Takeaway: DE gave low quality guidance that exceeded consensus, a strategy we think may backfire later this fiscal year. While the key components of the guidance look conservative at first, the outlook assumes stabilization in collapsing unit sales – a very tall order given our view of industry trends. DE’s outlook also benefits heavily from a convenient change in pension & OPEB assumptions. Long-term, we think DE is trapped in a less severe version of the 1980s Ag Equipment down-cycle, offering perhaps ~30% relative downside from current levels. DE is increasingly shifting to an FY17 story, as well. Shorter-term, we expect the report to pressure bears and allow us to repeat our ‘short-a-squeeze’ strategy.

Key Earlier Notes:

Replay & Materials From Ag Equipment Black Book

- Slides: CLICK HERE

- Replay: CLICK HERE

Best Ideas Addition (5/22/15)

Where To From Here (9/21/15)

Removing As Best Ideas Short (11/24/15)

Dissecting the Outlook

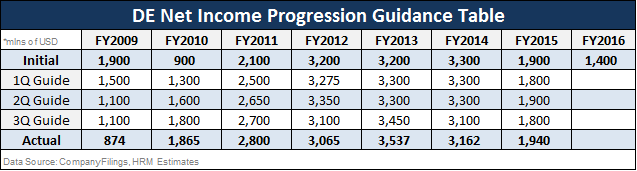

We’ll let others summarize DE’s quarter, as only one section of the release really matters: Guidance. We think DE’s FY2016 guidance is truly incredible in that it is difficult to believable. Management overshot with a back-end loaded $1.4 billion net income outlook, we think, which was puffed up with a “candidly…more accurate” change in pension & OPEB assumptions. Ag Equipment demand in DE’s key markets is in free fall; management ought to have included a larger buffer to accommodate continued deterioration. The outlook instead appears to assume stabilization at current run-rate levels.

Short Squeezes: For longs, the aggressive, low quality guidance risks an outlook cut later in the fiscal year. Who wants to buy DE shares on that? For the moment, the answer is weak longs and those trying to pick an Ag Equipment cycle bottom. We plan to wait for a fairly clear squeeze to add it back as a Best Ideas short, even though that strategy risks missing the next down move in the shares.

Big Picture: Our view is that the Ag Machinery industry is in a 1980s-lite scenario, a case we laid out in our Twin Peaks & Mid-Cycle Myths black book. In major capital equipment downswings, management and investors are typically surprised at just how far demand can fall. The recent downturn in mining equipment is a good example - sales of new equipment pretty much evaporated. Used equipment often competes with new equipment just as deteriorating borrower credit disrupts financing. If our view for the Ag Equipment industry is accurate, sales levels should continue to slip from the lofty 2013 peak.

Weak Guidance Strategy: The character of the FY2016 guidance may prove to be another hit to management credibility* following the unneeded FY2Q to FY3Q guidance fiasco. We would have expected management to guide to consensus, and then hope to ratchet the outlook higher over time. Fiddling with actuarial assumptions and guiding higher than needed is likely to be unhelpful. The guidance also assumes that the free fall in equipment sales abates, which may prove optimistic.

Implied Decrementals Not Too Aggressive: Maintaining current FY15 decrementals should prove challenging as DE cuts production to abnormally low utilization (e.g. single shift). However, guidance assumes a drop in decrementals excluding the benefit of the Pension/OPEB assumption change.

Yield Expectations Also Reasonable: Sure, yields could drop a bit.

