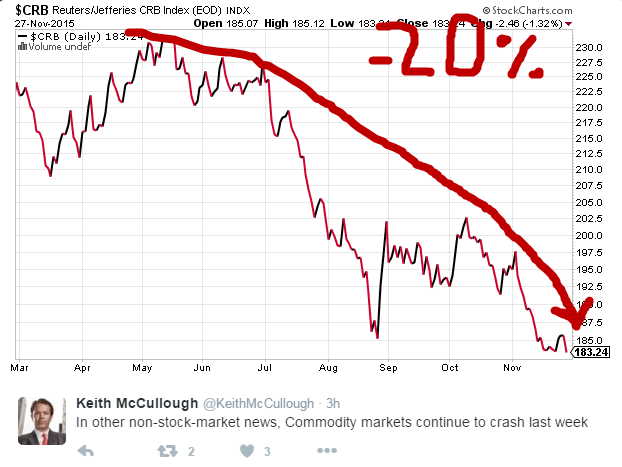

"The Euro was down another -0.5% last week (-12.4% YTD vs USD) and down again this morning as the USD Index ramps above 100," writes Hedgeye CEO Keith McCullough in a note to subscribers this morning. "Commodity markets don’t like this at all. The CRB Index remains in crash mode down -20.1% YTD."

Take a look at the ramp up in the U.S. dollar index since mid October.

As McCullough notes, the CRB index is getting crushed by the strong dollar move.

That's important.

By the time we get to Fed head Janet Yellen’s testimony in front of the “Joint Economic Committee” (JEC) in Washington on Thursday, more #StrongDollar Deflation will still have our esteemed authorities guessing.