Below are our analysts’ updates on our eleven current high conviction long and short ideas. As a reminder, if nothing material has changed in the past week which would affect a particular idea, our analyst has noted this. Hedgeye CEO Keith McCullough’s updated levels for each ticker are below. Please note that we removed Vanguard Extended Duration ETF (EDV) this week.

LEVELS

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

IDEAS UPDATES

TLT | JNK

To view our analyst's original report on Junk Bonds click here.

The long bond position is taking some heat with the rate hike fears, but that’s why you’re short JNK on the other side of it. Deflation and increasing rate hike expectations are the nemesis of poor credit. As mentioned last week, it’s called spread risk, and this leverage is fueled by low rate policy.

Since the Fed turned hawkish, bonds are down, rates have risen, and deflation has re-commenced. Admittedly, long-term treasuries haven’t worked. TLT is down -2.0% over the last month; BUT, if you’ve followed us with our short JNK call, that’s down -3.4%.

So as not to take too much credit for a gain here on the TLT/JNK pair, we also had EDV on Investing Ideas until Thursday, and here’s what Keith McCullough had to say about taking down some long-bond exposure (which we sent in a note to Investing Ideas subs):

“With the Fed hell bent on raising into a slow-down, we have to risk manage the risks associated with that. They have no idea on the economy (forecasts on growth have been wrong 70% of the time since Bernanke's un-elected reign). So the risk, is their forecast."

Looking at the data this past week (because, at Hedgeye, our market calls ARE actually data-dependent):

- Industrial Production printed down -0.2% sequentially for October (and that was off of a base of -0.2% for September!)

- Headline CPI printed just +0.2% Y/Y for October (That smells like deflation)

- Core CPI (the Fed’s preferred measuring tool), came in at +1.9% Y/Y for October. Hey, that’s almost at the 2% target. Maybe they’ll hike on that into this late cycle slowdown

If the Fed does hike into a late-cycle slowdown, the only thing that will be lifting off is long-term bonds.

WAB

To view our analyst's original note on Wabtec click here.

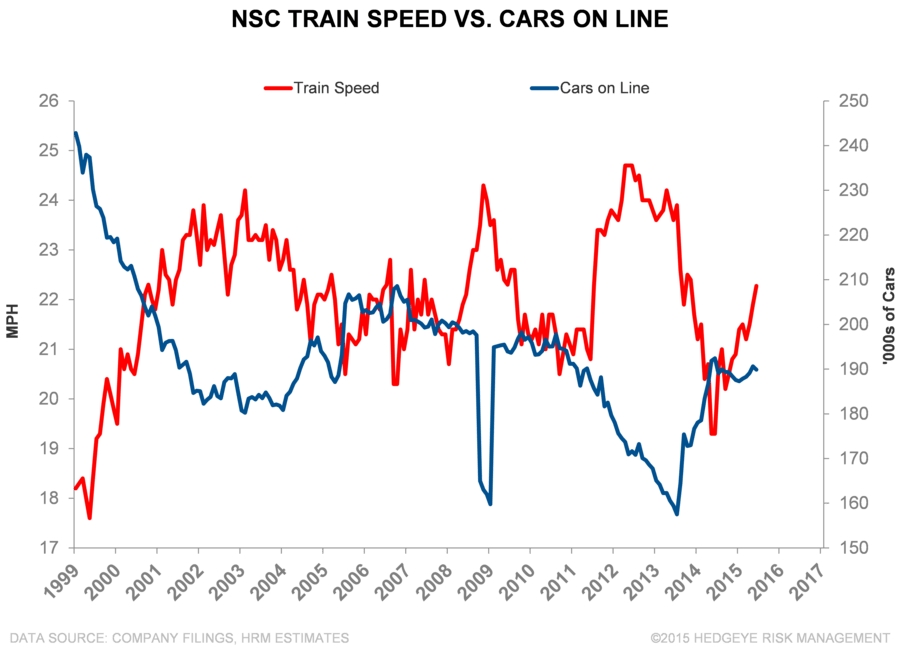

In 2014, rail congestion picked up. The slower speeds tended to pull equipment onto the track. Now that speeds are picking back up again, we expect that equipment to be pushed back out.

One can think of it as turning existing assets more quickly. Norfolk Southern (NSC) illustrates the relationship below. More speed results in less equipment in service. If speeds continue higher, freight railroads may find themselves with ample excess equipment and reduced aftermarket needs amid slow volume growth – a negative combination for Wabtec (WAB).

MCD

To view our original note on McDonald's click here.

Last week on November 10th we attended the McDonald’s (MCD) Investor day and came away even more bullish than we went in.

As expected, MCD is now reducing G&A by $500 billion compared to the $300 million target announced in May the vast majority of which they expect to realize by the end of 2017.

Expectations going forward are for system sales to grow faster than G&A. The incremental savings are primarily derived from savings coming from a more heavily franchised and less G&A intensive structure; streamlining of corporate and former Area of the World organizations and realizing greater efficiencies through the global business services platform. The G&A savings represent roughly a 20% reduction off of the G&A 2015 base of $2.6 billion.

Another big shift is that MCD is now aiming to refranchise 4,000 restaurants by the end of 2018, with mostly all of them to take place in the high-growth and foundational segments. The refranchising target of 4,000 restaurants by 2018 implies approximately 1,000 restaurants per year and will move MCD from 81% franchise today to about 93% franchise globally. Putting MCD well on their way to the longer term target of 95%. The refranchising strategy will help to improve MCD’s relative multiple versus its peer group.

MCD significantly increased the cash return target for the three year period ending in 2016 to about $30 billion. The $30 billion figure represents a $10 billion increase versus expectations. This aggressive move is further proof in the new management team's willingness to change the MCD business model and make the appropriate adjustments when needed.

The company will use incremental debt to fund the vast majority of this increase. The $30 billion cash return target will be nearly double the $16.4 billion for the three-year period ending 2013.

Importantly, MCD for the first time will manage to a non-investment grade rating of BBB+ at S&P and Baa1 at Moody's credit ratings. Going forward (beyond 2016) , MCD intends to return all free cash flow to shareholders over the long-term through a combination of dividends and share repurchases.

LNKD

To view our analyst's original report on LinkedIn click here.

There were no material developments for LinkedIn (LNKD) this week. Even though the selling environment remains solid, we're still cautious about staying long into LNKD's 2016 guidance release. The good thing is that the release won't be until February. As a result, we will get at least 2-3 more updates to our proprietary LNKD tracker before then.

If our tracker continues to improve, then we may stay long into the release. If not, we're definitely going to get out of the way and will reasses the setup post print. More to be revealed.

W

To view our analyst's original report on Wayfair click here.

As we’ve been saying, Wayfair's total addressable market is much smaller than many people believe. People, including Management, are using numbers like $90bn as an addressable market. That’s just flat-out wrong. We’ve done extensive research on this one, and when all is said and done, we think that the end market is no more than $30bn.

To put that into context, that suggests that Wayfair has about a 10% share of its market. That’s 2-3x the share of players like RH and IKEA. There’s absolutely no reason why this should be the case.

The purchasing process for a consumer durable, like a set of bunk beds, for example, almost always includes in-store visits as well as online research. You get that at Williams-Sonoma, Restoration Hardware, and even Pier 1. But you can’t touch and feel the seven million items sold by Wayfair before you buy. In fact, our research suggests that W’s target consumer has a ‘blind buy’ threshold of around $750. That’s well below the prices listed for furniture sold on its websites.

TIF

To view our analyst's original report on Tiffany click here.

Tiffany (TIF) reports earnings on Tuesday, November 24th. Going into the print we think there is a better chance of this being a negative event than positive. Here are some of the data points that point us in that direction:

- Several retailers have highlighted weaker than expected tourism traffic. TIF’s flagship store in NYC accounts for 10% of total sales and is highly levered to international tourist traffic.

- Nordstrom and Macy's saw significant comparable store sales slowdowns. Who is TIF’s core consumer domestically? Look no farther than these two comps.

- E-commerce traffic rank slowed throughout the quarter. E-commerce only accounts for 6% of sales at TIF, but it’s a good barometer for brand relevance and most of TIF's sales are in categories that generally require prior research.

