Upshot: CAT shares are already under pressure, and we likely wouldn’t press a short position on this week’s events. However, the Cat Financial analyst day continues to suggest that our take on this large and opaque division is on the right track.

Some Relevant Prior Publications

- CAT | Naughty (11/04/15)

- SUMMARY & REPLAY | CAT, JOY USED MINING EQUIPMENT VALUES CALL WITH MICHAEL CURRIE (11/16/15)

Feeling Used? CAT Black Book (latest of many)

- REPLAY: CLICK HERE

- SLIDES: CLICK HERE

Persistent and Substantial Concern

We have been ‘short’ CAT since launching Hedgeye Industrials in 2012, and our next downside catalyst has been investor concern over the firm’s captive finance subsidiary (e.g. see Retrieving Your Excavator From Botswana). We are getting that now. Caterpillar Financial is large, leveraged, and opaque - not a great combination in troubled times. For us, it is a largely straightforward march from excess resource-related equipment to lower collateral values and distressed borrowers. Investor concern about Cat Financial has been building, and has already likely been a driver of share price weakness. Those concerns should persist, dissuading value-trap seeking buyers.

Takeaways

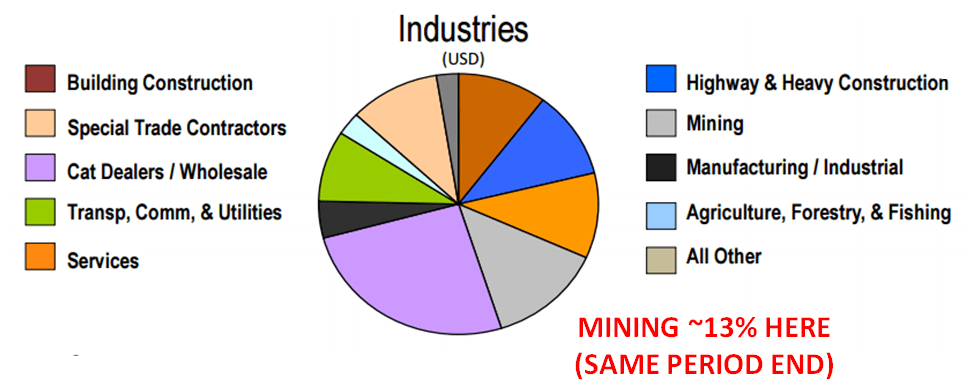

- Sloppy Faux Disclosure: Slide 13 of the presentation mattered, but the colors and units did not match the charts. More importantly, there were NO DEFINITIONS provided for the calculations or industries. This slide wouldn’t make it through a middle school math class, and we would guess that the ‘definition wiggle room’ is intentional. The new disclosures do not reconcile with previous filings, with Mining exposure 2x the prior disclosure. We think it will eventually be re-re-disclosed at even more than 2x.

- Agenda & Pulling Teeth: The presentation was apparently targeted at alleviating concern, but the ambiguity of the new disclosures may backfire. It screams to us “hey, look at how totally incomprehensible and irreconcilable my Finance segment disclosures are.” Good luck with the follow-ups, too, as CAT’s usually top-shelf IR department said they “don’t disclose that level of detail” when asked about mining-related exposures in categories other than “Mining”. If it weren’t there, they probably would have said as much. If it sounds like a silly question, recall Mining didn’t previously capture all of Mining, which is how we got a doubling of the disclosed exposure.

- Street Appeared Utterly Clueless On Cat Financial: CAT only allows Q&A from bulge bracket sell-siders, who have apparently only recently realized that prior portfolio disclosures were not useful. They failed to press for detail on the new disclosures, like how much of Cat Dealer/Wholesale is backed by mining equipment. Shortly, the street is likely to realize that Cat Financial cannot really be diversified since the captive finance sub only lends to CAT customers backed by CAT products. That is not a diverse group by our portfolio management standards.

Bullish On First Glance: At first, the Caterpillar Financial analyst meeting presentation looked pretty good for CAT. The portfolio exposures had not been previously disclosed by industry or really in any useful format as we see it. Slide 13 showed Cat Financial to have a reasonably diversified portfolio, with the larger exposures from North America, small borrowers, and Dealers. None of that seems so bad, right? But Caterpillar Financial’s collateral is all Caterpillar equipment, and how diversified can that really be? A closer look raises some interesting questions.

Mining Exposure: Half Is Not A Large Majority

“Most of it, the large majority of it shows up in the mining segment as broken out in our public filings with the SEC.” – James A. Duensing

First, A 2X Surprise: “Mining” was only 13% of the new pie chart. Of course, that 13% probably came as a surprise to many people, since “Mining” as disclosed in the 9/30/15 10-Q was only 6.7% of the portfolio. Now it is roughly twice that. We had known and written that 10-Q disclosure was not accurate previously.

