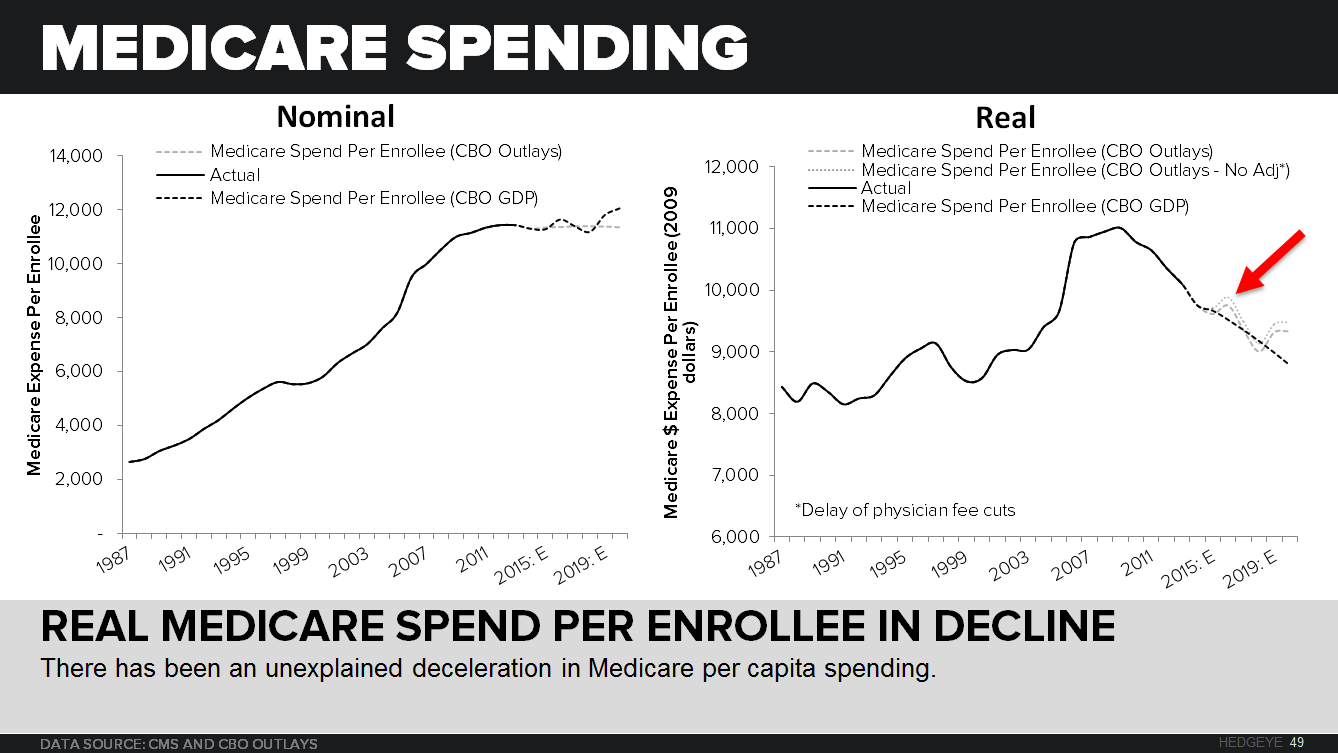

Editor's Note: This is a brief excerpt and chart from today's Early Look written by Hedgeye Healthcare analyst Tom Tobin. Click here to subscribe. He points to this key demographic trend:

"... The Baby Boomers will graduate into Medicare at a faster rate than Medicare spending is forecast to grow, and push growth of real spending per Medicare beneficiary negative.

...But people will get sick in the future and the population will consume more medical care; they will show up to the doctor office, pharmacy, and hospital regardless of the fiscal backdrop. However, when they do make that appointment, the price paid and profit available for those units of care will almost certainly be lower than today, resulting in a secular decline."