RECENT NOTES

11/23/15 CMG | SHORT THE FUNDAMENTALS

11/20/15 WEN | REMOVING THE SHORT | GOING LONG

11/20/15 ZOES | ALL IS WELL IN THE KITCHEN

11/17/15 CMG FLASH CALL | SHORT | HYPOCRISY THEORY GAINING MOMENTUM

11/16/15 MCD | THE DAY MCCAFE DIED

RECENT NEWS FLOW

Friday, November 20

HABT | Is postponing its proposed follow-on offering of common stock because of current capital market conditions (ARTICLE HERE)

CMG | National outbreak of E. coli at Chipotle restaurant continued to spread (CDC WEBSITE) (FDA WEBSITE)

MCD | Will try new smaller “Originals” unit in France, paying tribute to the early beginnings of the company (ARTICLE HERE)

Monday, November 16

MCD | To offer ‘McPick” 2 for $2 menu starting on January 4th, with heavy marketing backing from the company (ARTICLE HERE)

YUM | Taco Bell to serve cage free eggs at all 6,000 U.S. locations by the end of 2016 (ARTICLE HERE)

SECTOR PERFORMANCE

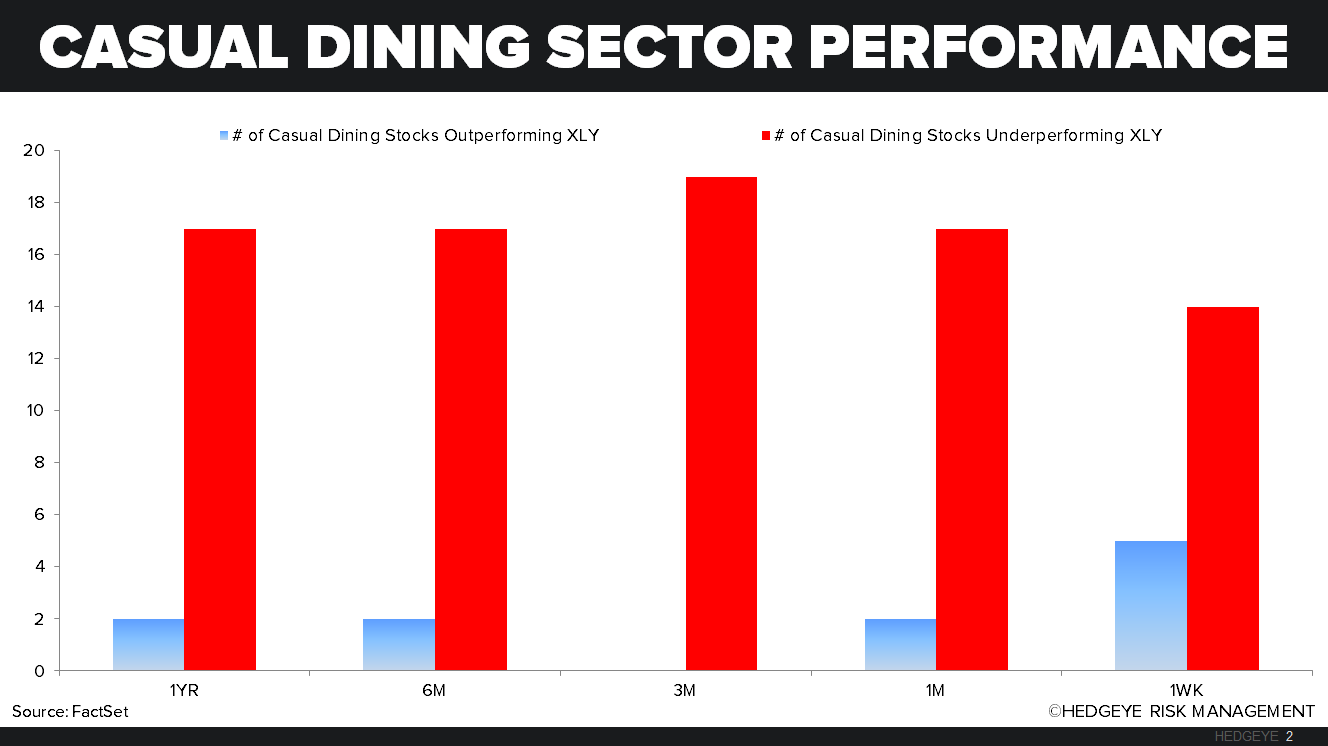

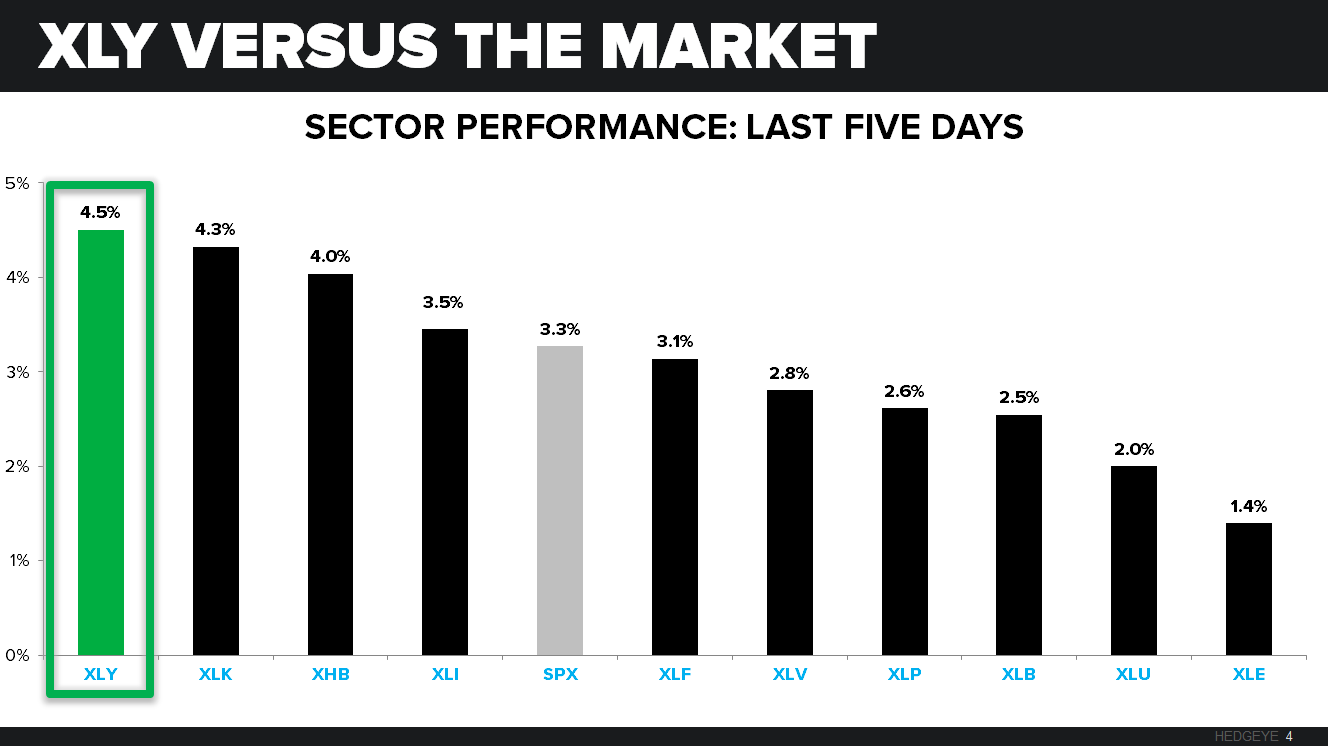

Casual Dining and Quick Service stocks that we follow widely underperformed the XLY, last week, which was up 4.5%. Top performers on a relative basis from casual dining were FRGI and KONA posting increases of +5.8% and +5.0%, respectively, while ARCO and WEN led the quick service group this week up +10.1% and +7.6%, respectively.

