The labor environment remains a two-state system for now. There are energy states and non-energy states. Energy states are continuing to decouple from the broader US, while the rest of the country remains reasonably strong. As the chart below shows, the indexed level of claims for energy states has hit a new high relative to the overall US. This is consistent with our call that energy company hedges roll off en masse at YE2015.

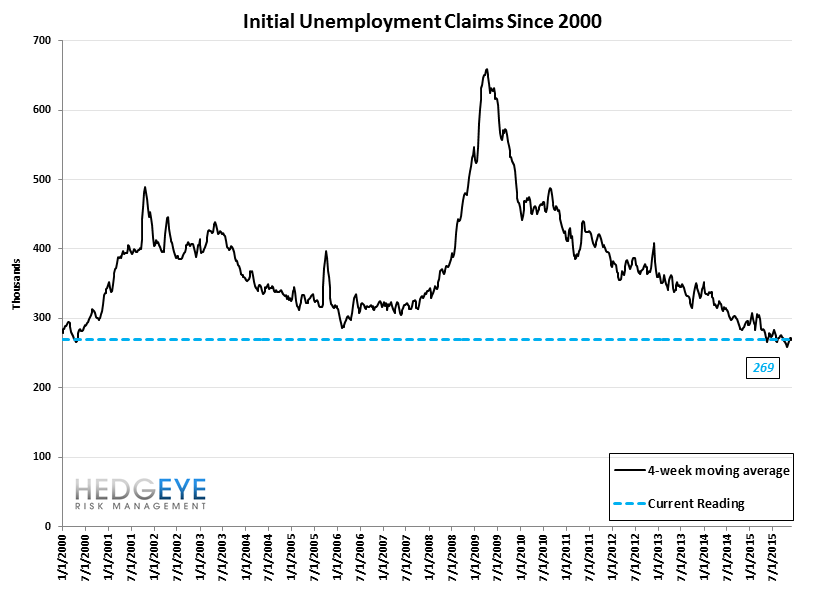

Separately, it's important to keep in context where we are in the cycle. We're now 22 months into a sub-330k claims environment. The last three cycles have seen claims stay below 330k for 24, 45 and 31 months (33 months on average) before the economy entered recession. That puts us roughly in-line with the min, 11 months away from the average and ~2yrs away from the max. We think the amount of track remaining is inversely correlated with short rates. With the Fed poised to begin raising rates in a few weeks, we think the amount of track remaining in this economic cycle is getting shorter.

Bear in mind too that the Fed raising rates will serve to increase the pressure on energy state labor conditions by incrementally strengthening the dollar/furthering energy deflation.

The Data

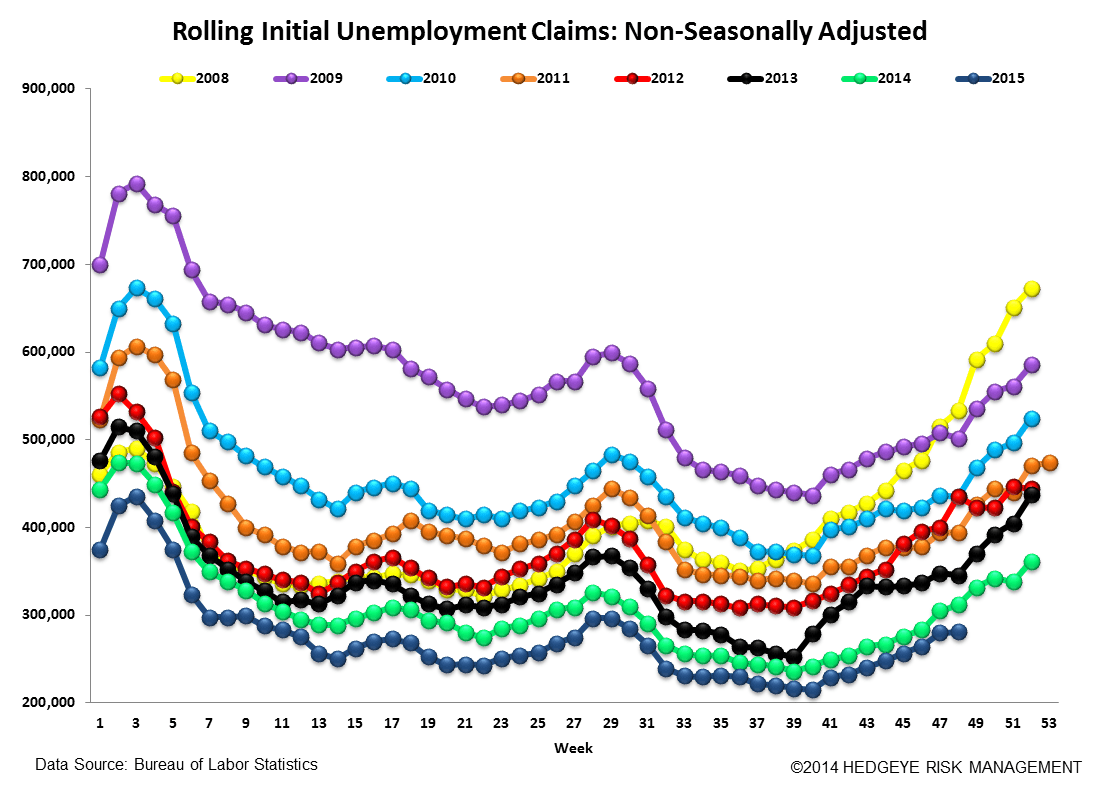

Prior to revision, initial jobless claims rose 9k to 269k from 260k WoW. The prior week's number was not revised. Meanwhile, the 4-week rolling average of seasonally-adjusted claims fell -1.75k WoW to 269.25k.