Source: Caterpillar Financial 9/30/15 10-Q

Source: Caterpillar Financial Analyst Day Presentation, HRM

New Number Accurate? If you can move past the unmatched colors, which certainly imply something, it is worth asking – is 13% actually the right number for Mining exposure? CAT won’t really answer that question, but we are pretty sure that the answer is NO.

Where Will Mining Go Next? We would bet that “Special Trade Contractors”, “Services”, and/or “Cat Dealer/Wholesale” also contain mining exposure. First, not all mining equipment is operated by mines, and mining contractors have been more likely to sell used equipment of late (Used Mining Equipment Values Call with Michael Currie https://app.hedgeye.com/feed_items/47572-summary-replay-cat-joy-used-mining-equipment-values-call-with-michael-currie). We would expect “Cat Dealer/Wholesale” portion, which we presume has the Caterpillar Purchased Receivables, to contain actual trade exposure to mining. Readers can check the Joy Global 3Q15 earnings call transcript to see how that is working out. And what, exactly, is “Services”? We would expect the disclosed Mining exposure to move higher on these slippery definitions.

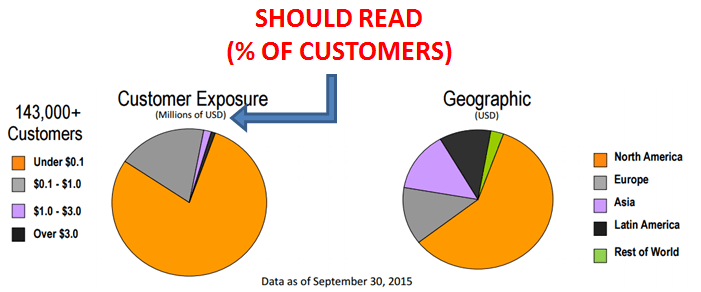

Mislabeled Customer Exposure Table: The Customer Exposure pie chart is labeled as (Millions of USD), so any reasonable reader might assume that pie chart shows the dollar value of the portfolio from each loan size category. But it is not – it is mislabeled in a way that makes Caterpillar Financial look more diversified. When asked, CAT disclosed that the chart “shows a percentage of our customers with exposure in the various exposure categories”. If that >$3.0 million slice were 10%, which would still look small and manageable, it would equal >$43 billion in portfolio exposure (bigger than the actual portfolio). This chart may look reassuring, but provides little specificity on Cat Financial’s customer concentration. Are we expected to believe that a Fortune 500 company doesn’t know how to properly put units on a pie chart? Or did management prefer the message conveyed by the inaccurate units?

Source: Caterpillar Financial Analyst Day Presentation, HRM

Residual Values

“Almost 90% of the machines that we have from off of a lease conversion or from repossession will be remarketed and sold through the Caterpillar channel.” - Kent M. Adams

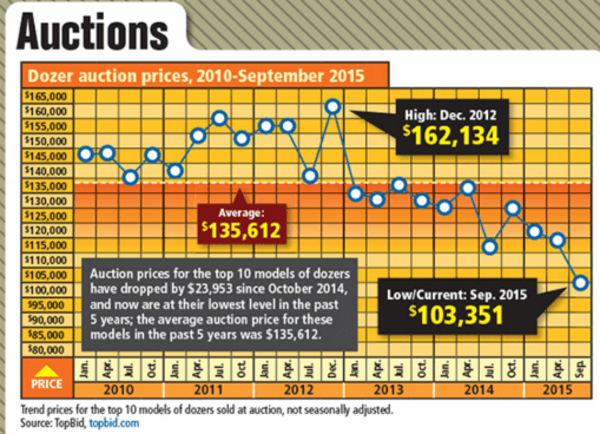

Dealer Resale: A function of a captive finance subsidiary is often to keep residual values high by making sure the sale of used equipment happens in an orderly fashion. It seems to us that CAT is holding equipment off the market, in large part because we have been tracking increased used equipment for sale (to see our recent black book, CLICK HERE). Investors should consider how that can end…

“And then we look at usually a three-year to five-year moving average in terms of historical prices of machines based on our database and how we set that residual, and we set those residuals annually.” - Kent M. Adams

Reset Should Be Interesting: Used equipment values are down pretty much across CAT’s major product categories. While it may take time to flow through to the assumptions, it likely will in our expectations. That is, unless, the “qualitative” part of the reserve process intervenes, as we suspect it did last quarter. Just wait for actual mine closures to see real aftermarket price pressure. Construction equipment is already troubled.

We Will Stop Here: We could go on and on about the analyst call, but we suspect that our point is clear. This is a topic that is still building and may take quite a while to work through.

Upshot: CAT shares have already been under pressure, and likely wouldn’t press a short position on this week’s events. However, the Cat Financial analyst day continues to suggest that we are on the right track in expecting eventual problems from this large and opaque division.