Editor's Note: Below is a brief excerpt from today's Early Look written by Hedgeye's Director of Research Daryl Jones. Click here to subscribe.

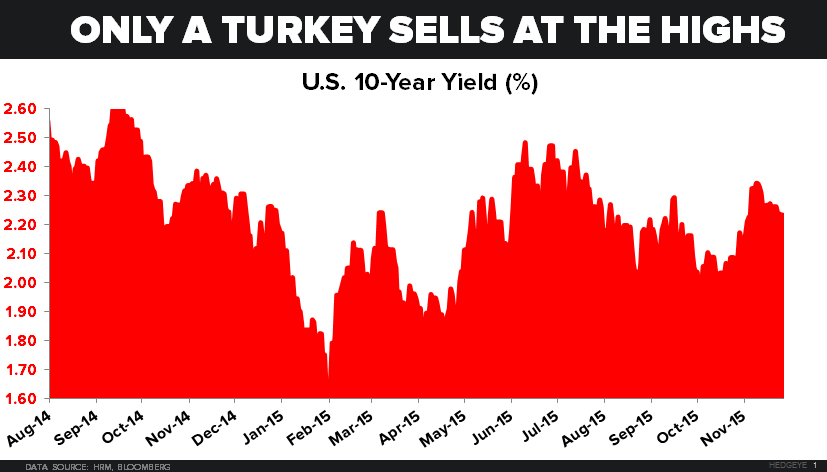

"... Now we certainly give money managers credit for being savvier, as it relates to the markets, than most members of the Federal Reserve, but the Chart of the Day shows that their “projections” may be almost as inaccurate as the Fed. As the chart highlights, in September 2014, the last time investors were selling Treasuries at this rate, it was basically at the peak in 10-year yield. So the moral of the story is: only turkeys sell at the lows."