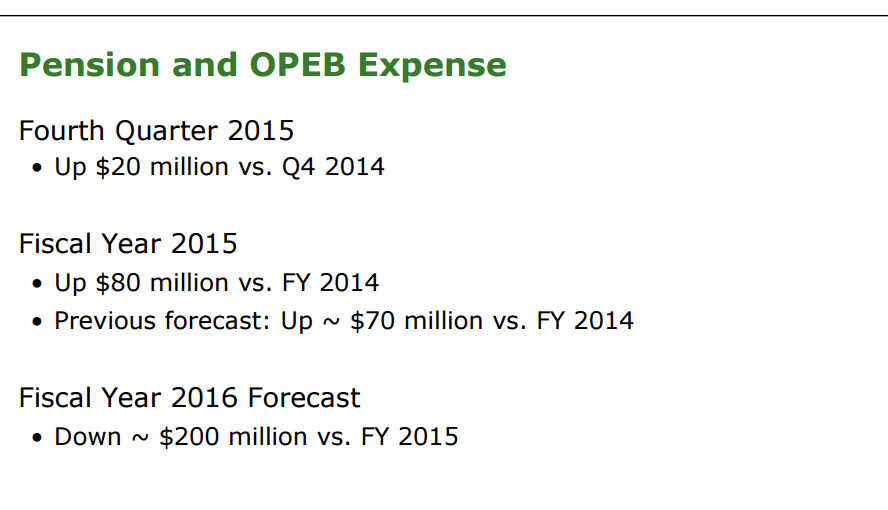

Lowering Costs Through New Pension/OPEB Assumptions: A driver of the higher guidance relative to expectations is Pension & OPEB expense, a huge 2016 tailwind. In late 2014, DE’s FY2015 guidance included a far smaller $85 million headwind. It is a low quality cost decline, but it has also been a market where accounting quality has been largely ignored. It may push out the DE short case, which is increasingly shaping up as a late FY16/FY17 story.

Source: Company Filings

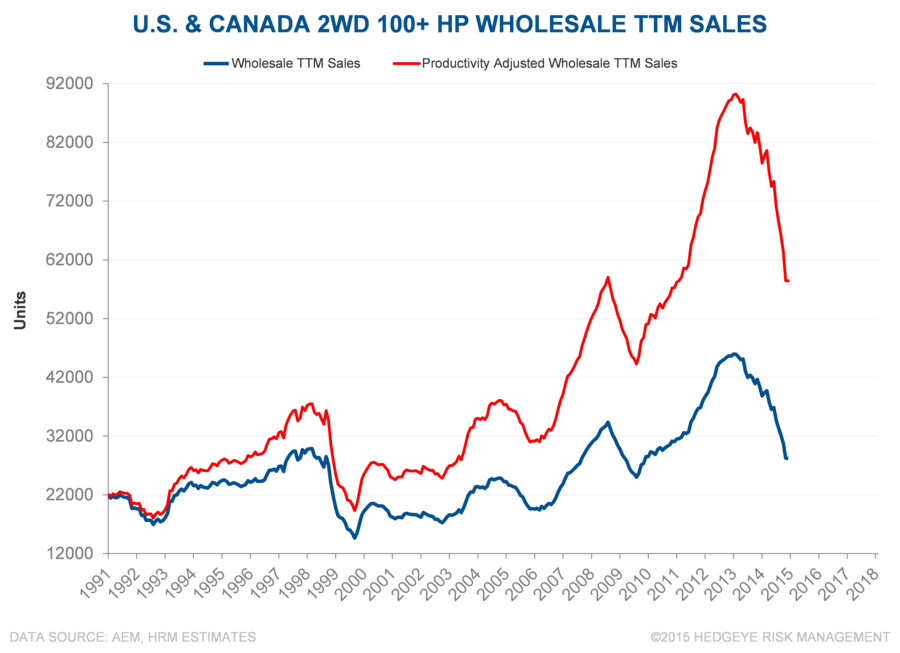

Units Likely Unreasonable: DE is a short thesis that is in the process of playing out, we think, and it is easy to mistake ‘new lows’ for a ‘bottom’. Cyclicals also tend to look “cheap” all the way down. Guidance assumes a significant deceleration in unit sales declines, by our estimates. Sales are in a free fall from very high productivity adjusted levels. In the late 1990s and early 1980s, unit declines continued at a pretty severe pace without much let up. Early order indications for 2016 have been horrific vs. 2015 levels (which were already down). Declines from peak look large, but can readily continue. There is no quick cure for too much industry capacity/equipment.

Too Reliant On Deere Financial, Especially Into FY17: The 2016 profit outlook also relies heavily on Deere Financial. Credit quality is likely to follow softening metrics like farm values, used equipment prices, and past dues. As the portfolio shrinks into FY17, in our estimates, Deere Financial may prove an uncertain source of a high percentage of DE’s profitability.

ICYMI - Why the strong quarter? Continuing the low quality theme, much of the beat relates to a lower tax rate.

Upshot: DE gave low quality guidance that exceeded consensus, a strategy we think may backfire later this fiscal year. While the key components of the guidance look conservative at first, the outlook assumes stabilization in collapsing unit sales – a very tall order given our view of industry trends. DE’s outlook also benefits heavily from a convenient change in pension & OPEB assumptions. Long-term, we think DE is trapped in a less severe version of the 1980s Ag Equipment down-cycle, offering perhaps ~30% relative downside from current levels. DE is increasingly shifting to an FY17 story, as well. Shorter-term, we expect the report to pressure bears and allow us to repeat our ‘short-a-squeeze’ strategy.

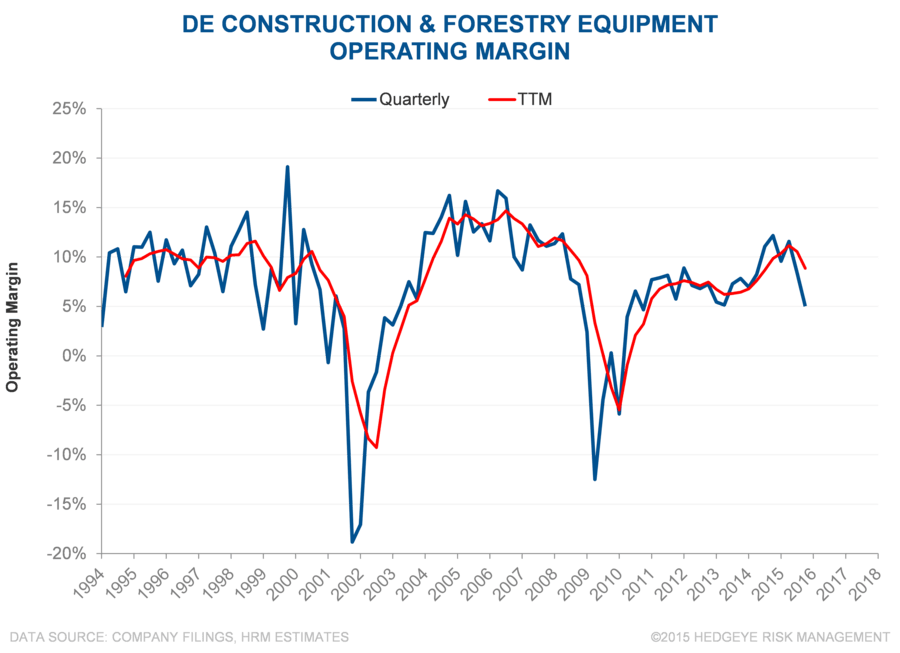

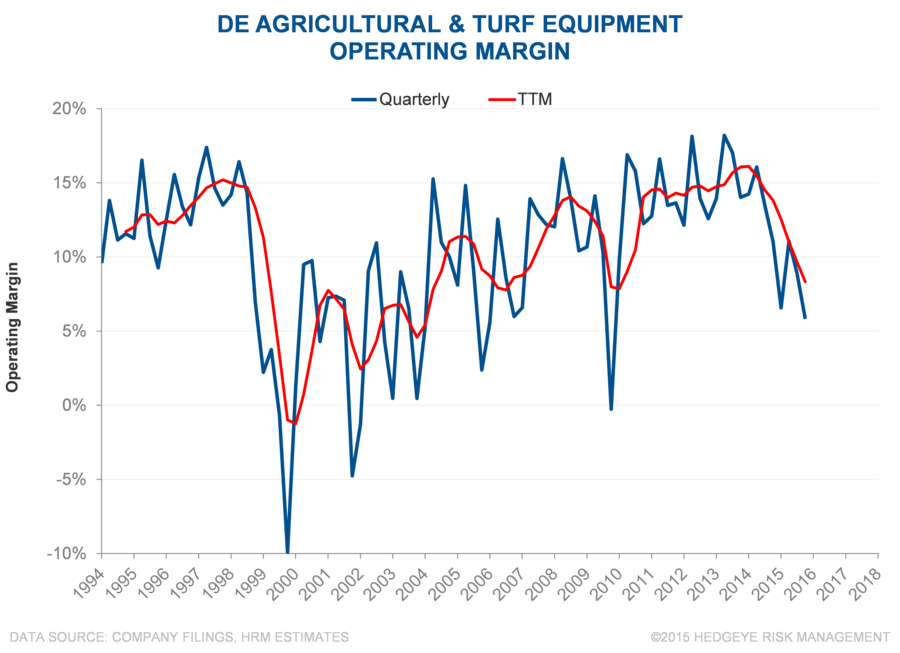

DE & Segment Margins

*To clarify, we believe management is doing very well with what they have. Unfortunately, outside of subject experts, few market participants are likely to notice as the cycle overwhelms excellent execution.