Conclusion: We’re happy to get into the debate about how crowded the parking lot was at the mall this weekend, but it’s nowhere near as relevant as the current profitability growth trajectory for Retail, and the consensus expectations for the group as we head into 2016. The good news is that 4Q sales estimates look only slightly high. The bad news is that margins expectations are still 50-100bps high for the group. The worse news is that the Street’s numbers are banking on a recovery in growth and margin starting in 1Q16. In other words, it’s chalking up this ‘thing’ retailers are feeling now as exactly what management teams want us all to believe – while they cross their fingers, hope and pray that the economy is not really slowing. The group might be viewed as damaged goods in this market, but keep in mind that it’s only down 4.3% for the YTD vs a 1.5% gain for the market – not a big difference. It’s trading at 18-19x earnings, and has short interest that is disproportionately low for an economy that is #LateCycle. We’re net sellers of Retail.

SHORTS: FL, KSS, HIBB, TIF, TGT, W, WSM, HBI, COLM, LULU, GPS, M

LONGS: RH, KATE, NKE, PIR, RL, DKS

FULL DETAILS

We’re going to let #WallStreet1.0 debate the success of the start of the holiday season based on things like how long the lines were at the Gap, counting shopping bags and empty parking spaces, or how long it took to get a Chick-fil-A at the food court. But I think most of us would agree that basing one’s view on a small handful of stores is a pretty useless exercise given that there are about 1,100 regional malls and 7,100 shopping centers in the US, which combined account for $5.3 trillion annually, $2.5 trillion in discretionary spending -- nearly $300bn of that falls in the month of December alone. Yes, there are always data points and anecdotes that might ultimately prove to be representative of the whole, but from our perspective, you overwhelmingly need to go big picture in looking at the next few months. That picture, unfortunately, is not a good one.

In contrast, management teams have been generally upbeat with Black Friday press releases (especially Kohl’s, Wal-Mart, Target). But make no mistake, the CEOs were not talking to us with their bullish statements. They were talking to consumers and more importantly, to employees. They have no choice but to be very upbeat, get their salesforce jazzed up in the process, and sit and hope that things play out in their favor. Even this week, when we inevitably get negative datapoints on sales versus last year, the press releases will contain verbiage intended to keep hope alive that business will pick up materially throughout December – the elevated levels of inventory are banking on it.

If there are any numbers we come remotely close to trusting about the weekend, they’re online sales growth numbers given by the sources below. All in, it suggests that sales growth slightly accelerated vs last year on Thanksgiving, but growth was lower on BF vs last year. The numbers are hardly consistent, but we’ve found that all four in concert have been a good directional indicator as to how things are going. If we had to believe just one of the sources, it’d be IBM, which has been closer to the mark in the past with its reporting.

FINANCIAL TRAJECTORY IS NOT LOOKING GOOD

But the real thing we care about is the financial trajectory in aggregate for the group, which we aggregate below. We have eight historical quarters of sales, margins, earnings, working capital and capex, along with quarterly consensus estimates through mid 2016.

Sales and Margins: The good news is that consensus is looking for just 1.2% sales growth in 4Q (ending Jan). It happens to be on top of a very solid 6.8% sales growth number last year – but at least the Street seems to have done the math right with 4Q revanue estimates. On the flip side, the Street is looking for revenue growth to pop back up to a 3-4% rate in 1H16. That’s not eggregious, but its more aggressive than we see in 4Q.

Margins: Margin expectations look too high. While 80bp below last year, the Street’s 4Q margin target (columns in the chart below) looks too high. It represents a 100bp sequential increase, which simply does not seem plausible given the inventory overhang. Etimates also assume that we’re back to flat yy by 2Q, which also seems very aggressive. In other words, the street is treating this slowdown as a weather event – and nothing more. If the economy is actually weakning, which we think it is, then sales will come down, and margins will come off materially.

