“Clearly those esteemed authorities had been guessing.”

-David McCullough

One of the best parts of evolution stories is that eureka moment when someone comes to realize that the received wisdoms of the past are standing in the way of future progress.

The aforementioned quote comes from The Wright Brothers when Orville and Wilbur Wright realize “that so many of the long established, supposedly reliable calculations” (on flight from Lilienthal, Langley, etc.)… “had been proven wrong and could no longer be trusted… the accepted tables were, in a word, worthless.” (pg 63)

To be fair, I don’t consider ECB, BOJ, Federal Reserve, etc. forecasts worthless (there’s so much money to be made doing the opposite of what their anchoring-linear-forecasts imply). But their calculations do pose systemic threats to worldwide economies.

Back to the Global Macro Grind…

For your friends who are still only staring at the “Dow” (in daily fantasy points) as a proxy for what “the market” is doing, there’s absolutely nothing to worry about. The Dow, bro, is only -0.1% YTD.

Then there are those of us who have embraced not only the non-linearity of a dynamic ecosystem like the Global Economy, but the interconnected and sometimes correlating style factors within macro markets (including Currencies, Commodities, Countries).

On that score, last week signaled more of our 18 month old call on the mother of all economic risks – #Deflation. And before I drip on why deflation morphs into a risk to the Fed’s serially overoptimistic growth forecasts, here’s what happened in Global Macro last week:

- US Dollar Index ramped > 100, closing up another +0.5% on the week to +10.9% YTD

- Euros dropped another -0.5% (vs. USD) on the week, taking its YTD devaluation to -12.4%

- Canadians lost another -0.2% of their currency’s purchasing power, taking the CAN$ to -13.1% YTD

- Commodities (CRB) remained in #crash mode, falling another -0.3% on the week to -20.1%YTD

- Oil’s (WTI) crash/deflation for 2015 dropped another -0.5% on the week to -30.4% YTD

- Dr. Copper’s crash/deflation hit new lows intraweek, then bounced to -27.3% YTD

I’ll take a breather right there as that’s just a wall of headline foreign currency and commodity market risk factors that every legitimate macro investor should be aware of. If you don’t do macro, it will eventually do you.

Moving along to the beloved US Equities side of the market:

- Healthcare Stocks (XLV) were +0.8% on the week, still beating “the market” (SP500) at +5.4% YTD

- Financials (XLF) were down -0.4% on the week, still lagging “the market” at -0.6% YTD

Now, as the Fed prepares to raise rates (into worldwide #Deflation and a #LateCycle US economic slow-down), isn’t the ongoing bearish divergence between what the Financials are doing and the Fed’s “supposedly reliable calculations” on GDP interesting?

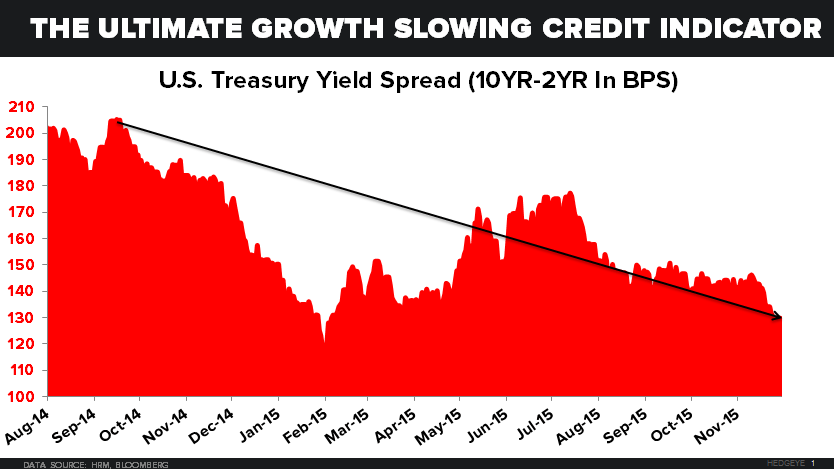

It certainly shouldn’t surprise anyone who is paying attention to both the #GrowthSlowing and credit cycle signals of the bond market. The long-end of the curve is compressing into said “hike” expectations.

Here’s how that looks this morning, in bond market terms:

- Short-term (2yr) Yields spike to 0.95%

- Long-term (10yr) Yields don’t budge at 2.23%

- Yield Spread (10yr minus 2yr) compresses to +128 basis points, -23 basis points (at the lows) YTD

In other words, since the rate of change in the Yield Spread is a far better leading indicator for the expansion/contraction of the economy than some central-planning dude’s forecast, the Global Macro market continues to read the Fed’s forecast (hike) as a risk to the economy.

Oh, and on the said “data dependence” of the Federal Reserve, they’ll get both a PMI reading out of Chicago this morning and an ISM reading for November tomorrow. Last month’s super slow ISM reading of 50.5 wasn’t cited by anyone at the Fed, or our competition.

But does the data really matter? Nope. Yellen’s speech at the central-planning (economics) club of Washington on Wednesday does. And so will Mario Draghi’s central market planning event on Thursday morning (ECB meeting).

By the time we get to Yellen’s testimony in front of the “Joint Economic Committee” (JEC) in Washington on Thursday, more #StrongDollar Deflation will still have our esteemed authorities guessing.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.18-2.28%

SPX 2045-2109

NASDAQ 5034-5181

USD 99.19-100.29

Oil (WTI) 40.55-43.26

Copper 1.98-2.11

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer