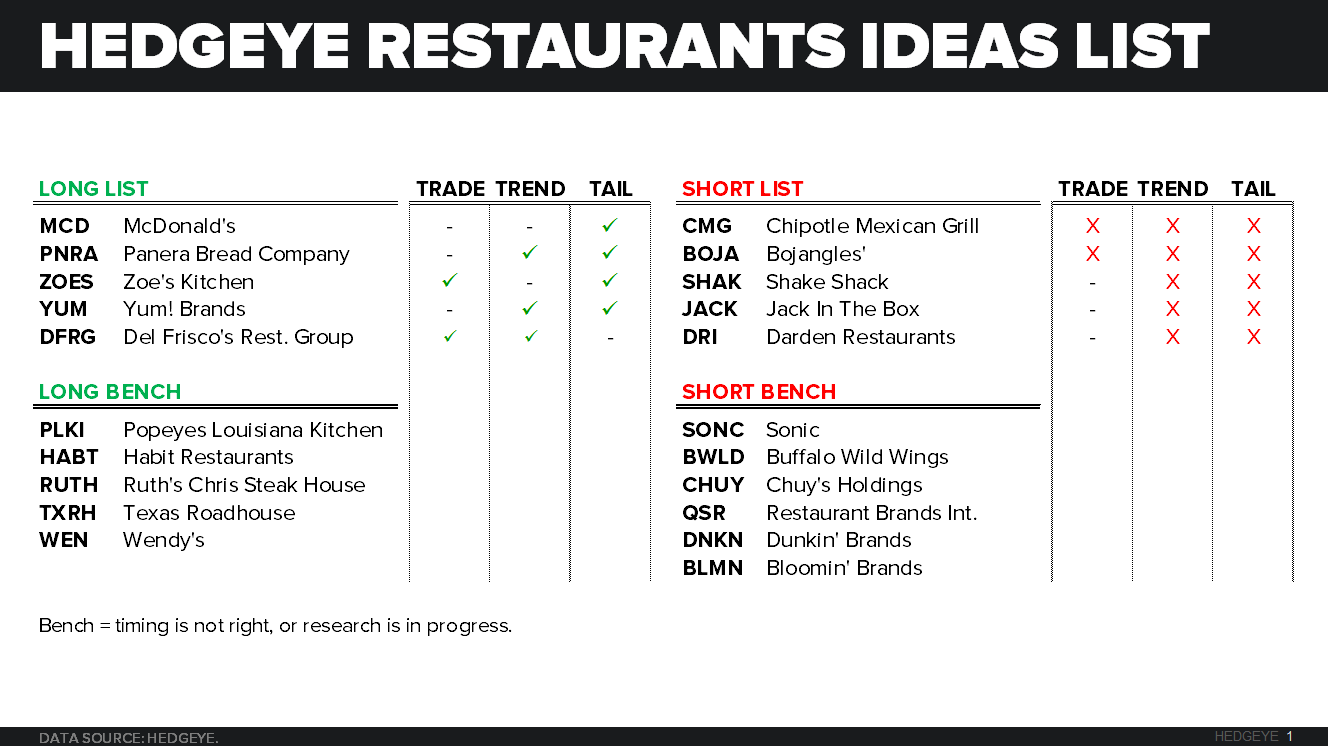

RECENT NOTES

11/24/15 INVITE | THOUGHT LEADER CALL | RICK BERMAN ON CHIPOTLE AND OTHER INDUSTRY ISSUES

11/23/15 Restaurant Industry Macro Note (Sales, Confidence, Employment and Commodities)

