Zoes Kitchen (ZOES) is on our Hedgeye Restaurants Best Ideas list as a LONG.

HEDGEYE OPINION

ZOES was never a one or two quarter call for us. Given the high multiple (EV / NTM EBITDA of ~27x) nature of the stock it is ultra-sensitive to the volatile market. Since going LONG the name on 4/08/15 (link to Black Book HERE) at a price of $31.21, we saw a peak in the stock price on 7/23/15 at $45.60 per share and now we are back down to the ~$30 range. This stock does not contain style factors that the market likes right now (high-beta, low-cap), so we expected a turbulent ride, but you must stay strong and buy on the dips. This quarter for instance is a perfect example, there was nothing wrong with it, besides the comp number missing slightly, and the stock was down 9% immediately in after-hours trading, it has since recovered slightly. People that sell on these headlines create great buying opportunities, and we are buyers of ZOES on any big down day like this.

3Q15 RESULTS

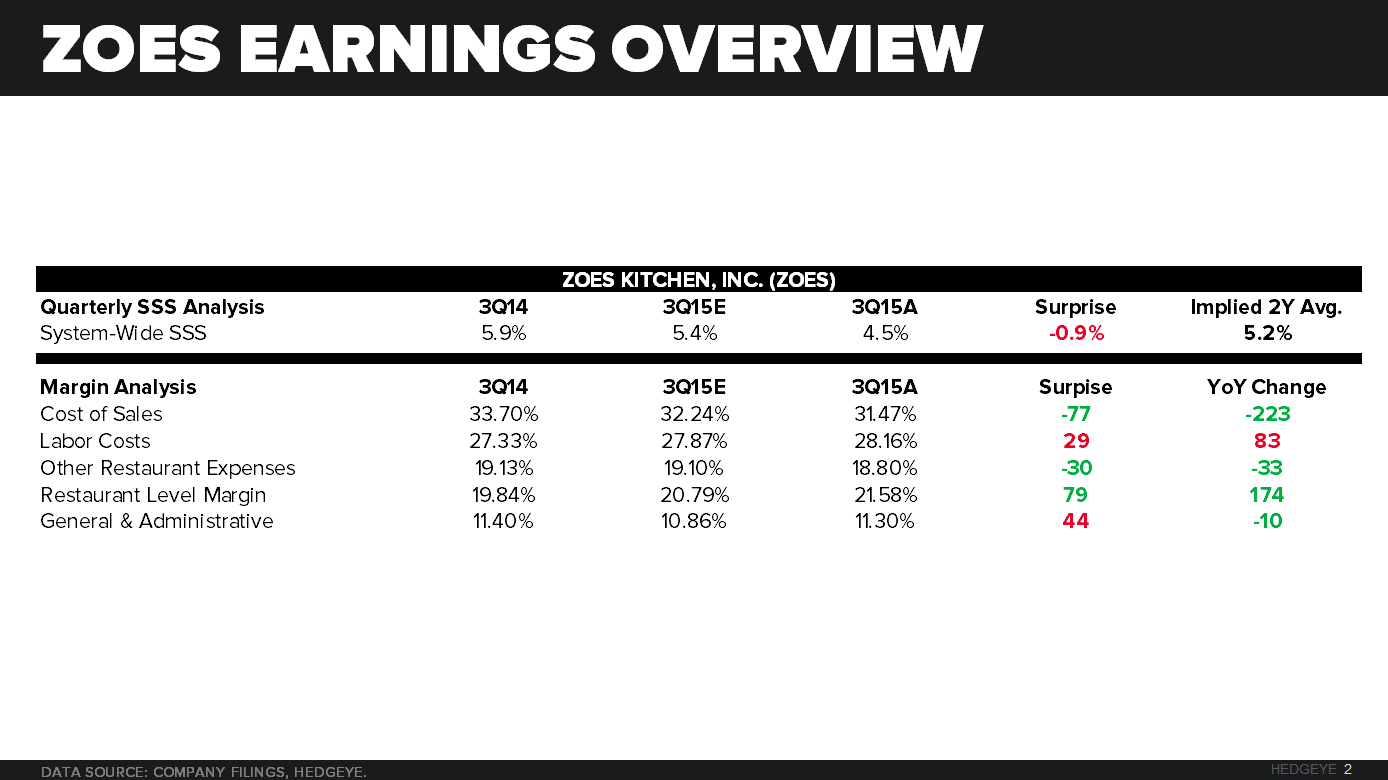

ZOES reported revenue of $56.4 million, representing 29.4% YoY growth and beat consensus expectations of $55.7 million. Comparable restaurant sales increased 4.5%, versus consensus expectations of 5.4%. The comp was built up by +4.6% mix, +0.3% price and a -0.4% traffic. Management’s explanation for why traffic declined was because they have been pushing catering and family offerings, which reduce the actual number of transactions. By diving deeper into this phenomenon, management seemed to have created more questions for themselves than answered. Nonetheless, this was a solid comp performance given they took virtually no pricing. In select markets management is now testing price increases to assess elasticity.

Restaurant level operating margin for ZOES improved to 21.58% an increase of 174bps YoY and beat consensus expectations of 20.79% by 79bps. This improvement was led by a reduction in cost of sales by 223bps down to 31.47% from 33.70% last year. Slightly offset by an increase in labor costs, which were 28.16% in the quarter, up 83bps YoY and 29bps higher than consensus expectations. ZOES prides themselves on hiring great talent and paying higher than the minimum wage, to that end, labor will continue to be a headwind into 2016. Commodity basket deflation will be a minor tailwind for them, as they have been experiencing lower poultry costs

ZOES adjusted net income for 3Q15 was $0.09 million, or $0.05 per diluted share, beating consensus estimates of $0.03 and increasing $0.01 YoY.

DEVELOPMENT

Opened 10 restaurants during the quarter, for a total of 158 company-owned restaurants. Since the end of Q3, ZOES has already opened four more restaurants, bringing the 2015 count to 33 new company-owned restaurants (high end of the guidance). Looking into 2016 ZOES plans to open four stores in Colorado and three more in Kansas City, which already has one store.

MANAGEMENT GUIDANCE

For the full year 2015 the company updated guidance slightly. Restaurant sales will be between $222 million and $224 million versus previous guidance of 220 million and $224 million. Comparable restaurant sales growth of 5.5% to 6.0% versus previous guidance of 5.0% to 6.0%. Restaurant contribution margin of 20.3% to 20.6% versus previous guidance of 20.0 to 20.5%.

Please call or e-mail with any questions.

Howard Penney

Managing Director

Shayne Laidlaw

Analyst