XLY VERSUS THE MARKET

QUANTITATIVE SETUP

From a quantitative perspective, the XLY looks BULLISH from a TRADE and TREND perspective, TREND support is 77.99.

CASUAL DINING RESTAURANTS

QUICK SERVICE RESTAURANTS

Keith’s Three Morning Bullets

US stocks had their 3rd up day in the last 13 (Friday) and volume was -14% vs. it’s 1yr avg:

- USD – another #StrongDollar week in the bag (+0.6% USD Index to +10.3% YTD) after Draghi Devaluation sent the Euro -1.2% on the wk to -12% YTD – this is as deflationary a force as it was in the summer-time – FICC markets get that – Equities, not so much

- COMMODITIES – crash in Copper (-1.8% this am to $2.02) continues and Oil is down another -3%, testing $40 WTI (again) – hardly the green shoots a supply/demand bull is looking for, but I’m probably being too bearish looking at fact vs fiction

- UST 2YR – spike continues to 0.93% this morning as the Fed abandons the “data dependence” thing and goes with whatever the SP500 is doing instead – USD and short-term rates say DEC hike – so does the Yield Spread, compressing 9bps last wk, which reads as a hike perpetuating both #Deflation and #GrowthSlowing

SPX immediate-term risk range = 2040-2108; UST 10yr Yield 2.18-2.36%

Please call or e-mail with any questions.

Howard Penney

Managing Director

Shayne Laidlaw

Analyst