The Fed continues to say that they are “data dependent.” We just don’t believe them.

In case you missed it, Atlanta Fed president Dennis Lockhart said there was a “compelling” case for a December rate hike earlier today. Maybe we’re missing something here, but didn’t the Atlanta Fed just cut its GDP forecast yesterday? And didn't they ratchet down their GDP forecast the prior week as well?

Apparently cutting your GDP estimate is the new bullish case for liftoff…

Does this make sense?

We’re still scratching our heads. But let’s take a closer look at Lockhart’s speech. We think there are a few revealing insights for investors heading into the Fed’s December policy meeting.

A few excerpts for your consideration:

- “Absent information that drastically changes the economic picture and outlook, the case for liftoff is compelling.”

- “The economy is growing at a solid pace in spite of ongoing headwinds coming from global conditions and the strong dollar.”

- “To circle back to growth drivers, solid job gains and rising household incomes should contribute to a favorable spending outlook.”

Perhaps most important was this story Lockhart told to conclude his remarks:

“To wrap up, I've given you just the highlights of what I can assure you is a comprehensive review of the economic data that my staff and I perform before any FOMC meeting. Policy considerations at the upcoming meeting call for an especially deliberate process. There are two weeks to go, with additional data still to arrive. That said, absent information that drastically changes the economic picture and outlook, I feel the case for liftoff is compelling.”

Wait. Did Lockhart’s “comprehensive review” include his own GDP forecast?

Just yesterday, Lockhart’s Atlanta Fed cut its fourth quarter U.S. GDP estimate to 1.4%. This was down from 1.8% last Wednesday and lower than its 2.2% forecast from less than two weeks ago. Quick rhetorical question:

Q: What did Lockhart et al cite for taking a hatchet to their estimates?

A: Yesterday’s data

Here’s the Atlanta Fed’s explanation accompanying the GDP downgrade:

"The GDPNow model forecast for real GDP growth (seasonally adjusted annual rate) in the fourth quarter of 2015 is 1.4 percent on December 1, down from 1.8 percent on November 25. The decline occurred this morning after the Manufacturing ISM Report On Business from the Institute of Supply Management and the construction spending release from the U.S. Census Bureau."

(sigh)

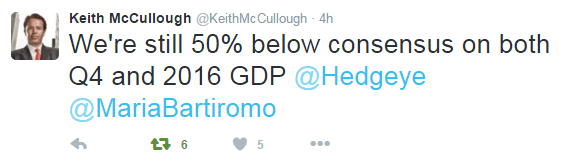

Interestingly, that cut now puts the Atlanta Fed estimate in-line with Hedgeye’s Q4 GDP forecast.

To be clear, our recent market commentary is nowhere near Lockhart's (illusionary) outlook. In fact, we've been very vocal about the rising probability of a recession in the next 6 to 12 months.

So forgive us for thinking Lockhart is being a bit disingenuous when he says that after his “comprehensive review” of the data he still sees a favorable outlook for U.S. growth. (Editor’s Note: In his speech, the Atlanta Fed head didn’t even mention that his team of economists decided to cut their GDP forecast yesterday.)

But we digress...

Lockhart also called the December 15th and 16th Fed policy meeting “historic.”

Finally, something we can agree on...

As Hedgeye CEO Keith McCullough has reiterated in the past few days, a December rate hike would be the first time the Fed raised rates into an economic slowdown.

So to piece together the reality that Lockhart won't tell you: