Before reading our expectation on the likely course of action from OPEC (we expect no action), the next few charts should be more concerning for USD Longs/commodity shorts than OPEC jawboning pre-meeting:

- In the first chart below, going into today, commodities have been crushed, yet protection is most expensive NOW (OVX back over 50). The market is heavily short commodities

- Volatility expectations for this year’s meeting are grossly higher than last year – protection is near its most expensive point since summer of 2014 (tighter stops on lower volatility expectations causes more volatility (last year’s 10%+ down day post OPEC meeting)

- The Commitment of Trader’s Report from the CFTC suggests the market was heavily short commodities and long dollars into this week. That doesn't get unwound in one day. A catalyst to take commodities lower from here is hard to find with renewed rate hike expectations.

We’re seeing the risk to one-way consensus positioning front and center, as outlined in a note earlier today titled Is This the Beginning of the Great Unwind of USD Consensus Longs?

This story looks a lot like the end of August pre- Jackson Hole and rate “lift-off” expectations. You could see more of what you’re seeing today on a bad jobs report tomorrow, and this move would be exacerbated if the Fed decides to push a rate cut.

----------

Last year at this time the world was contemplating whether or not OPEC would conspire together in an attempt to move global energy markets. We wrote about the unlikeliness of that happening (OPEC CUT? NOPE. ) The point of the note was to dispel the relevance of OPEC quotas. It’s worth a read as a primer.

A cut was expected by many at $73 on WTI. Now, at $41, the expectation is that OPEC quotas will remain the same at 30MM B/D. For the significance of quota levels, see the chart below which shows that:

- Out of the 48 months over the last four years that OPEC quotas have been set at 30MM B/D, OPEC collectively has produced under that quota in just 4 months (8.3% of the time)

- Since the beginning of 2014, production has averaged more than 1MM B/D above the collective OPEC quota level

- Any reason for production below quota levels has not been voluntary. At the end of 2013, a civil uprising reminiscent of the Libyan Revolution in 2011 was successful in reducing Libyan production by over 1MM B/D in several months (That accounted for two of the months below official OPEC quotas)

- Of the 9 of 12 OPEC producers in the global production table below, only 2 of them has reduced production Y/Y

- Of the 4 largest producers in OPEC, production is up double digits in all but Saudi Arabia where production is still up significantly. That’s a market share story:

- Saudi Arabia: +8%% Y/Y

- Iraq: +27% Y/Y

- U.A.E.: +10% Y/Y

- IRAN: +14% Y/Y

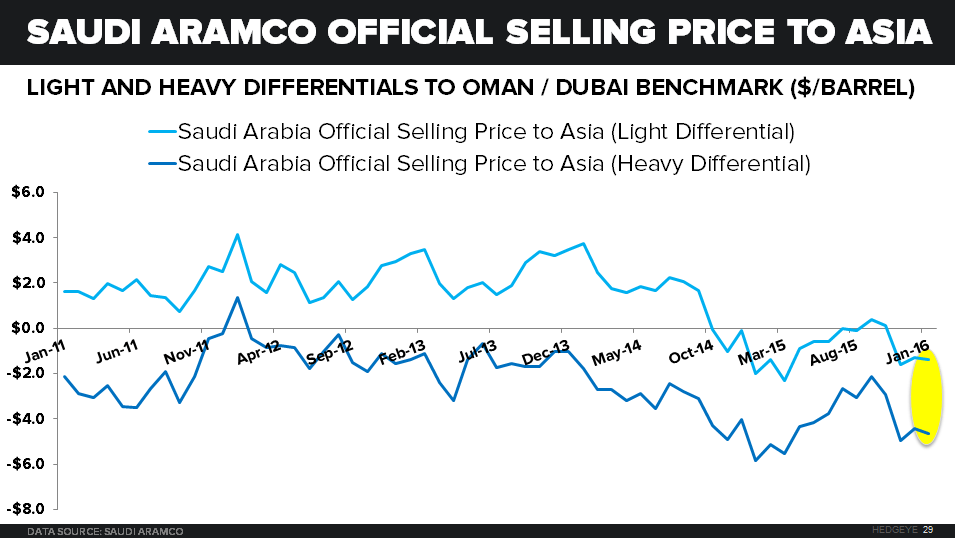

If Saudi Arabia had any plans to cut production they probably wouldn’t be racing to cut official selling prices to Asia into 2016. On a spread to the Oman/Dubai benchmark, Saudi Aramco undercut that spread in both light and heavy crude for January:

