will remain negative.

The bottom line is that the Fed looks very intent on hiking rates to show they can. However newsy a hike might be in the short-run, the Fed will have a difficult time ignoring the ongoing and prospective degradation in domestic economic growth that is embedded in our #LateCycle theme:

- Various measures of household consumption growth (e.g. Real PCE, Retail Sales) are decelerating on both a sequential and trending basis;

- Industrial production growth is decelerating on both a sequential and trending basis;

- Export growth is decelerating on a trending basis and still contracting from a YoY perspective;

- PMI readings are decelerating on both a sequential and trending basis;

- Consumer confidence is decelerating on both a sequential and trending basis; and

- Producer price inflation (a proxy for corporate revenue growth) is decelerating on both a sequential and trending basis.

Rate hike, or not, we expect the bond market to remain the proxy for forward looking growth expectations. It’s been a long ride with TLT, but stick with us for direction as this trade continues to unfold.

LNKD

Editor's note: We added LinkedIn to Investing Ideas on August 3rd. Since then shares have risen over 18% while the S&P 500 has fallen 1.17%.To view the original report on LinkedIn click here.

Our Internet & Media Sector Head Hesham Shaaban has no new update on LinkedIn (LNKD) this week.

WAB

To view our analyst's original note on Wabtec click here.

As rail congestion picked up in 2014, the slower speeds tended to pull equipment on to the track. Now that speeds are picking back up, we expect that equipment to be pushed back out. One can think of it as turning existing assets more quickly.

NSC illustrates the relationship below. More speed results in less equipment in service. If speeds continue higher, freight railroads may find themselves with ample excess equipment and reduced aftermarket needs amid slow volume growth – a negative combination for Wabtec (W).

TIF

To view our analyst's original report on Tiffany click here.

The market might have blown off this ugly print, but we're not.

Tiffany (TIF) will miss again. We’re staying short TIF in the wake of the company’s 3Q results. Simply put, in the absence of 2016 guidance, the consensus will remain too high – likely in the range of $4.30-$4.40. We’re clocking in about $0.30 lower. Is that a huge miss? No. But:

- We also don’t assume a material worsening in the economy in our model, which could push numbers closer to $3.50.

- After last holiday’s blow-up, the Street was at $4.45 for FY15, and now is at $4.02. Not a huge earnings miss by our standards – yet the stock is down 28% year to date. There’s no reason we can’t, and won’t, see that again.

W

To view our analyst's original report on Wayfair click here.

The Holiday sales numbers Wayfair (W) reported this week were big with direct sales up 130% this year and up 103% on a 2yr basis.

Management called out the fact that it would up the ante during this holiday season in areas like seasonal décor, housewares, etc. as it realized last year that could play the Black Friday game in areas less tied to furniture and more directly competitive with retailers like Bed Bath, Target, Walmart, Kohl’s, etc.

While the press release came 6 weeks ahead of last year's, there was no comment this year on the number or percent of orders that were placed by repeat customers which is an interesting omission in its own right.

Also, let’s not forget two things:

- Most people did not know what Wayfair was last Black Friday

- People don’t use Black Friday as an excuse to buy higher-ticket/margin furniture.

The bottom line on Wayfair is that this company is spending – and it’s spending big – around penetrating what management believes to be the company’s TAM. Unfortunately, we think they are overestimating it by a country mile, and are building an infrastructure for growth that will not materialize – at least not profitably.

RH

To view our analyst's original report on Restoration Hardware click here.

A lot has happened in 13 weeks... not the least of which is that

Restoration Hardware (RH) is underperforming not only the market by 16%, but Retail as well (by 7%) – despite RH being more insulated from some of the issues that are clipping earnings today for retailers more broadly.

Over this time period, however, RH meaningfully accelerated square footage growth, launched two new concepts. Some say it’s bad timing. We disagree. RH is our favorite name in the retail space, and we like it across all three durations. Trade, Trend, and Tail.

MCD

Editor's note: We added McDonald's to Investing Ideas on August 11th. Since then shares of MCD have risen 16.9% compared to a -0.7% return for the S&P 500. To view our original note on McDonald's click here.

Restaurants Sector Head Howard Penney had no material update on McDonald's (MCD) this week. However, here is what Penney wrote around when we added MCD to Investing Ideas. It's worth reiterating our high conviction in the stock:

"We continue to get more bullish every time we talk to the company, franchisees and/or customers which we have polled via conducting surveys. We are going to be looking at a much different company 1-3 years from now."

"Urgency has been instilled from the top down by new CEO Steve Easterbrook," according to Penney. "This ship is in gear and headed north. 2015 will be the last time this stock is below $100."

ZBH

To view our analyst's original report on Zimmer Biomet click here.

As growth in employment slows, the impact to Zimmer Biomet's (ZBH) America’s Knee revenue growth rate is likely to slow as well. While it’s not perfect in the very short term, the trajectory seems pretty clear to us.

From our Macro Team, we’ve been seeing ample evidence that the US and global economies continue to slow. For Non-farm payrolls in the US that means the peak growth rate in February 2015 likely marks the top of any economic tailwind we might see in patients heading into the operating theater.

Not that getting surgery is the first thing I would think to do if I was benefitting from a strong economy, but that won’t stop consensus from thinking positive economic growth = positive Knee growth. If you’re wondering, we do think the drivers are much less obvious, but simple none the less.

Does it make more sense that employment in Outpatient Care Centers might be more tightly related to Knee surgical volume? We think so and the chart below suggests as much. If I was giving an estimation of the impact of the “economy” and ZBH, I think it’s probably more informative to believe a slightly more elaborate statement.

Slowing economic growth => slowing employment => slowing insured population => slowing heathcare demand => slowing outpatient care center employment

ZBH has other complicating issues in the shorter term such as the CCJR, pricing, demographics, but as long as the statement above holds together, and the data comes our way, we’re staying short the stock.

We might add the Q415 preliminary to the Employment Outpatient to the chart above.

GIS

General Mills (GIS) continues to be one of our top ideas in the Consumer Staples sector. Sector head Howard Penney loves the name for its characteristics during this macro driven market. Big-cap, low-beta, and their line of sight at growing the top line in a meaningful way, are contributors to our LONG thesis.

Since adding GIS to Investing Ideas at the end of May, the stock is up 3.8% versus down 1.6% for the S&P.

ZOES

"Zoës Kitchen (ZOES) was never a one or two quarter call for us," Hedgeye Managing Director Howard Penney recently wrote.

Given the high multiple nature of the stock, it is ultra-sensitive to the volatile market. This stock does not contain style factors that the market likes right now (high-beta, low-cap), so we expected a turbulent ride, but you must stay strong and buy on the dips.

This week was a prime example, with the stock off 2.5% through Tuesday but then rallied, finishing the week essentially flat (-0.3%). Such selloffs create great buying opportunities. As Penney wrote recently, "we would be buyers of ZOES on any big down day."

There was nothing wrong with the latest quarter. Besides the comp number missing expectations slightly (4.5%, versus consensus expectations of 5.4%), ZOES reported revenue of $56.4 million, representing 29.4% YoY growth and beat consensus expectations of $55.7 million. The company also raised its guidance.

For longer-term investors, ZOES is still one of our high-conviction stocks.