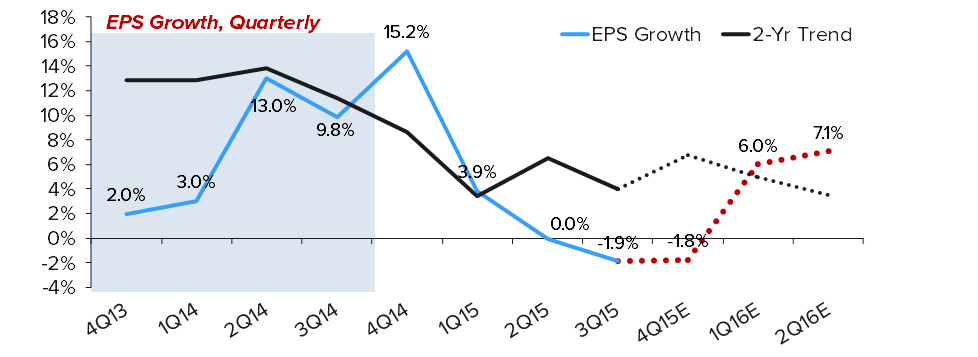

EPS: Third quarter EPS declined by 1.9% for the group. The good news is that 4Q estimates call for a similar decline. We think it will be worse than that, but perhaps not terribly. The risk, however, is that growth expectations pop back up to mid-single digits rather quickly after 4Q. As noted in the Sales/Margin discussion, we need to assume a rock solid economy for this to happen.

Capex: has been quite stable for the past two years at a fairly low rate of 3.8% of sales. That said, we’re hard pressed to find a retailer that is not increasing its planned rate next year as it invests more in e-commerce. We stress ‘planned rate’ because the dollars are in motion, but if the sales level comes in weak, which happens commonly when we’re late in a cycle, then the rate goes up materially.

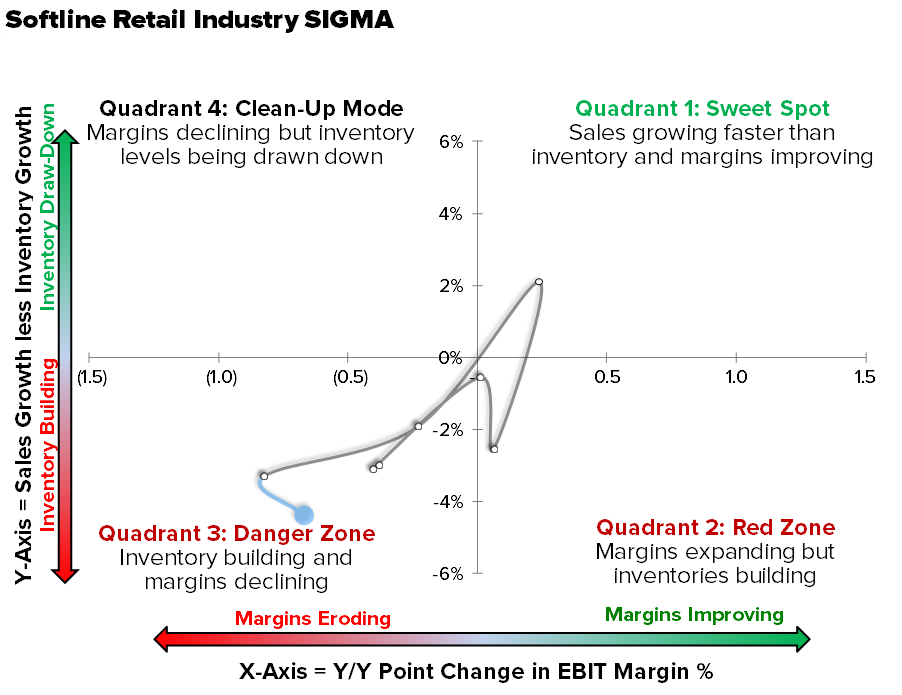

SIGMA: In looking at the triangulation of sales, inventories and margins (SIGMA) the group has the unfortunate distinction of being in the lower left hand quadrant for the second consecutive quarter. That means inventories are growing faster than sales, and margins are down. The only thing we could realistically see at this point is a defensive move to clear inventories, which would mean another leg down in margins. We see that often at the company level, but it’s rare to see an entire group of companies move in concert to clear inventory. Realistically, we’re looking at a negative 2-3 quarter event.