For the record, veteran Hedgeye Restaurants analyst Howard Penney has been bearish on Shake Shack (SHAK) since it went public in February. In a "mince-no-words" moment back in May, he wrote:

“The Shake Shack charade is over. And I mean over and done. It’s just a matter of time.”

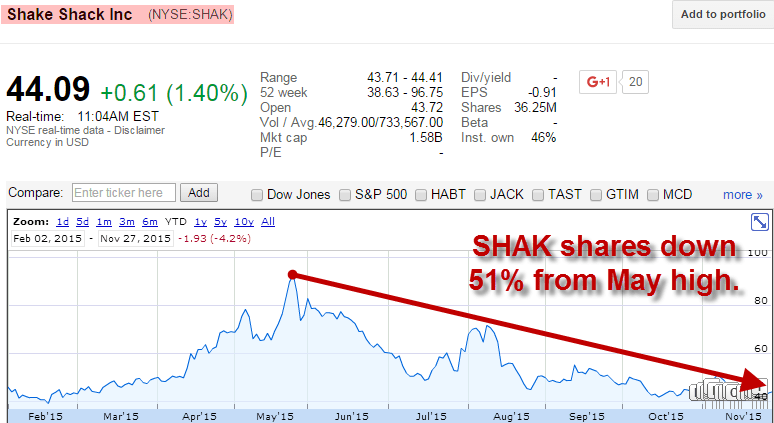

Back when those prescient words succinctly outlined our short call six months ago, shares of the burger chain were approaching what would ultimately be their all-time high. Since then, SHAK is down 35% and off 51% from its May high.

Here’s the chart. It's not pretty:

Penney has maintained his short call on SHAK since originally penning his thoughts back in March. Here are a few interesting excerpts from his March research note:

“For the most part, the SHAK growth story (business model) is predicated on the view that what works well in NYC will work well in the rest of the world… The bull case for the stock centers on the brand’s unique beginnings and its “cult-like” status, which sets it apart from other better-burger operators… We’ve seen many “cult-like” companies come and go and the vast majority of these stories have ended poorly.”

In other words, the company management has extrapolated its initial success in New York City to a growing base of locations in other cities. But outside Manhattan, Penney continues, its average restaurant generates significantly slimmer margins because the brand awareness isn’t as strong.

“The SHAK bears, such as us, argue that new units in dispersed markets typically experience lower average unit volumes and opening-related inefficiencies, such as higher labor costs. In addition, we question whether or not there has been enough investment in G&A to have the necessary resources to work through these inefficiencies by the second or third month.

The bottom line is that, for us, there is a very good probability that SHAK begins opening up some new units that fall short of the Street’s expectations.”

Here's Penney and analyst Shayne Laidlaw in their most recent SHAK research note:

"... Instead of taking the conservative approach of building out its new units with a geographic concentration that allows for SHAK to maintain economies of scale and building brand awareness, management has gone the route that has been the death of nearly every concept that has tried."

Bottom line? We haven't changed our thinking on the stock. Penney sees 40% downside from here.

Look out below.