11/23/15 CMG | SHORT THE FUNDAMENTALS

11/20/15 WEN | REMOVING THE SHORT | GOING LONG

11/20/15 ZOES | ALL IS WELL IN THE KITCHEN

SECTOR PERFORMANCE

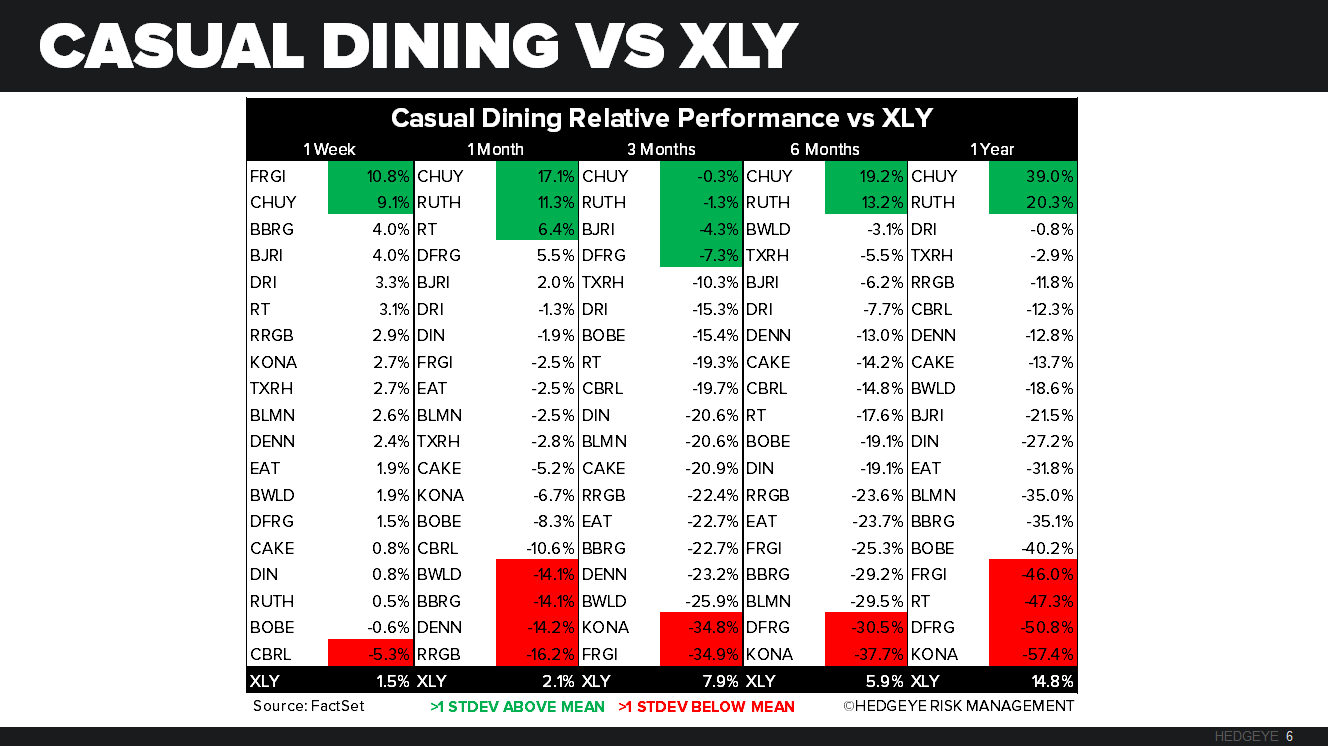

Casual Dining and Quick Service stocks that we follow widely outperformed the XLY, last week, which was up 1.5%. Top performers on a relative basis from casual dining were FRGI and CHUY posting increases of +10.8% and +9.1%, respectively, while ARCO and HABT led the quick service group this week up +18.8% and +9.2%, respectively.

XLY VERSUS THE MARKET

QUANTITATIVE SETUP

From a quantitative perspective, the XLY looks BULLISH from a TRADE and TREND perspective, TREND support is 78.42.