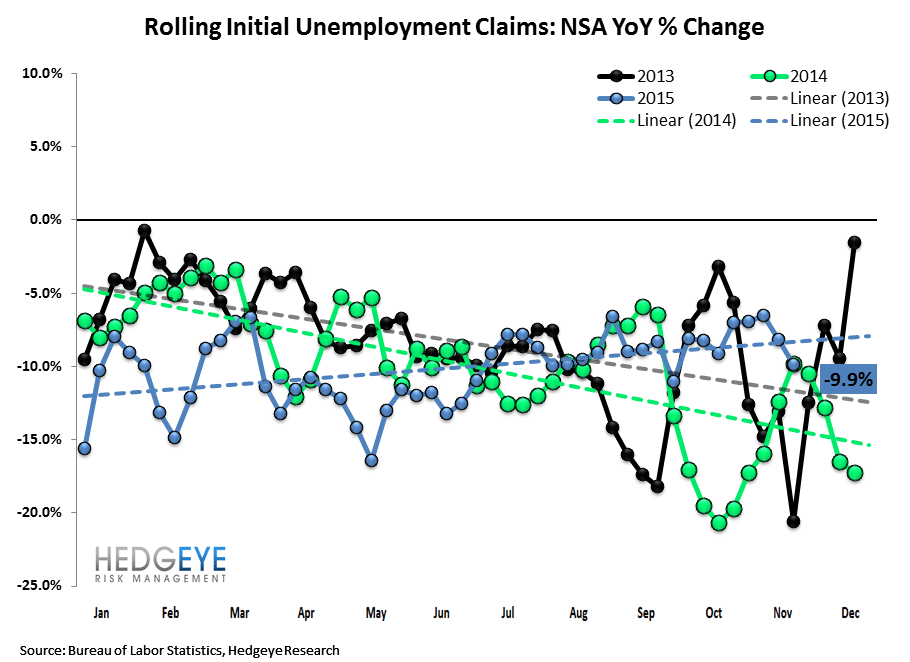

The 4-week rolling average of NSA claims, another way of evaluating the data, was -9.9% lower YoY, which is a sequential improvement versus the previous week's YoY change of -8.2%

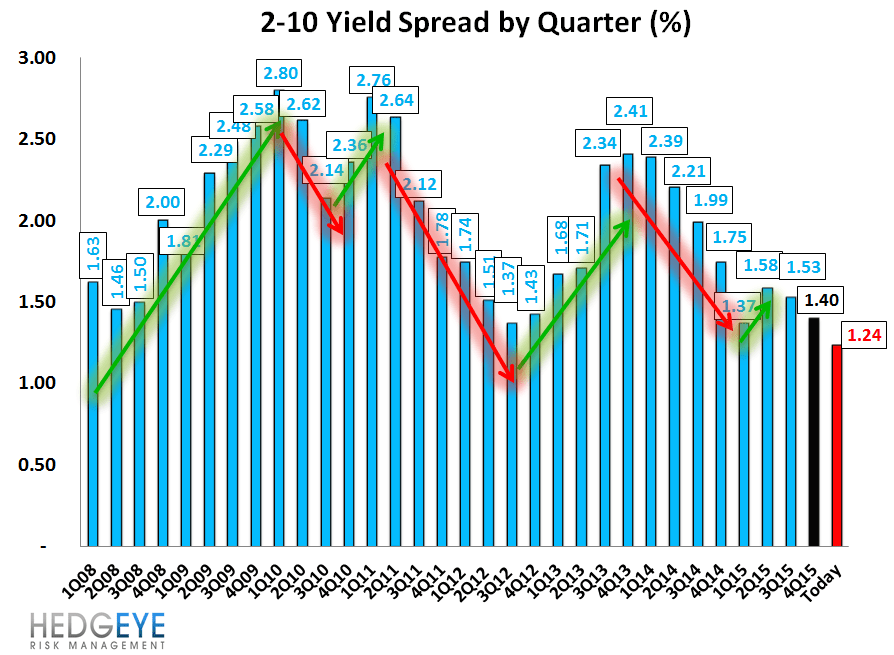

Yield Spreads

The 2-10 spread fell -6 basis points WoW to 124 bps. 4Q15TD, the 2-10 spread is averaging 140 bps, which is lower by -13 bps relative to 3Q15.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT