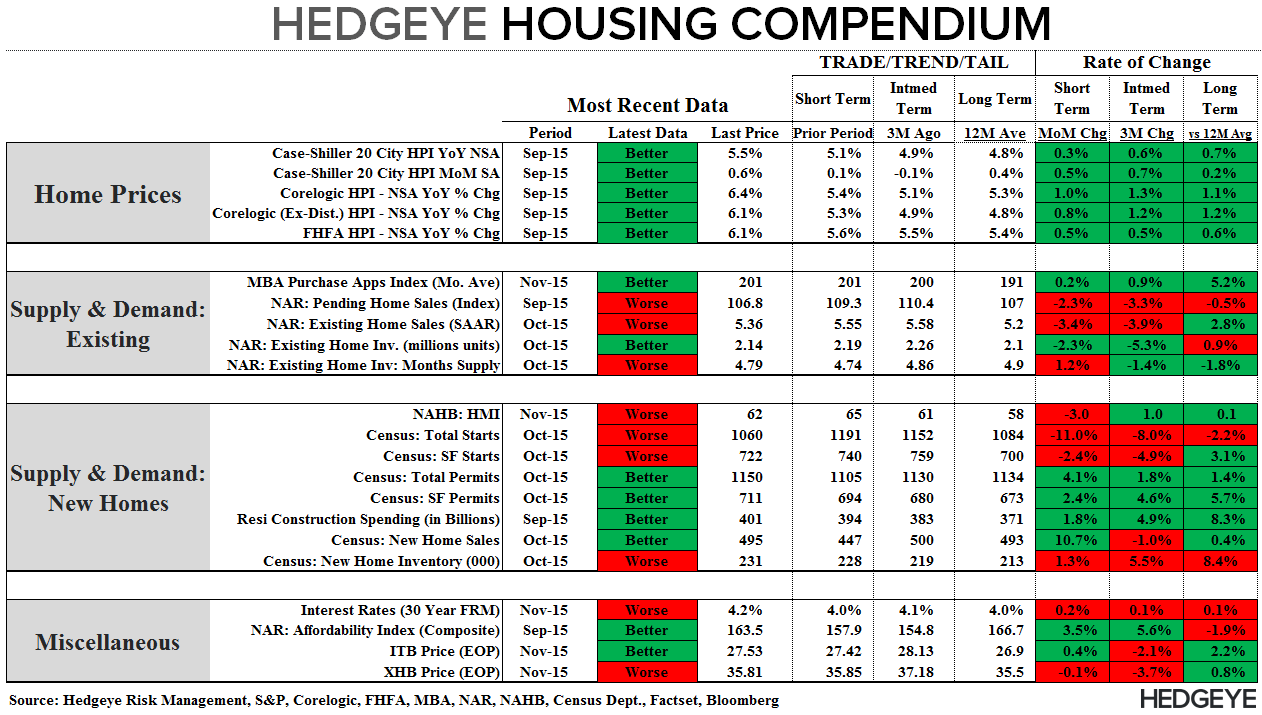

Our Hedgeye Housing Compendium table (below) aspires to present the state of the housing market in a visually-friendly format that takes about 30 seconds to consume.

Today’s Focus: New Home Sales for October, FHFA HPI & MBA Apps

In Short: Purchase Demand held above trend for a 2nd week, New Home Sales in October retraced the Sept cratering and FHFA HPI confirmed the acceleration in Prices.

We’ll try to keep it tight here in reviewing the pre-holiday data deluge in housing.

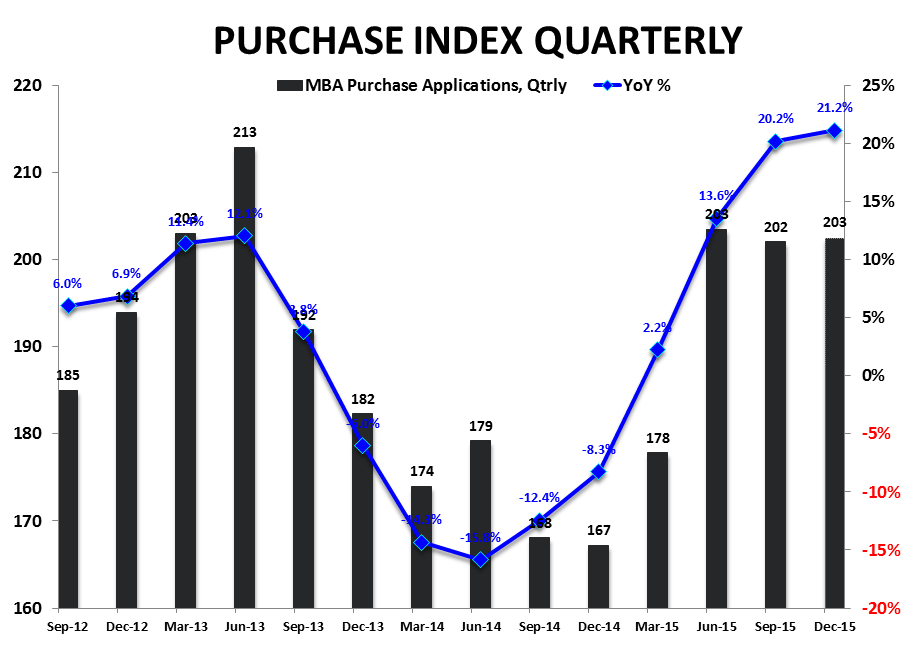

Purchase Applications: Purchase demand dipped -0.5% WoW and accelerated to +24% YoY, providing some soft confirmatory evidence that last week’s +11.9% gain was more than just statistical noise in a holiday week (Veteran’s day). Two weeks of strength now have 4Q tracking +0.3% higher QoQ and accelerating to +21.2% YoY.

Alongside (what the Fed hopes is) the most well-telegraphed rate hike in history, its more probable than not that we’re seeing some measure of demand pull-forward with prospective buyers pulling the purchase trigger in fear of further financing based affordability declines.

While comps remain easy the next 5-6 weeks and the data should remain good on balance, discerning a clear trend in the underlying data during the holiday period is challenging as imperfect statistical adjustments can push the data either way in any given week.

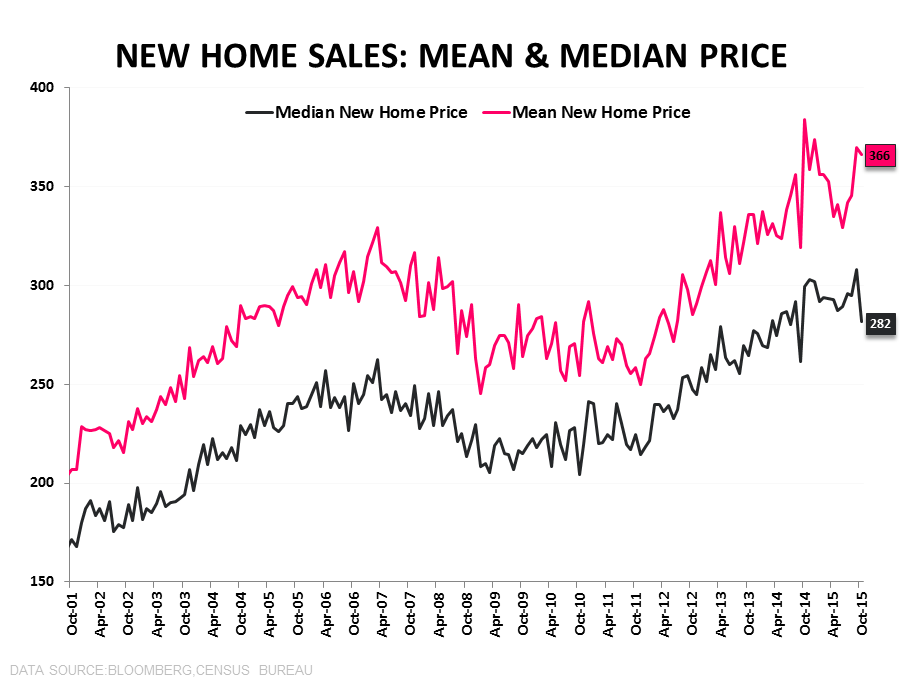

New Home Sales: New Home Sales rose +10.7% MoM in October following the bomb of a print in September (-12.9%, which was revised further lower). What happened in September is unclear but we do know a couple things:

First, NHS is the most volatile housing series there is and carries a large standard error with significant subsequent revisions.

Second, the NHS estimate methodology is particularly sensitive to the impacts of TRID implementation. NHS estimates are imputed based on permits data but many new homes have a sales contract prior to permit issuance – and any TRID related pull-forward would mostly likely show up as un-permitted, signed contracts.

In any case, at 495K in October, NHS sit exactly on the TTM average and just below the YTD average of 499.6K with sales thru October running +15.2% over the same period last year. So, on net, perhaps some marginal weakness the last two months with the latest month rebounding back to Trend.

FHFA HPI: The FHFA HPI series accelerated +50bps sequentially to +6.1% YoY. With the Case-Shiller series also registering acceleration yesterday, all three of the primary price series are telling a congruous, positive 2nd derivative HPI story. We reviewed the Case-Shiller data and the supply situation yesterday (HERE) and we’ll get our first look at October price data with the CoreLogic HPI release next week.

About New Home Sales:

Each month the Census Department releases the New Home Sales report, which measures the number of newly constructed homes that have been sold in the month. The difference between the New Home Sales report and the Starts and Permits report is that New Home Sales only includes single family spec homes built and sold by builders, and does not include condos, apartments, or owner-built units. This is why New Home Sales typically run at roughly half the rate of Starts.

About MBA Mortgage Applications:

The Mortgage Bankers’ Association’s mortgage applications index covers more than 75% of mortgage applications originated through retail and consumer direct channels. It does not include loans delivered through wholesale broker and correspondent channels. The MBA mortgage purchase applications index is considered a leading indicator of single-family home sales and construction. Moreover, it is the only housing index that is released on a weekly basis.

Frequency:

The MBA Purchase Apps index is released every Wednesday morning at 7 am EST.

Joshua Steiner, CFA

Christian B. Drake