- US jewelry store retail sales slowed to -0.4% in August and September, from +1.5% in 2Q15.

RH

To view our analyst's original report on Restoration Hardware click here.

Below are two callouts from this Thursday's Willams-Sonoma (WSM) third quarter earnings print as it relates to Restoration Hardware (RH). RH will report earnings in early December.

- West Elm – i.e. the only concept within the WSM family of brands that is growing square footage put up a 15.7% comp in the quarter which equated to a 40bps acceleration on a 2yr basis sequentially. The concept has always been a good bellwether for RH from a directional standpoint. The consumer/concept are much different. West Elm productivity is in the $800/sq.ft. range compared to RH at $3,300 (inclusive of e-comm) in the same size box. But it’s the only concept growing square footage. We are modeling a divergence in 3Q15 as RH pushed its growth into 2H from 1H with the release of two new concepts this Fall (Modern and Teen).

- GM – was down 110bps in the quarter, with merch margins relatively flat offset by dilution from International franchise growth and increased shipping expense as WSM continues to iron out its inventory position from the West Coast port contract dispute. It's important to mention the contract dispute because it was resolved nine months ago (and yet the company still talks about it). On the shipping front, new rate hikes at FedEx and UPS haven’t hit the P&L, so this was all self-inflicted. Each of the negative drivers on the GM line appear to be unique to WSM and shouldn’t be contagious to a name like RH.

ZBH

To view our analyst's original report on Zimmer Biomet click here. To watch a replay of a video with our Healthcare analyst Tom Tobin discussing field notes on ZBH click here. Below is an update on our ZBH Short call:

We spoke with an orthopedic surgeon this week to discuss case volume trends, device pricing, and the impact from the CCJR*. The near term impact of the CCJR is likely to be small, but should become a meaningful headwind over our investment timeframe. Other comments included a view that:

- Consolidation is heating up in direct response to "population health."

- Orthopedic groups are "milking" the rehab system by driving patients to practice-owned rehab facilities ("30% of practice income").

- Patient-matching (cheap implants for Medicare patients) results in device cost "2X to 3X" for commercially insured patients versus Medicare patients.

- Blue Cross and other payors are developing more restrictive implant guidelines including limits on patient BMI, or HbA1C at "controlled" levels.

In our view, these insights confirm that the structural policy headwinds, deflation, and slowing volume remain firmly in place.

*Comprehensive Care for Joint Replacement (CCJR) is a CMS initiative to change reimbursement for total joint replacements from fee for service to a bundled payment based on single episode of care.

GIS

General Mills (GIS) continues to be one of our top ideas in the Consumer Staples sector. Sector head Howard Penney loves the name for its characteristics during this macro driven market. Big-cap, low-beta, and their line of sight at growing the top line in a meaningful way, are contributors to our LONG thesis.

ZOES

All is well at Zoës Kitchen (ZOES).

On Thursday, ZOES reported revenue of $56.4 million, representing 29.4% year-over-year growth, beating consensus expectations of $55.7 million. Comparable restaurant sales increased 4.5%, versus consensus expectations of 5.4%. The comp was built up by +4.6% mix, +0.3% price and a -0.4% traffic.

Management’s explanation for why traffic declined was because they have been pushing catering and family offerings, which reduce the actual number of transactions. By diving deeper into this phenomenon, management seemed to have created more questions for themselves than they answered. Nonetheless, this was a solid comp performance given they took virtually no pricing. In select markets management is now testing price increases to assess elasticity.

Restaurant level operating margin for ZOES improved to 21.58% an increase of 174bps year-over-year and beat consensus expectations of 20.79% by 79bps. This improvement was led by a reduction in cost of sales by 223bps down to 31.47% from 33.70% last year. That was slightly offset by an increase in labor costs, which were 28.16% in the quarter, up 83bps year-over-year and 29bps higher than consensus expectations.

ZOES prides themselves on hiring great talent and paying higher than the minimum wage. To that end, labor will continue to be a headwind into 2016. Meanwhile, commodity basket deflation will be a minor tailwind for them, as they have been experiencing lower poultry costs.