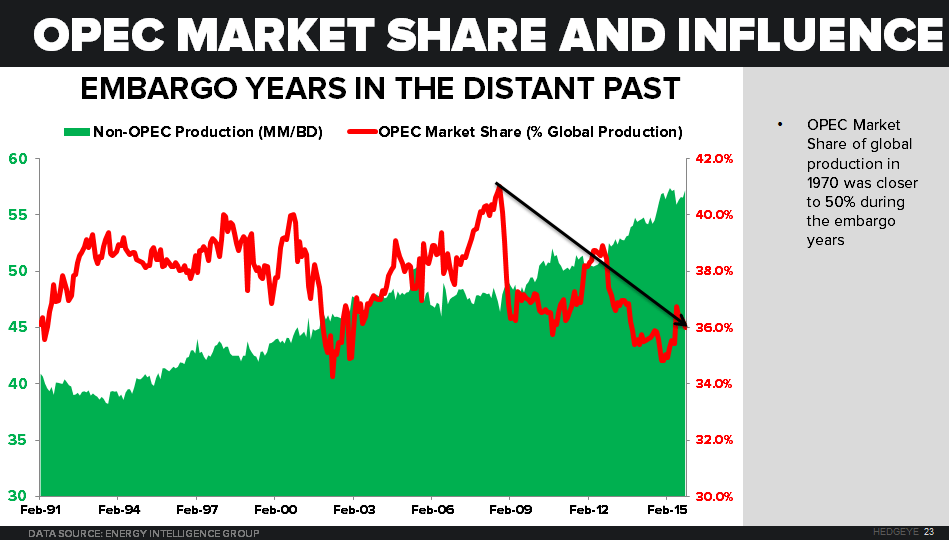

Keeping a grip on dwindling market share is the goal. In a commodity-producing business, a low-cost producer (Saudi Arabia) with the most reserves is not incentivized to cut production. OPEC’s global market share is about 36% currently, but they hold 60-70% of the world’s proven reserves.

Like last year, Russia has already said it has no interest in complying with collective production cuts or even attending the meeting.

Most of OPEC’s spare capacity is with Saudi Arabia. The way they see it, they are doing their job. Given any need to accommodate Iran post sanctions, it would be hard to envision lower targeted quotas unless it was purely a smoke and mirrors exercise to boost prices in the short-term. As outlined in last year’s note, OPEC ANNOUNCEMENTS have an ability to move spot prices for about 15-20 days, but there is no evidence that production levels are at all influenced.

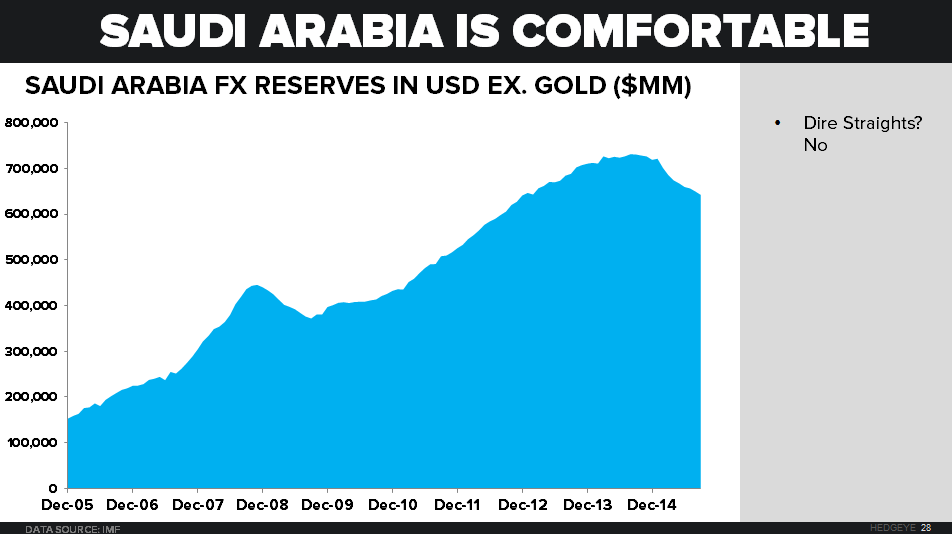

We think the argument the Saudi Arabia would cut production despite the fact that they are a low cost producer with endless reserves (and all of the spare capacity in OPEC) is just newsiness. FX Reserves are only down 12% from an August 2014 high, which is hardly a dent with oil prices declining 56% over that same time period. Prices could remain low for years, and they’d be in good shape.

Deflation has taken a hold of the market for the last 18 months, and the catalyst to reverse deflation’s dominoes will be behaviorally and policy-driven. Look for a real catalyst with tomorrow’s jobs report. A bad one could perpetuate the currency move seen today.

As always we welcome any comments or questions.

Ben Ryan

Analyst