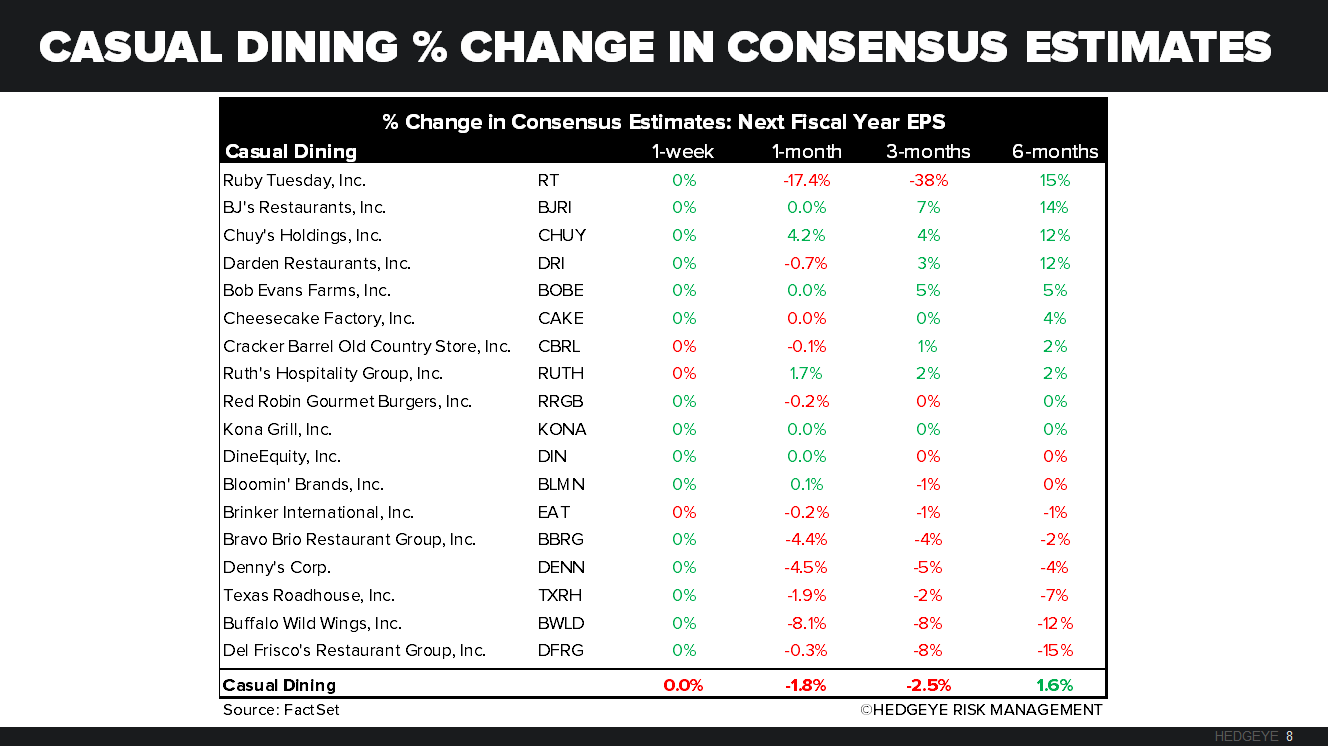

CASUAL DINING RESTAURANTS

QUICK SERVICE RESTAURANTS

Keith’s Three Morning Bullets

Damn the data – it’s all about central planning events this week. Yellen and Draghi have a busy schedule!

- EURO – down another -0.5% last wk (-12.4% YTD vs USD) and down again this morning as the USD Index ramps > 100; Commodity markets don’t like this at all as the CRB Index remains in crash mode, -20.1% YTD

- EM – as long as you only look at the Nasdaq, everything is fine – EM and LATAM stocks deflated another -0.6% and -2.4% respectively last week and EM Asia (Indonesia -2.5% overnight) isn’t responding well to #StrongDollar either

- YIELDS – super spike in the short-end (2yr = 0.95%) continues to flatten he curve (10yr minus 2yr testing YTD lows at 128bps wide this am) – so the Fed can tighten into a slow-down and perpetuate the late cycle slow-down by doing so

SPX immediate-term risk range = 2045-2109; UST 10yr Yield 2.18-2.28%

Please call or e-mail with any questions.

Howard Penney

Managing Director

Shayne Laidlaw

Analyst